Montana Aerospace (AERO SW) – Riding the OEM Coattails

Taking a look at the Swiss aerospace component manufacturer

Welcome to Bristlemoon Capital! We have written previously on AER, ADBE, TDG, the AI bubble, FICO, GOOGL, ASML, SNPS, UNH, META, GRND, HEM SS, MELI, U, APP, PDD, IBKR, PAR, AER, PINS, BROS, MTCH, CPRT, RH, EYE, and TTD.

If you haven’t subscribed, you can join 5,954 others who enjoy our deep dives and investment insights here:

Australian wholesale investors looking to invest in the Bristlemoon Global Fund can do so via this link.

Business Overview

Today we’re taking a quick look at Montana Aerospace (AERO SW), the Swiss aerospace company. AERO is one of the fastest growing aerospace suppliers, having grown its Aerostructures revenue at an 11.5% annual rate between FY22 and FY25. This has primarily been driven by market share gains and ramping OEM build rates. The aim of this writeup is to jot down our thoughts on the business and whether it’s interesting enough to be considered for the Bristlemoon portfolio.

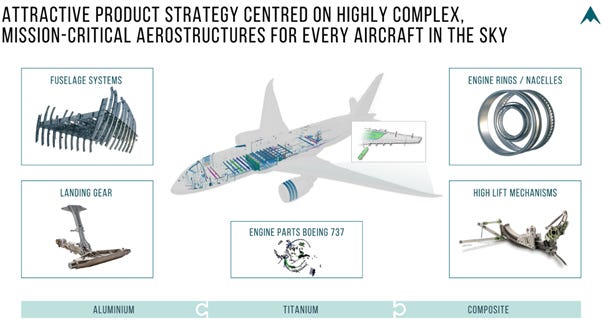

AERO is a supplier of complex, mission-critical components for aviation and space applications. The company’s product portfolio includes structural components for fuselage (think of this as the structural long beams that comprise the skeleton of an aircraft’s fuselage), wings, and landing gear, critical engine parts exposed to extreme thermal and mechanical stresses, as well as large-format extrusion products.

Source: Company filings

The company’s aerospace portfolio is split as follows:

Universal Alloy Corporation (UAC) – manufacturer of aerospace structural components and assemblies.

ASCO Industries – designer and manufacturer of high-lift structures, complex mechanical assemblies, and critical functional components for the aerospace industry.

Montana’s products are on all major commercial aircraft platforms (historically the company has had a roughly 50:50 split between Boeing and Airbus). Back in 2023 the company had around €350k of average shipset content across its platforms, with this expected to ramp up to €450-500k in the years following, driven by new content share wins and further OEM outsourcing[1].

The way AERO works as a business is that they win content on various aircraft platforms. Think of this as Boeing contracting with Montana as a supplier of say, a landing gear product. In reality, there are many different parts that Montana will supply into an aircraft platform (note that AERO offers over 100k SKUs in aerostructures).

This all ties together into a contracted shipset value – that is, the total dollar value of all the components that Montana is contracted to provide for one single aircraft of a specific model. And recall that AERO has significant content on all Boeing and Airbus aircraft types.

So, in this sense you can think of AERO’s sales as being driven by the shipset value multiplied by the number of aircraft that Boeing and Airbus will produce in the future. And how much certainty we can get over Montana’s future sales depends on how long Montana remains as the supplier to that aircraft platform, and how the economics of supplying those components change over time.

There’s reason to believe that AERO will be able to keep selling its products into these aircraft platforms for many years because most of the company’s contracts are “single source” – that is, AERO is the exclusive supplier of that product, creating strong visibility over future revenues and providing barriers to competition (given the time and cost of qualifying alternate suppliers). However, we found it more difficult to get confidence around the pricing power and economics of AERO supplying into those platforms (as we discuss further below).

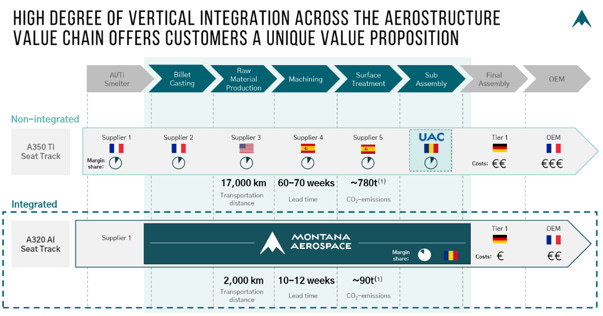

Vertical integration

AERO is vertically integrated – it covers the aerospace value chain from processing raw materials to the assembly of entire components. This removes some of the issues that result from multiple third-party suppliers, whereby there might be delays that are capable of disrupting the entire production process. In contrast, a non-integrated value chain means that the final outcome of the component for the OEM is multiplicative – that is, it requires execution from multiple suppliers and if there’s a hiccup with one then it stalls the entire process (basically one of the suppliers being a “zero” in the multiplicative string of events). AERO can mitigate these risks by having greater control over the value chain.

Source: Company filings