RH (RH) – A Retail Transformation

Can RH climb the luxury mountain?

Welcome to the third Bristlemoon Capital stock write-up. Please see the following links for our previous reports on Copart, Match Group, as well as our appearance on the Business Breakdowns podcast discussing Match.

Bristlemoon readers can also access some of the resources we used to research RH via the links below:

Tegus – Bristlemoon readers can enjoy a free trial of the Tegus expert call library via this link

Koyfin – Bristlemoon readers can get 20% off a Koyfin subscription via this link

Table of Contents

Introduction

Business History

The original Restoration Hardware

Who is Gary Friedman?

How did Gary Friedman end up at Restoration Hardware?

The private era

Business Overview

RH store formats

Store unit economics

The RH ecosystem

RH value proposition

International expansion opportunity

Culture

Is RH a Luxury Business?

True luxury requires heritage

Lack of vertical integration

Luxury taste at scale is an oxymoron

Unbranded goods reduce social signaling

Financials

RH gross margin drivers

Retailer KPIs

Inventory health concerns

RH the compounder

Key stock debates

Will the product refresh be capable of overwhelming the weak macroenvironment?

Parallels to RH Modern launch in 2015?

How much gross margin pain is left?

Valuation

RH buybacks

Membership multiple expansion potential

Conclusion

Key Takeaways

RH is an upscale retailer of home furnishings that has generated immense shareholder value since it listed in 2012. The company has compounded its stock price at 26% per annum for 11 years. What is even more impressive is that that astonishing rate of compounding is after RH’s stock price declined by 59% from the peak reached in 2021.

In the words of RH’s larger-than-life CEO, Gary Friedman, RH is “climbing the luxury mountain”, attempting to transition the company to a true luxury lifestyle brand sitting alongside the likes of Louis Vuitton, Chanel and Hermes. Not only do we believe this attainment of “true luxury” status is unlikely to ever happen, but the aggressive price increases that were implemented to elevate the brand have potentially alienated a portion of RH’s customer base and created a margin profile that we believe will prove to be illusory.

RH was a COVID-beneficiary as consumers leaned heavily into goods-based consumption during the pandemic. As a result, RH’s financial performance spiked to unprecedented levels over the last few years.

Between FY12 to FY19, and notably, prior to the pandemic, RH averaged a c.37% adjusted gross margin. During the pandemic, RH recorded adjusted gross margins of 46.8%, 49.3%, and 50.8% in FY20, FY21, and FY22, respectively. Adjusted gross profits have now been declining for five consecutive quarters. Despite this, 3Q23 LTM gross margins are still 730 bps higher than the pre-COVID average.

We would also note a deterioration in the inventory health of the company, with inventory days of 173 in 3Q23 materially above the 127 days average for the pre-pandemic period of 1Q18 to 4Q19.

Lastly, RH’s inventory value capture ratio, that is, the level of profit extracted from the company’s inventory, has materially degraded to 0.5x in 3Q23, less than half the levels of the prior year period.

The normalization of the COVID demand bump is coinciding with a period where RH is refreshing 80% of its product assortment, the largest transition in the RH lineup to date. The company must discount old stock in order to make room for the new collection, and we can readily observe 30-70% discounts in the “Sale” section of RH’s website. We believe the market is overlooking the negative gross margin impact from clearing the old stock in a soft demand environment as well as the enormous stress this transition will place on the company’s supply chain.

We suspect RH’s financial performance will get worse over the next few quarters before the business ultimately inflects as the new collection gets traction, improves inventory turns, and precipitates a top-line and FCF acceleration. While there is the potential for large upside from today’s levels, we would note a wide range of valuation outcomes and we have been unable to get comfort that a severe downside scenario is off the table, particularly given the company’s 3.5x leverage ratio. This high level of financial leverage, combined with a fluid demand environment and the operating leverage inherent in a brick-and-mortar retailer, elongates the left tail of future value outcomes in a way that we simply cannot get comfortable with.

Introduction

Amancio Ortega of Zara. The Walton family of Walmart. Tadashi Yanai of Uniqlo. They have a collective wealth of over $300 billion and are amongst the top 50 wealthiest people in the world. They also generated their fortunes as retailers. The wealth creation algorithm in the world of retail typically follows a similar pattern: 1) create a store concept that resonates with consumers; and 2) open more stores to introduce the store concept to a greater number of consumers. Provided the store unit economics are sound and don’t drastically degrade with scale, this can be an incredible formula for wealth generation.

At first glance, it might appear that RH (NYSE: RH), formerly known as Restoration Hardware, might be following a similar strategy. For starters, there has been immense value creation. RH listed on November 1, 2012, at a price of $24 per share. At the current price of $305 per share1, this means that RH has compounded its stock price at 26% per annum for 11 years. What is even more impressive is that that astonishing rate of compounding is after RH’s stock price declined by 59% from the peak reached in 2021.

Source: Koyfin (Bristlemoon readers can get 20% off a Koyfin subscription via this link)

The company’s revenues have increased 3x over the last decade, rising from c.$1.2 billion in FY12 to around $3.6 billion in FY22. It would be easy to believe that RH is following the tried-and-true retail store footprint expansion playbook. There’s a catch, however. The number of RH Galleries2 actually declined over that period. This speaks to the atypical retail strategy followed by RH, guided by the bold vision of CEO Gary Friedman.

While RH is indeed opening grandiose stores, which they refer to as Galleries, they are also shuttering legacy locations that no longer reflect the brand ethos of the company. As Friedman puts it, RH is “climbing the luxury mountain”, taking what was once a destitute retailer and attempting to transform it into a true luxury lifestyle brand. A quick comparison of the storefronts of the original Restoration Hardware concept with the new RH Galleries makes the magnitude of the transformation apparent.

Here is a photo of the original Restoration Hardware store in Eureka, California.

Source: YouTube via Ben Ramirez

And here is a photo of the RH Marin Gallery which opened in 2020.

Source: RH

There is debate over whether this elevation strategy will succeed and whether RH can ultimately join the ranks of luxury powerhouses like LVMH, Chanel and Hermes. We will dig into this debate.

The history of RH is fascinating and relevant in contextualizing the significance of this store transformation, and the pivotal role Gary Friedman has played in orchestrating this strategy.

Business History

The original Restoration Hardware

RH was born from the humble beginnings of Restoration Hardware, a company that was far from anything considered luxury. The original incarnation of Restoration Hardware, started by Stephen Gordon in 1979 in Eureka, California, is unrecognizable from the business of RH today. Restoration Hardware sold quirky items that founder Stephen Gordon would write folksy descriptions for, such as the Original Russian Forever Flashlight and the Bite The Man dog toy. The original Restoration Hardware assortment of kitschy, nostalgic wares included a garden gnome named “Aqua-Troll” that would sprinkle water once connected to a garden hose.

Source: The Original Russian Forever Flashlight via WorthPoint

The original business subsisted off impulse-driven purchases (customers were buying based on novelty as opposed to necessity), was highly seasonal (Q4 was their only profitable quarter due to holiday season gift purchases), had convoluted brand positioning with high-end goods dispersed amongst bargain-basement products, and had anemic profitability (in 1998, the year the business went public, it eked out a 1.8% profit margin and then became loss-making again in 1999). Gary Friedman acknowledged the confused customer value proposition, commenting on the 2Q05 earnings call: “If you think about the perimeter walls in Restoration Hardware in 2001, 80% of the perimeter walls did not represent a core business”.

Who is Gary Friedman?

Gary Friedman is a larger-than-life figure who is pivotal in the RH story. Friedman did not come from luxury. Rather, he had a difficult upbringing. His father died when he was five, and his mother had bi-polar and schizophrenia whereby the most she earned in a year was $5,000. Friedman recounts how they never owned a home, nor did they ever own new furniture. In fact, they were evicted multiple times from rental properties.

Friedman’s academic track record appeared unpromising: he had a D average in junior college. The college counselor took such insult to Friedman’s academic performance that he said that Friedman attending college was wasting taxpayer dollars. Friedman subsequently dropped out of college and took a position at The Gap, replenishing the stock on the shelves. Friedman expeditiously rose through the ranks of The Gap. He became the youngest regional manager, and then the youngest district manager in the company’s history, where he presided over 63 stores.

Friedman was then offered a senior position at Williams-Sonoma, prompting him to join the specialty retailer of high-end products for the home as Senior Vice President of Stores and Operations in 1988. He once again swiftly ascended the ranks, getting promoted to the President of Williams-Sonoma and Pottery Barn brands, Chief Merchandise Officer, and then ultimately the President and Chief Operating Officer of Williams-Sonoma. During Friedman's time at Williams-Sonoma, Pottery Barn (owned by Williams-Sonoma) went from a $50 million tabletop and accessories business to a more than $1 billion home furnishings lifestyle brand3.

How did Gary Friedman end up at Restoration Hardware?

Gary Friedman was being groomed for the CEO position at Williams-Sonoma, which he recounts was verbally promised to him by Howard Lester, the Chairman and CEO of Williams-Sonoma. Friedman, however, was passed over for the CEO position in favor of a company outsider, Dale Hilpert.

“Kid, no one’s going to be the CEO but you. You’ve made me a wealthy man. And then one day he hired somebody 25 years older than me to be the CEO and it broke my heart…I just knew that there was a bond that was broken and a level of trust that was broken” – Gary Friedman.

Friedman resigned from Williams-Sonoma after 13 years at the retailer to join Restoration Hardware as the CEO in 2001, a business that Williams-Sonoma almost bought two years prior. He had walked away from $50 million worth of stock options at Williams-Sonoma4. Many at the time thought the move was utterly insane. Restoration Hardware had a market capitalization of roughly $20 million when Friedman joined and had just breached a debt covenant. According to Friedman, “people were waiting for it to go bankrupt”. Friedman desperately needed to raise money to recapitalize the business (he had no prior experience in raising money, however). He put roughly $5 million of his own money into the business – which at the time was almost everything he had – and called a few friends who invested an additional $10 million.

Friedman touched on his rationale for the move: “I had always thought that there was an opportunity for a premium home-brand in the space”5. For Friedman, Restoration Hardware was merely a vessel for him to enact his long-term vision of creating a luxury home brand. The company had to raise equity three times in the first year in order to stay in business. As Friedman recalled, “we almost went bankrupt here at least a dozen times. In that first ten years we managed this company on the edge of bankruptcy. We had to dig it out of the grave”. It is difficult to fathom how stressful and tumultuous this period would have been.

The private era

The business improved and became profitable in 2004 but soon flipped back to a loss in 2005. The market punished Restoration Hardware’s stock, driving it down from $9 to $3. It was at this point that Catterton Partners, a private equity firm, looked to buyout the company for $267 million. The purchase consideration was structured as $6.70 per share in cash for the home décor chain, a 150% premium to the pre-announcement stock price. Gary Friedman and several institutional shareholders were also participating in the transaction. Catterton Partners later reduced the transaction price by one-third to $4.50 per share in cash, citing pressure in the home goods retail sector. The deal closed in June 2008, with Restoration Hardware’s stock ceasing to trade on the NASDAQ.

As a private company, Friedman pushed to reposition the company as a more upscale brand. Originally in 1998, Restoration Hardware was targeting consumers with $75,000 in household income. The company would later target higher-income households as per its 2012 S-1 filing: “We target households with incomes of $200,000 and higher, which we believe drive a disproportionate share of spending in the home furnishings market”. As part of this change to shift away from the prior brand, the company changed its name to RH. The company also made a push to establish direct relationships with its suppliers, as opposed to going through wholesaler intermediaries who would take their own margin and bloat costs.

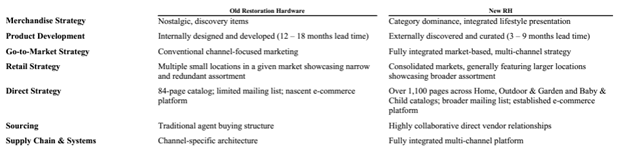

As a private company, RH was able to accelerate the transformation of their business and brand, with the strategy shift tabulated in their 2012 S-1 [page 96]:

Source: Company filings

RH eventually became public again, listing on the NYSE in November 2012, and it has been pursuing its brand elevation strategy as a public company ever since.

Business Overview

RH is primarily a retailer of home furnishings. The company sells merchandise across a number of categories, including furniture, lighting, textiles, bathware, décor, outdoor and garden, and baby, child and teen furnishings. Furniture comprised 69% of RH’s FY22 sales mix, with 31% coming from non-furniture categories. RH showcases its product assortment in what it calls Galleries (these are large, upscale, visually-striking stores), with the company’s website and Sourcebooks acting as virtual and physical extensions of RH’s physical spaces, respectively. Below are some examples of how products are presented in RH Galleries.

Source: RH

RH store formats

RH’s stores are the heart of its business. The company refers to its stores as Galleries, and they are engineered to reinforce a luxury brand aesthetic. Newer Galleries are often housed in grand, historic buildings, and feature fully appointed rooms that emphasize collections over individual pieces. RH isn’t just selling furniture; they’re conceptualizing and selling spaces. The company’s stores allow customers to visualize and aspire to the luxury lifestyle these collections convey. RH has a number of store formats which include Design Galleries, Legacy Galleries, as well as RH Outlets.

Below we can see the average square footage of RH’s various store formats. Notably, total retail leased square footage per store has almost doubled over the last decade – increasing from 10,817 square feet per store in FY12 to 21,346 square feet per store in FY22 – as RH transitions to larger format Galleries.

Source: Bristlemoon Capital; Company filings

As of 3Q23 RH had 36 Legacy Galleries, comprising 53% of the company’s total Galleries. Legacy Galleries are the older format RH store that have approximately 6,000 to 8,000 square feet of selling space (7,400 average leased selling square footage per store for FY22) and are often located in premium shopping malls and street locations. These Legacy Galleries are only capable of presenting less than 10% of RH’s total product assortment. RH found that products that were presented in a physical RH Gallery would sell 50% to 150% better than products that were only displayed online and in catalogs. This was one of the reasons behind RH transitioning its store base to larger format stores that the company refers to as Design Galleries, allowing it to display more of its product range.

“we're not taking them and just remodeling them. We're not taking them and making them 20% bigger or 50% bigger. We're making them like 500% bigger. And they're really the most exciting and interactive and experiential and dominant physical experiences of their kind in our industry today across any category, I'd argue.” – Gary Friedman [4Q21 Earnings Call] [referring to the Design Gallery concept].

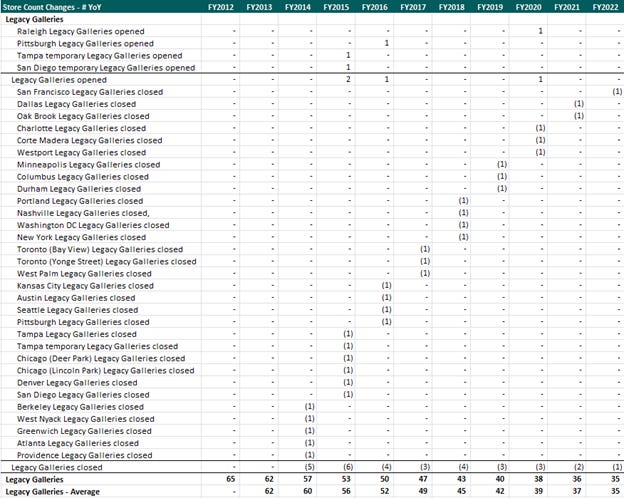

We can see in the below table the Legacy Galleries that RH has closed:

Source: Bristlemoon Capital; Company filings

RH had 28 Design Galleries as of 3Q23, comprising 41% of total RH Galleries (n.b.: the Design Gallery and Legacy Gallery sales mix numbers don’t sum to 100% as there are also Modern Galleries, as well as Baby & Child and TEEN Galleries). Design Galleries are 3-5x larger than the company’s Legacy Galleries. They allow RH to not only display a greater percentage of its assortment and improve sell-through rates, but they also act as a statement for the brand. Most of RH’s new Galleries incorporate a hospitality experience, with rooftop restaurants and wine bars. This is strategically masterful: the company is combining well-executed restaurant concepts that have a relatively high purchase frequency, with the very low purchase frequency of the company’s core furniture and homeware products. This drives incremental foot traffic to RH’s stores that can spark inspiration for patrons to refresh the interior of their homes, or to introduce new people to the brand.

Below is a table showing the markets in which RH has been opening Design Galleries:

Source: Bristlemoon Capital; Company filings

The company has been opening Design Galleries and then closing any neighboring Legacy Galleries. RH has consistently said that this strategy leads to the newly opened Design Galleries ramping up to double the average sales of the shuttered Legacy Gallery within the first few years. On the 2Q19 earnings call Friedman said there was also a 10% to 20% lift in online sales associated with this store format transition. This store transformation opportunity has contributed to RH’s sales growth and the incremental sales volumes provide leverage on the company’s fixed cost base.

“But we have -- in our average legacy galleries, we have an average volume of $15 million. But everywhere we open new galleries, especially now that we have the restaurants and the incremental traffic it brings and so on and so forth, we're doubling. So if we have a $15 million gallery, it generally turns into a $30 million gallery. $20 million gallery turns into a $40 million gallery, roughly.” – Gary Friedman, 1Q22 Earnings Call

“And then if you kind of just think about the business, the last point I made there, every time we transform a legacy gallery to a design gallery and we expect in the first few years to double the business, that provides leverage across our entire platform.” – Gary Friedman, 3Q19 Earnings Call

Gary Friedman has spoken about Design Galleries generating revenues of $5 billion to $6 billion in North America, and $20 billion to $25 billion globally. Part of reaching that North America sales ambition will come from transitioning the remaining Legacy Galleries to the newer Design Gallery format to generate the abovementioned sales uplift. Importantly, this is a sales growth lever that is in the company’s control.

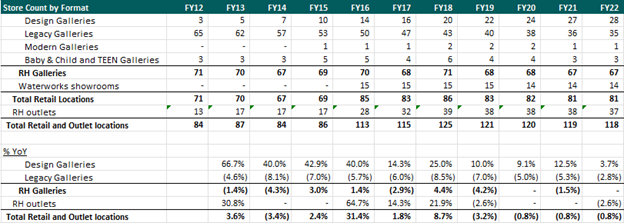

Below is the store count for the various RH store formats:

Source: Bristlemoon Capital; Company filings

Store unit economics

RH in its 2012 S-1 noted that for its Design Galleries, it targeted an average payback period of approximately 20 months on the initial investment. This is a very attractive payback period and appears to have been maintained with later Galleries that have been opened. Gary Friedman, on a September 2018 call, commented on the New York City Meatpacking Gallery having a payback period of “just under two years or right around two years”. The favorable store unit economics are reflected in the fantastic returns on incremental capital achieved by RH, which we will discuss later in the report.

The RH ecosystem

Gary Friedman has said that RH has drawn inspiration from the likes of Apple (specifically, the tech giant’s ecosystem approach revolving around a singular brand), LVMH (a true luxury platform capable of earning luxury margins), and Berkshire Hathaway (a dutiful allocator of capital). Below is a visual depiction of the RH ecosystem.

Source: Bristlemoon Capital; Company filings