TransDigm (TDG) – The King of Aerospace Private Equity

The blueprint for a 2,880x return

Welcome to Bristlemoon Capital! We have written previously on the AI bubble, FICO, GOOGL, ASML, SNPS, UNH, META, GRND, HEM SS, MELI, U, APP, PDD, IBKR, PAR, AER, PINS, BROS, MTCH, CPRT, RH, EYE, and TTD.

If you haven’t subscribed, you can join 5,449 others who enjoy our deep dives and investment insights here:

Free subscribers will only receive a partial preview of our reports. The remainder of our reports, which contain the deeper analysis, are reserved for paid subscribers. Consider becoming a paid subscriber for full access to our reports.

Bristlemoon readers can also enjoy a free trial of the Tegus expert call library via this link.

Australian wholesale investors looking to invest in the Bristlemoon Global Fund can do so via this link.

Introduction

Private equity in public markets – it’s a phrase often used by fund managers, and one that borders on being trite. But it’s no wonder that fund managers tend to overuse the expression – private equity as an asset class has performed decently well. The Cambridge Associates US Private Equity Index achieved a pooled annual net return of 12.09% over the last 25 years, compared to the annualized returns of 8.46% and 9.38% for the Russell 2000 and the S&P 500 indices, respectively[1].

There is, however, a publicly listed company that has implemented the “private equity in public markets” concept better than anyone else. That company is TransDigm (TDG), and its financial and stock price performance trounces that of even the most respectable private equity outfits.

TransDigm was formed in 1993 with initial equity of $25 million, after which not a dollar of additional equity was contributed to the company. Today, TDG’s equity value is $72 billion. In other words, TransDigm has returned 2,880x its initial invested equity.

Since its 2006 IPO, the stock has increased from $21 per share to $1,270 per share, a 23.1% annualized return for almost 20 years! This has been supported by revenues and earnings growing at 17% and 23%, respectively, over the last 20 years. TransDigm, with these numbers, is one of the all-time great stock market compounding stories.

We will look at what makes TransDigm a phenomenal business, some of the risks inherent in the company’s approach to achieving such stellar results, and what the future could hold for TDG.

Business Overview

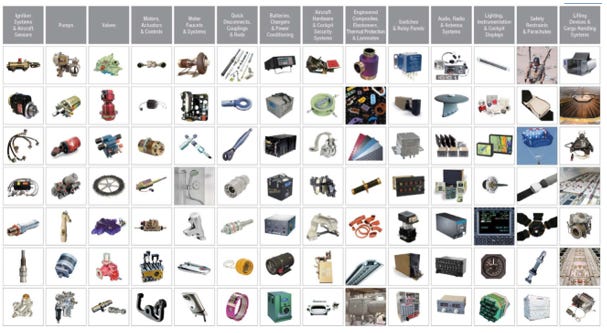

TransDigm is a designer, producer, and supplier of highly engineered aircraft components. In fact, the company sells its components into nearly every commercial and military aircraft worldwide. If you’ve ever boarded a plane, it’s a virtual certainty that you’ve interacted with one of their many products.

TDG’s products are numerous and varied, with the company supplying components such as aircraft passenger seatbelts, cockpit security systems, actuators, and the list goes on. Below is an overview of TDG’s products.

Source: 2024 TransDigm Analyst Day

TDG’s business is organized into three segments:

Power & Control – includes operations that make components and systems to provide power to or control the power of the aircraft using electronic, fluid, power and mechanical motion control technologies. This includes products such as mechanical actuators, ignition systems, specialized pumps and valves, batteries, etc.

Airframe – includes operations that make products used in airframe applications. This could be latching and locking devices, connectors, cockpit displays, lavatory components, seat belts, thermal protection and insulation. In addition to systems and components, TDG also has some services based businesses such as wind tunnel and jet engine testing services, and equipment testing solutions.

Non-aviation - includes seat belts for ground transportation, actuators and controls for space applications, parts for gas turbines, and refueling systems for heavy equipment used in the mining and construction industries.

TDG’s operating units sell components into the original equipment and aftermarket channels. Their customers include OEMs such as Boeing and Airbus, suppliers that sell to the OEMs, airlines, third party maintenance suppliers, and military buying agencies.

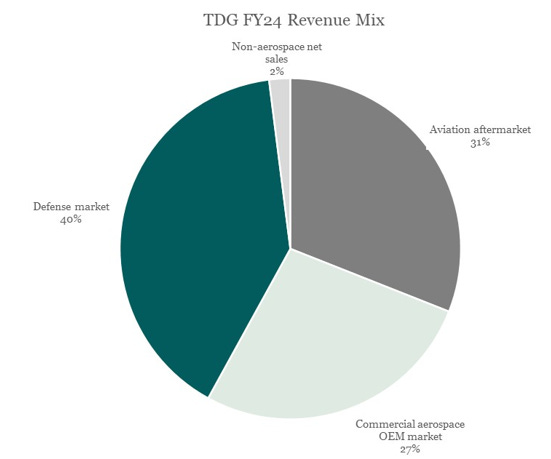

Below is a snapshot of TDG’s revenue mix by end market for FY24.

Source: Bristlemoon Capital; company filings

It is worth noting that TransDigm is a holding company that owns a collection of mostly aerospace component suppliers. Each business operates separately under its own brand, as opposed to going to market under the TransDigm name (we touch on this highly decentralized approach below). Importantly, all of these businesses have been acquired.

Private equity approach

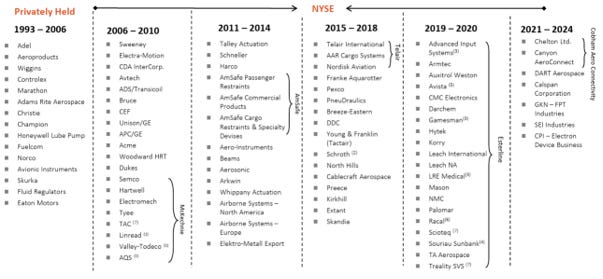

TransDigm is essentially a private equity firm that specializes in the aerospace industry. Since its founding in 1993, TransDigm has acquired more than 90 businesses. Today, these acquired businesses are split into 51 independently run operating units that collectively produce parts for nearly every commercial and military aircraft platform.

Below is a history of the numerous acquisitions TDG has made both as a private company as well as after it went public.

Source: 2024 TransDigm Analyst Day

The company employs significant leverage to enact its acquisitive growth strategy, running net debt / EBITDA at almost 6x on average for the last 10 years. Usually this significant level of leverage would concern us and rule out the company as an investment prospect.

We’d point to two things that give us comfort: 1) TDG derives a significant portion of its earnings from the aftermarket (c.3/4 of adjusted EBITDA comes from the aftermarket), which is a much more stable earnings stream; and 2) the business navigated and survived two of the most severe exogenous shocks (the GFC and COVID), testing their highly levered strategy and showing that their model can withstand material demand shocks and credit crunches. Aside from a -6% EBITDA decline in FY20 and -4% in FY21, TDG has never experienced a full-year EBITDA decline, hinting at a well-managed, resilient business that is capable of supporting elevated amounts of leverage.

OEM and aftermarket

TDG sells its products into original equipment manufacturer (OEM) markets as well as the aftermarket. TDG supplies components to OEMs which include the major global aircraft manufacturers (e.g., commercial aircraft manufacturers such as Boeing and Airbus, as well as private aircraft manufacturers like Gulfstream, Bombardier and Cessna) and defense contractors (e.g., Lockheed Martin and Northrop Grumman). Often, however, TDG is selling products to other suppliers, who then sell to companies such as Boeing and Airbus.

The OEM market is defined as the sale of components to the aircraft manufacturer (or related suppliers that sell to that aircraft manufacturer) for the production and initial delivery of new aircraft.

The aftermarket, on the other hand, refers to the supply of replacement parts for aircraft that are already in operation. It is a much more stable stream of revenues that is correlated to the distance flown by aircraft; revenue passenger kilometers (RPKs) have grown at 5-6% for decades, providing a nice demand tailwind. In other words, more flight hours lead to more wear on an aircraft’s components, necessitating periodic replacement of those parts.

It is worth noting that the aerospace industry follows a two tier pricing model. The OEMs (e.g., Airbus and Boeing, or a supplier selling into these firms) pay TDG one price for the original part and additional warranty parts. The OEMs exert their duopolistic leverage over the aerospace supply chain to push down the prices they pay for these parts so that they can improve the margin they make on selling planes.

These planes are then sold to airlines, who are then responsible for purchasing aftermarket replacement parts at a higher price than what the OEMs initially paid. Sometimes there are long-term agreements (LTAs) that specify the aftermarket pricing that TDG can charge, but typically there’s flexibility for TDG to exercise its pricing power in the aftermarket.

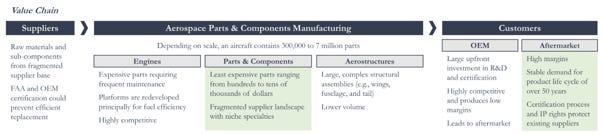

The graphic below gives a snapshot of the aerospace value chain and highlights where TDG derives the bulk of its earnings from.

Source: Compounding Labs

In essence, the OEM market is where TDG gets its proprietary parts designed into a platform, securing an annuity-like revenue stream for the decades-long aftermarket phase (which is much higher margin than selling to the OEM market). In this way, TransDigm is implementing a razor razor-blade model: sell the parts cheaply upfront and make the margin on the long tail of replacement demand for that part (note that TDG’s philosophy is that you don’t have to lose money on the upfront sale to the OEMs, even if many other suppliers do).

In the original 2003 investment memo from Berkshire Partners when they were looking to acquire the then-private TransDigm, it was estimated that the company will usually achieve $100 of aftermarket sales over the lifespan of an aircraft from each $1 of OEM sales[2]. This long-tail of high margin replacement demand is one of the most attractive aspects of TransDigm’s business.

Why TransDigm is a Great Business

There are reasons why TransDigm’s aftermarket-focused strategy has worked spectacularly well. Essentially, the businesses TDG has acquired have unique characteristics that have enabled the company to raise the prices of its products over long stretches of time without customers switching to other suppliers. We will dig into each of these characteristics in turn.