Unity Software (U) – AppLovin at home?

Can Unity replicate some of AppLovin's success?

Welcome to Bristlemoon Capital! We have written previously on APP, PDD, IBKR, PAR, AER, PINS, BROS, MTCH, CPRT, RH, EYE, TTD, and META. If you haven’t subscribed, you can join 3,747 others who enjoy our deep dives and investment insights here:

Free subscribers will only receive a partial preview of our reports. The remainder of our reports, which contain the deeper analysis, are reserved for paid subscribers. Consider becoming a paid subscriber for full access to our reports.

Bristlemoon readers can also enjoy a free trial of the Tegus expert call library via this link.

Introduction

Unity Software is a company that we have followed on and off since its IPO in September 2020. We have always thought that Unity as a business had tremendous potential, with the dominant engine for creating real-time 3D content and a highly complementary mobile ad network for monetizing said content. But from an all-time high of $201 to an all-time low of $14, Unity has been an unmitigated disaster for shareholders over the past three years.

Anyone familiar with Unity will know that the business does not fit any definition of quality. Nor does it belong in the growth bucket, having seen revenue growth decelerate from over 40% in the three years through 2021, to a -14% decline in the YTD Q3 2024. So why has Unity resurfaced on our radar?

Following our extensive work on AppLovin and the success that stock has had, we decided to dust off and refresh our thesis on Unity. This was an efficient way to both leverage and further build upon our knowledge of digital advertising. We were also looking for any evidence that Unity’s ad monetization business might stage a turnaround and catch some of the excitement that currently surrounds AppLovin. For anyone that remembers, Unity Ads was by far the largest tier 2 mobile ad network behind Google and Facebook, before the rise and rise of AppLovin.

The deep dive that follows is part analysis of how Unity got into the mess that it’s currently in, and part speculation about how the company might rebuild its key businesses and make a return to growth. While writing this piece, we also uncovered some new facts that change our perception of Unity’s turnaround, which we share in the interest of transparency.

Table of contents

Business overview

Create Solutions

Grow Solutions

An end-to-end solution for developers

Where did Unity go wrong?

Gaming industry layoffs

The Runtime fee debacle

App Tracking Transparency and IDFA deprecation

Poor capital allocation, R&D and M&A malinvestment

The path to recovery?

Resets everywhere

Can Unity create upside for Create?

Small core game engine market

Expansion into industry

Pricing power is mixed

Still the dominant game engine for mobile

How does Grow get back to growth?

Sizing the market opportunity

How mediation changed the mobile advertising landscape

The path dependency of Unity Ads

Can Unity rebuild its ad network?

Concluding thoughts

Business overview

Unity is a leading platform for the creation, operation and monetization of real-time 3D (RT3D) content, primarily in the form of mobile games. The business is comprised of two segments: Create Solutions, which houses the Unity Editor, a software platform for building and deploying interactive 3D experiences; and Grow Solutions, a mobile ad network for user acquisition and app monetization. Together, these two complementary assets offer developers the only end-to-end solution from ideation to monetization available in the market.

Create Solutions

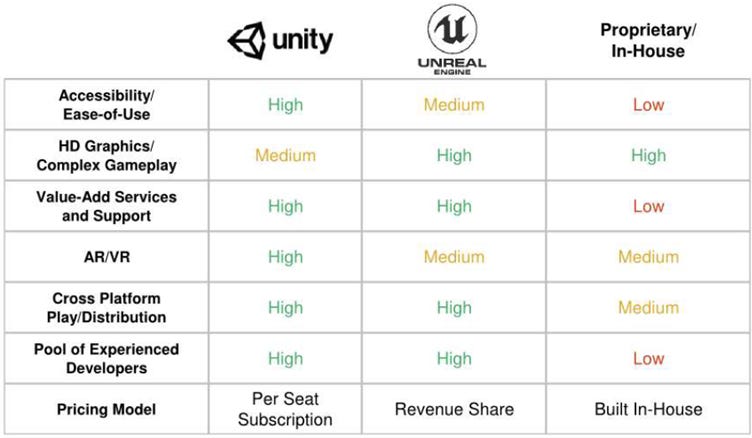

The Unity Editor is the world’s most popular RT3D engine a.k.a. “game engine” (we use the terms interchangeably). Over 60% of the world’s mobile games are developed with Unity, including 70% of the top 1,000 games, and applications made with Unity are downloaded 3.7 billion times a month on average[1]. While the dominant use case of the engine is game development, its range of applications extends well beyond gaming into industries such as aerospace, automotive, construction, manufacturing and retail. Unity is also the leading engine for AR/VR content, a category that has endured a long post-COVID winter but may gradually thaw thanks to Meta’s Quest and Orion efforts.

The third-party (i.e. not in-house) game engine market can be considered a duopoly between Unity and Unreal (owned by Fortnite developer Epic Games), though the two largely swim in their own lanes. Unreal Engine is known for being a more performant engine producing higher fidelity graphics favored by AAA console and PC developers. Unity, on the other hand, is generally regarded as more beginner- and developer-friendly, less hardware intensive (perfect for mobile), and has better community support with over 1.1 million monthly active developers[2]. Games made with Unity can also be deployed to over 20 platforms including PC and most console and VR platforms, making the engine ideal for cross-platform deployments.

Source: Morgan Stanley

Unity monetizes the engine through a freemium SaaS model, charging a tiered per-seat subscription. This differs from Unreal which charges a royalty rate on gross game revenue of up to 5% – an important distinction that we will return to. As of January 1, 2025, Unity offers three pricing plans for game developers from free to several thousand dollars a year, and an Industry plan that all non-gaming customers must use. A “Plus” plan for $399/yr was retired in September 2023, with plan subscribers up or downgrading to Pro or Personal upon annual renewal.

Source: Unity website

Despite the obvious mission criticality of the Unity Editor to customers, Create segment revenue was only 31% of total revenue in the trailing twelve months (TTM) to Q3 2024. This is unchanged from 2019, the year prior to Unity’s IPO, when Create was also 31% of total revenue albeit under slightly different segmentation. What’s perhaps more surprising is that the dollar revenues – $169 million in 2019 and $418 million in TTM Q3 2024 after adjusting for an estimated 20% non-gaming revenue – represent less than a 40 bps take rate of the $100+ billion mobile gaming industry revenues.

Source: Bristlemoon Capital; Company filings. Note resegmentation in 2022, ironSource acquisition in 2023, Strategic portfolio revenue only in 2023 and 9M 2024

Source: Bristlemoon Capital; Data.ai

We believe that a substantial majority of Unity developers are using the engine for free on a Personal plan. The Unity S-1 disclosed that over two-thirds of Create revenue in 2019 came from the $1,500/yr Pro plan. Assuming the remaining less than one-third of revenue is split between Plus and Enterprise, Unity had somewhere around 160,000 paying subscribers. The fact that the Plus plan was later discontinued suggests that it was a small contributor to revenue, as forcing a large percentage of subscription revenue to upgrade to Pro at 5x the cost or downgrade to free seems excessively risky. Applying a 10/30/60 split between legacy Plus, Enterprise & Industry, and Pro plans to TTM core Create revenue suggests around 320,000 of the 1 million-plus Editor MAUs are paid subscribers. This could fall to less than 250,000 as the grandfathered Plus plans expire through 2025 and users either upgrade or churn.

Source: Bristlemoon Capital; Company filings

We’d also highlight that the Unity Editor includes an In-App Purchase (IAP) plug-in that simplifies IAP setup and asset deployment across multiple app stores. This plug-in, which helps developers monetize their games, is free. Yet Apple has built a tens-of-billions revenue stream from charging a 30% commission on IAP, mostly from mobile games.

The potential for Unity’s engine business to capture a greater share of mobile gaming industry economics has been a long-held bull case. From former CEO John Riccitiello on the Q3 2020 earnings call:

“So you're correct in saying that our take rate in gaming overall is not high. It's about 0.4%. When I talk to people in the industry, they have a mental picture and it must be at least 2%, 3%, 5%, 10%. I don't think they are wrong. I'm not telling you that I can get there tomorrow. I have the benefit of having been involved in publishing north of $40 billion of the games in my life, and I'll tell you the one thing I hated more than anything was a royalty model or rev share to a tool maker.”

Even though the CEO at the time was explicit about not shifting to a revenue share model, investors during the heady days of 2021 dared to dream of 1%, 2% or even 5% take rates. After all, why not? The mobile gaming industry would be a fraction of its current size without Unity, so why shouldn’t the engine business share in more than just 40 bps of industry economics?

We’ll dig into why not later, but for now let’s turn to the segment that does grow with the success of Unity’s customers.

Grow Solutions

The Grow segment (f.k.a. Operate) consists primarily of Unity’s mobile ad network which allows publishers to monetize their apps via advertising and grow their users via user acquisition (UA) campaigns. As an ad network, Unity Ads takes a share or spread on the advertising dollars that flow through the network, typically in the 20% to 30% range. If customers are growing and monetizing their games, Unity’s ad revenue should grow with its customers’ success, unlike the seat based Create revenue.

The remainder of this deep dive assumes some basic understanding of mobile ad networks. For those encountering mobile ad networks for the first time, we highly recommend pausing here and reading the AppLovin thesis in our Q3 letter which goes into some detail about how these ad networks operate.

The short version is that a mobile ad network connects advertisers looking to promote their app/product/brand with app publishers who have advertising space to sell. The more inventory a network has available to sell and the stronger its user targeting capabilities are, the more advertising dollars it will attract. In the context of Unity Ads or AppLovin, these ad networks predominantly serve mobile game publishers in monetization and user acquisition.

Source: Bristlemoon Capital

Publishers who monetize via ads will prioritize ad networks that provide the highest effective cost per mille (eCPM) or revenue per thousand impressions sold, at the highest fill rates. UA advertisers will allocate budgets to the ad networks that provide the best return on ad spend (ROAS) at the requisite scale, be it the lowest cost per action or some interim target like Day 1 or Day 7 ROAS.

An end-to-end solution for developers

Unity is in an advantaged position of being the only business in the industry with an end-to-end solution that can support the entire game development cycle from initial idea through to monetization. There are few scaled game engines and dozens of ad networks, but only Unity can integrate the pre-launch creative workflow with post-launch operation and monetization.

The synergies should be clear: a majority of mobile games are developed with Unity, and a majority of these developers form the long tail of the mobile game development industry. According to a former Global Program Manager at Unity on Tegus, 85% to 90% of all games are created by small teams of two to four developers, and only 10% from large publishers. These small developers typically don’t have a marketing/revenue officer and without prior experience managing multiple ad networks, Unity Ads is the obvious default choice. Even large publishers with the infrastructure to manage multiple ad networks will still have Unity Ads in their mediation stacks – an important topic we will cover in detail later.

“So given the fact that like 85%, 90% of all game developers are these small, medium-sized teams, two to four people and most of the games volume-wise being published and launched are new games. What they don't have on their team is a marketing person. They basically just have developers and then when the game is finished and it comes time to choosing the ad networks, typically, if there is an easy choice just to get started to monetize, that's the choice that they can prefer. And this is why Unity has such a strong positioning in the market is because 50%, 60% of mobile games get built on their engine.” Former Global Program Manager at Unity on Tegus

In addition to the Editor/Ads cross-sell advantages, the game engine also provides Unity with unique data advantages that in theory could be leveraged across the ad network. Here is Unity management (and even AppLovin’s CEO) talking about the value of this data:

“Our Operate organization captures and analyzes 50 billion in-app events each day. If you do the math, that's about 35 million in-app events every minute, and we do this across 20 platforms. […] Unity's game engine leadership is a strength, and it provides us with deep context for our ads business.” Former Unity CFO on Q1 2021 earnings call

“Unity has a unique insight into how to maximize the lifetime value of the gaming consumer, and it's derived from our integral role in both the development and live operations of cross-platform games. The work we're doing to unlock those insights and to improve the gaming industry for developers and consumers alike is what motivates us here at Unity every day.” Current Unity CEO on Q3 2024 earnings call

“Create is the underlying technology in the majority of mobile games. So if you think about that, the contextual data that Unity has access to is very compelling. We also reach a lot of the mobile games in the ecosystem through our technologies on MAX and AppDiscovery, but that combination could be very compelling. And that's why Create is important to us and why we see this path of being able to unlock a lot of synergies by the complementary nature of these two complicated technologies, which could unlock a lot.” AppLovin CEO on Q2 2022 earnings call, explaining rationale behind the offer to merge with Unity

Yet, with the enviable synergies between game engine and ad network, and rich proprietary data from its dominant position in mobile game development, why has Unity been such a disaster for investors over the past three years?

Unity share price down -90% from all time high and -60% from IPO:

Source: Bloomberg

Unity sellside consensus Revenue expectations:

Source: Bloomberg. Note the spike in revenue expectations in November 2022 was due to the close of the ironSource acquisition

Unity sellside consensus EBITDA expectations:

Source: Bloomberg

For paid subscribers, we explore where Unity went wrong over the past three years, from industry headwinds to self-inflicted unforced errors in both its core businesses. We then lay out why we believe Unity now has the right assets and the right team (at least until earlier this month) in place to stage a turnaround that, if successful, could see it follow in AppLovin’s footsteps.