PAR Technology Corporation (PAR) - The Right Jockey For the Right Horse

A profit inflection on the horizon

Welcome to Bristlemoon Capital! As of 1 July, we officially launched our global long/short strategy: the Bristlemoon Global Fund. More information can be found at www.bristlemoon.com or by emailing info@bristlemoon.com. We have written previously on PINS, BROS, MTCH, CPRT, RH, EYE, TTD, and META. If you haven’t subscribed, you can join 2,459 others who enjoy our deep dives and investment insights here:

Free subscribers will only receive a partial preview of our reports. The remainder of our reports, which contain the deeper analysis, are reserved for paid subscribers. Consider becoming a paid subscriber for full access to our reports.

Bristlemoon readers can also enjoy a free trial of the Tegus expert call library via this link.

Introduction

Imagine a company that sells a mission-critical product into a durable customer base. Without that product, those customers can’t make sales. Now imagine that this mission-critical product comprises a miniscule part of the customer’s overall costs. And despite having a set of competitors that are lethargic and slow moving, the company has historically not pushed through material price increases, creating latent pricing power. That company is PAR Technology Corporation (NYSE: PAR), a $1.6 billion market cap company that we believe has strong compounding potential.

The CEO of PAR, Savneet Singh, has said that in investing “[t]here are bets that are on a market. There are bets on a business. There are bets on the jockey”[1]. We believe that PAR is a bet on all three due to 1) the digitalization of restaurants and a rapidly evolving technological landscape that is causing an increase in active RFPs as restaurants seek to upgrade their tech stack; 2) PAR’s advantaged positioning as an integrated enterprise solution that is out-executing the competitor set; and 3) a smart, driven, pragmatic CEO who has transformed the business and positioned it to accelerate market share gains.

We became interested in PAR upon hearing that it had won the Burger King contract, an RFP that every major enterprise restaurant technology company participated in. Our understanding is that Oracle’s Simphony product offered a lower price, yet Burger King still chose PAR. This was enough to pique our interest and the deeper we dug, the more we liked the PAR opportunity.

Rather than needing to identify the next Cava or Sweetgreen, PAR provides a way to buy the best-in-class enterprise restaurant technology platform that will grow as its customers roll out new units[2]. PAR’s business is royalty-like in nature: restaurant customers spend a certain percentage of their average unit volumes (AUVs) each year on software provided by PAR. We believe that not only can PAR maintain this take rate of its customers’ AUVs, but it has an opportunity to dramatically increase its take rate over time via like-for-like pricing as well as the cross-selling of additional products into its customer base. There is ample headroom for PAR to expand its take rate; a $2 million AUV restaurant would be paying PAR an infinitesimal 0.2% of its AUVs. Over time, we believe that PAR will get better at proving out the ROI its products bring to customers and be able to appropriately charge for the immense value it’s providing.

We believe PAR is capable of growing at the top-end of the company’s 20-30% ARR growth range, with the very high incremental margins potentially being underestimated by the market. If the company can hit a 30% ARR CAGR and achieve software-level margins over the next five years, there is a scenario where investors could earn a 4x multiple of invested capital (or 37% IRR) on PAR over this five-year period. But even with more conservative assumptions, we believe there’s still value in the stock.

Table of Contents

Business Overview

Business History

Financials

Temporarily depressed gross margins

Underlying opex flat

Inflection to profitability is nearing

Growth Drivers

Transition to the cloud accelerating upgrade activity

PAR’s Unified Commerce approach

ARPU expansion

Burger King contract rollout

TAM expanders

International

Risks

Valuation

Business Overview

What does PAR do?

PAR Technology Corporation (PAR) provides hardware and software solutions to the restaurant industry, with its core product being the point-of-sale (POS), a system that allows restaurants to accept payments and track sales. The company sells its products primarily to enterprise restaurant chains, spanning the quick service restaurant (QSR), fast casual, and now table service segments. The company classifies enterprise restaurants as those with more than 50 units (or strong ambitions and prospects to reach that level of scale). PAR isn’t serving your local mom-and-pop pizza restaurant.

According to the company, PAR is in almost 50% of the top 100 restaurants in America. PAR sells hardware to restaurant behemoths such as McDonald’s and Yum! Brands (owner of KFC, Pizza Hut, Taco Bell, and The Habit Burger Grill). In fact, these two brands represented 17% of the company’s FY23 revenues and PAR has been selling products to these chains for over 40 years. The company for decades was predominantly a POS hardware provider to restaurant chains but has more recently pivoted its focus to the fast-growing POS software product.

PAR sells its software to large enterprise chains such as Dairy Queen, Arby’s, Five Guys, and is currently rolling out its products to a marquee customer that was recently won: Burger King. In addition, the company also counts as customers a number of burgeoning restaurant concepts that include Sweetgreen, Cava and Big Chicken. You can think of PAR as a pick-and-shovel play on the restaurant industry: it is providing the supporting tech infrastructure that enables restaurants to run efficiently.

So, what makes PAR special? PAR isn’t just offering a point solution; it is offering a platform that ties together a range of modules that help restaurants operate. PAR offers an integrated suite of products including point-of-sale, customer engagement and loyalty, digital ordering and delivery, payment processing, and other related services. More than 700 restaurant customers use PAR’s solutions, and they are deployed across more than 70,000 active restaurant locations.

The point-of-sale (POS) is the heart of a restaurant’s tech stack. It acts as a system of record, with data from all the other modules passing through the POS. For this reason, the POS is a mission-critical piece of infrastructure for every restaurant. If the POS suffers downtime, the restaurant loses sales.

Source: Company filings

We can crudely think of a restaurant as being split between front-of-house (the customer-facing portion of the restaurant which includes POS) and back-of-house (where food preparation, storage, and business administration occurs). PAR has products that span the entire restaurant value chain, connecting the front-of-house with the back-of-house.

For example, let’s say that you place an order with a restaurant via a mobile app. The data received in the mobile app must then be fed through to the POS system which then alerts the kitchen that an order has been received. If the customer is part of that restaurant’s loyalty program, their purchase activity must interface with the loyalty solution so that they earn loyalty points. Lastly, the data from that person’s order needs to also flow into the restaurant’s accounting system, inventory management system, and then analytics in order to glean insights that can be used to run the business more efficiently.

As we can see, a customer journey for something as simple as ordering food in an app involves data passing through many different software modules. If these modules are provided by different vendors that don’t talk to each other effectively, then the restaurant is left with a suboptimal solution that is at risk of breaking, as well as suffering more downtime if something goes wrong (it is harder to coordinate patches/solutions amongst multiple vendors who often point the finger at each other).

Let’s take a look at the different PAR products so that we can properly understand what this business does.

PAR’s product suite

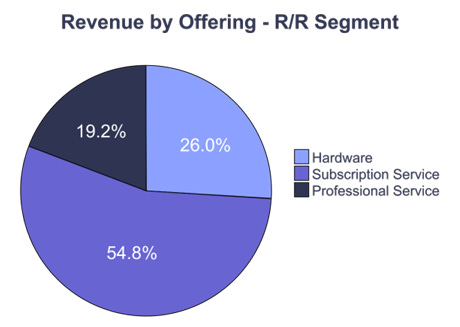

We can split PAR’s revenues broadly into three categories: 1) subscription revenues; 2) hardware; and 3) professional services. Below is the 1Q24 revenue breakout for PAR:

Source: Company filings

The most important value-driver for PAR is its subscription revenues, which have grown at a 46% annual rate over the last two years (part of this stellar growth has come from acquisitions). These software revenues have been growing much quicker than the Hardware and Professional Service segments, both of which have experienced declining revenues for the last few consecutive quarters. As such, subscription revenues as a proportion of total Restaurant/Retail revenues for PAR reached c.55% in 1Q24, up from around 28% just two years ago in FY21. The complexion of this business is rapidly changing, and we expect this trend to continue.

Within subscription revenues, the company groups its products into two segments: 1) Operator Cloud; and 2) Engagement Cloud.

Source: Company filings

Operator Cloud includes Brink POS, payments, and the Data Central product which is back-of-house reporting and labor & food management.

Engagement Cloud houses PAR’s loyalty products such as Punchh and Stuzo, as well as MENU Dispatch and MENU Online Ordering.

As of 1Q24, the ARR by subscription product line breaks down as follows:

Source: Company filings

Let’s look at each of the PAR products, what they do, and how they slot together. This might seem tedious but it’s necessary to properly understand PAR’s value proposition and why it’s so compelling for customers.

Brink POS

In September 2014, PAR acquired Brink Software Inc., a provider of cloud-based POS software for restaurants[3]. Prior to a cloud-based POS solution, restaurants needed to maintain their own on-premise server which housed the POS data, a more expensive and far less efficient setup. In fact, there are many restaurants out there today that still rely on this antiquated on-premise technology with a co-located server.

Brink POS is a cloud-based, open solution that allows PAR’s customers to accept payments. Brink POS, it should be noted, is hardware-agnostic and can run on any Windows device. Brink POS can integrate with a range of products including kiosks, kitchen video systems, and enterprise reporting. This is all done through the more than 500 integration partners that build products on top of PAR’s platform. The key point is that the Brink POS has an open API, meaning that the company’s SaaS products are extensible.

This is important to enterprise customers who might want to use third-party vendors for part of their tech stack, but still want it to integrate well with the Brink POS. Over time, however, we do expect PAR to become less open, given in recent years it has acquired products that it would surely want to support with a superior integration compared to an API with a third-party competitor solution.

Brink POS costs around $2,500 to $3,000 per store today, depending on the restaurant’s requirements[4]. The company communicated that just three years ago Brink POS cost roughly $1,900 per store[5], meaning that there’s a positive pricing mix effect as customers roll off these legacy contracts and come in at the higher rate. We believe there is enormous latent pricing power in PAR’s software suite that continues to grow as restaurants over time appreciate the better ROI of being on PAR’s integrated platform (we discuss pricing in the Growth Drivers section).

MENU

MENU is an eCommerce platform for restaurants that powers the online ordering of food across a range of digital customer touchpoints, including mobile, web, kiosk, and third-party delivery apps such as Uber Eats and DoorDash. The product is loved by customers and was a key reason why PAR was able to win the Burger King contract. There are a few things that MENU allows its restaurant customers to do:

Synchronize their menus across a range of ordering channels, with full control over the customer experience as well as retaining a direct customer relationship.

Manage orders across multiple channels.

Coordinate their delivery operations.

There are three key products that sit within MENU. The first is MENU Digital Ordering, which is basically a white-labeled mobile or web app online ordering platform that can be used on or off-premise by the restaurant. Think of it as a Squarespace equivalent for a restaurant creating their online ordering system. This could be for a website, mobile app, or an in-store ordering kiosk. The restaurant brand controls the UI/UX (as opposed to templated website designs that can be clunky) and can adjust the order flow as desired to boost average check sizes and re-order activity. Any uptick in average order ticket from the MENU system can be measured and communicated to the restaurant in terms of an ROI on their MENU spend. Crucially, all order data from these varied ordering channels is automatically synced with the POS system.

The second product is called MENU Link, which is an aggregator of third-party delivery orders from the likes of Uber Eats and DoorDash. MENU Link integrates external ordering channels into a single system for centralized order and menu management. This keeps orders from multiple delivery marketplaces in a single backend, which obviates the need for restaurant staff to use multiple tablets to deal with these orders. These delivery marketplace orders are received and automatically injected into the POS system, which reduces errors that come from otherwise having to manually record these external orders into the POS.

Lastly, there is MENU Dispatch, which allows restaurants to deploy their orders via a range of delivery channels, which might include their own drivers or third-party delivery service providers. MENU Dispatch will automatically assign orders for dispatching, and it includes tools to plan routes, assign orders, and manage drivers. Customers are also given delivery time estimates and can track their order directly from their mobile.

MENU was originally a Swiss company that PAR acquired in August of 2022. The company went through a heavy investment period to bring the MENU product to the U.S. market, a result of extremely strong customer demand. This has had a deleterious effect on consolidated margins which we will explore later in the report.

Depending on the number of MENU modules deployed by the customer, pricing for this product is around $800 to $2,400 per store per year. Selling the MENU product into the Brink POS customer base has the potential to result in a material uplift in customer ARR. For example, a customer combining Brink POS and MENU might be paying $5,400 per store, an 80% ARR uplift over the $3,000 per store they might be paying for the standalone Brink POS product. This highlights the significant ARR growth potential if PAR’s land-and-expand strategy continues to build momentum.

Punchh

Punchh is an enterprise grade customer loyalty and engagement solution. When customers are enrolled in a loyalty program, the restaurant can capture valuable data on their behavior and preferences. This allows restaurants to engage with customers on a deeper level via personalized messaging, exclusive rewards, and tailored offers. At its core, a loyalty program is about customer retention and incentivizing return visits. To the extent that a successful loyalty program can drive additional purchases without incurring expensive promotional costs to win new customers, then this can boost the customer lifetime value and sales of a restaurant.

Punchh makes a lot of strategic sense within PAR’s product stable, particularly its integration with MENU. By combining digital ordering from MENU with Punchh’s loyalty offerings, guests can redeem loyalty rewards across mobile, web and kiosk ordering channels. This provides a better customer experience and benefits the restaurant by having all customer insights available from a single system. The Punchh product costs around $1,000 per store per year.

There are also synergies between PAR’s payment product and its loyalty solution. Savneet communicated at the J.P. Morgan Global Technology Conference in 2023 the following:

“in our loyalty products, we now have a product called Single Scan Flow, which would literally, one tap, what we call a single scan, you can pay for your transaction, earn points or whatever the unit of loyalty is, but also redeem whatever coupon you might have, all in one tap. And so, you're not sort of going, here is my coupon, here's my credit card, here's my loyalty number. It's all in one tap.”

PAR Payment Services

Unlike the majority of PAR’s other products which were acquired, PAR’s payments product was built internally. PAR Pay is a payment facilitator (often abbreviated as PayFac). Basically, it is a payment service provider that allows its restaurant customers to accept electronic payments. PayFacs have a master merchant account and a master Merchant ID (MID) with acquiring banks. Restaurants that choose PAR’s payment solution setup a sub-merchant account and run their transactions under PAR’s MID. This simplifies the onboarding processing, making it quicker and simpler. The flipside for PAR is that they take on credit risk (although this is a non-issue given the resilient, enterprise restaurant customer base where fraud and defaults are exceedingly rare).

The funds are aggregated across merchants in a pooled account. This allows PAR to get more competitive pricing on the interchange rate, which they then mark up by a few cents. Notably, most of PAR’s payments monetization is by taking a fixed fee on transactions, not one that scales as a percentage of gross payment volumes (GPVs). This is an important point. PAR’s fixed fee monetization is in stark contrast with a company such as Toast (NYSE: TOST), which plays in the SMB space and takes a clip of its customers’ GPVs. Toast takes a roughly 2.5% slice of its customers GPVs, and these gross transaction-based fees comprise 82% of Toast’s revenue mix (note that Toast recognizes its payments on a gross-basis, while PAR recognizes its payment revenues on a net basis).

Here's the problem for Toast and why we believe it is unlikely that the company will be able to push up the customer stack from SMBs into enterprise chains: large-scale restaurants will refuse to pay the high fees Toast gets away with charging its SMB customers. We will explore this further in the Risks section.

PAR Pay is still a nascent business but is growing strongly. In 4Q23, PAR achieved a GPV annual run rate of $2.1 billion. PAR management noted on the 3Q23 earnings call that payments ARR more than doubled year-over-year, and the majority of MENU signings included Payments attachment. Furthermore, on the 2Q23 earnings call CEO Savneet Singh disclosed an 80% attach rate of PAR Pay to Brink deals. This is the cross-selling/upselling strategy in action, with PAR Payments an important driver of this. In fact, at the Evercore ISI Payments & FinTech Innovators Forum in February 2024, Savneet commented that the portion of PAR’s ARR growth that has come from upselling has come primarily from Payments. If this high PAR Pay attach rate can sustain, it means that future deals will come in at significantly higher ARRs per site.

The company frames its Payments revenues as “transactional ARR” which can range between $1,000-$2,000 per year for a restaurant store, depending on volumes. As mentioned, PAR’s Payments revenues are recognized on a net basis and are thus very high margin, with gross margins expected to get north of 70%.

We would lastly note that by having a customer use PAR for payments, it helps PAR better address problems that can arise from payment-related issues. Savneet has in the past noted that 40% of PAR’s service calls were for payment issues[6], and that by owning the payments product PAR could provide its restaurant customers with a better experience.

Data Central

Data Central is a back-office solution used to manage inventory and labor, as well as perform enterprise reporting. Think of Data Central as a central hub that collects data from the POS, inventory, supply, payroll, and accounting systems, and then spits out actionable insights and reports. The aim of this software is to help restaurants better understand and manage their operations more efficiently. Notably the solution is POS-agnostic: you don’t have to use PAR’s Brink POS to use Data Central. The Data Central product costs around $1,500 per store annually.

Hardware

In addition to the software modules discussed above, PAR also sells hardware such as terminals, tablets, headsets, and kitchen display systems. Brink POS software needs hardware to run, and software purists will say that this hurts the ability of PAR to scale up quickly. This is true, but it also makes it a more difficult business to enter. We anticipate PAR’s hardware business to progressively shrink as a portion of total revenues, given the much stronger growth in the software segment.

Sale of the government business

PAR has a legacy Government division which comprises one-third of PAR’s consolidated revenues. Investors have long expected a sale of the Government business, and PAR even updated its 2023 10-K to include wording that made it apparent that a sale of the Government segment was being explored. On June 10, 2024, PAR announced that its Government subsidiaries were being sold to Booz Allen Hamilton (NYSE: BAH) and NexTech Solutions Holdings for a combined total of $102 million.

While the sale price maybe fell short of expectations, we view the sale as a good outcome. The Government business was an uninteresting distraction that muddied the PAR story and likely provided a multiple overhang. For example, the Government operating segment came in at a measly 6.4% gross margin in FY23, depressing PAR’s overall gross margin profile (although notably the government segment was cash flow positive and in effect subsidizing the loss-making software business).

We expect that the sale of the business will attract more software investors to the PAR story and over time support multiple expansion as the software business can prove its standalone financial viability. PAR will become a restaurant pureplay which broadens the investor base, it removes a management team distraction with having to manage a non-core legacy business, and it also provides a cash infusion.

Very durable customer base

PAR is selling its products into one of the most robust customer bases that exist. Consider the following quote from CEO Savneet Singh at the Evercore ISI Conference in February 2024:

“Some of our customers measure the length of their franchisees in decades. So it's like, are you 1.5? Are you a 2.5? It's not even years. I mean these are really, really durable business that go from family to family….And so again, they're so sticky. And in times of economic uncertainty, they tend to do better because they're more cost-effective foods.”

This translates into very low levels of churn: PAR’s churn levels are currently around 4%, and most of these are just store unit closures as opposed to logo losses. When these enterprise restaurant chains close a store, they often re-open that store in a nearby location. If we were to adjust the churn numbers to account for store relocation activity, then churn levels would be even lower. During the pandemic churn levels spiked to 14% but by the end of 2020 it was back down to 7%. Almost all of PAR’s customers came back, speaking to the strength of their value proposition.

Who makes the purchasing decisions?

The buyer of PAR’s products is generally the CIO, with some CMO involvement for the Engagement Cloud loyalty products. Historically, the CIO would benchmark POS vendors on price and then pick the cheapest one that wouldn’t break. This is changing as restaurants re-think their tech stacks as what were traditionally cost centers, and better understand their potential to be profit drivers. Increasingly there has been CEO involvement in these purchase decisions. This is because digital sales are becoming more important to restaurants’ growth plans, forming part of the restaurant’s strategy that has CEO oversight. There are a number of things that restaurants consider when choosing their software vendors:

Ease of integration.

Intuitive user interface (the people that are using the hardware at the restaurant level often are not very technical).

Customizability.

Other functionality such as sales reporting.

Customer support.

Scalability.

Security.

So why did PAR win Burger King? We heard from the Director of IT Governance, Risk & Compliance at RBI via Tegus who made the following comments (Bristlemoon readers can enjoy a free trial of the Tegus expert call library via this link):

“[S]pecifically, because PAR is so strong in the restaurant space and so customizable, and they have so many features specifically for the restaurants. That is obviously one of the big reasons why they ended winning the bid because the other ones didn't have as many features as PAR did…It was very customizable and it's really easy to use to make modifications. It's very plug and play, I would say, compared to a lot of the other vendors”.

Business History

PAR Technology Corporation was founded by John W. Sammon Jr. in 1968. For those curious, PAR stands for Pattern Analysis & Recognition. The company’s beginnings were as a small government IT contractor working for the U.S. Department of Defense in Upstate New York. In 1978, PAR developed one of the first POS systems that helped solve problems for the restaurant industry. In 1980, McDonald’s selected PAR as the exclusive POS vendor, and off the back of this strong traction PAR filed for an IPO in 1982.

PAR did well over the next decade but eventually struggled as it was relegated to the increasingly commoditized hardware layer, missing an opportunity to build out a software layer. PAR seemed stuck as a cyclical hardware provider and systems integrator at the mercy of the hardware refresh cycles of restaurants. All the while restaurants were buying their POS software elsewhere. It wasn’t until 2014 that PAR acquired Brink, a small POS software product. PAR took the Brink POS from being installed in 300 stores, to over 9,000 locations five years later, a remarkable feat and no doubt one that leveraged the longstanding relationships PAR had with enterprise restaurant chains.

However, it was in 2018 that PAR found itself in an unbelievable mess. Here are some of the highlights:

The company was under investigation by both the SEC and DOJ over whether certain officers and directors of PAR violated federal securities laws by issuing false and misleading statements regarding sales activities at the company’s China and Singapore offices[7].

The prior CFO of PAR, Michael Bartusek, defrauded PAR out of around $776,000 and invested these ill-gotten funds in a scheme to buy and sell African diamonds[8]. He was sentenced to two years in prison in 2021. (As an incredible aside, Mr. Bartusek, now out of prison, is currently serving as the Group CFO of KPISOFT, a machine learning company. Astonishing).

The company was being run by its Chief of Staff, Karen E. Sammon (daughter of the founder, John W. Sammon), who had been demoted from the CEO position in 2017.

The company had a bad culture with an employee Net Promoter Score (NPS) of -60, and a customer NPS at a similarly poor level.

There were two activist shareholders rattling for change, most notably a sale of the company.

Thankfully PAR is a very different business today (otherwise we would have passed on this investment long ago). Much of that change has come under the stewardship of CEO Savneet Singh. Savneet joined PAR’s Board of Directors in April 2018, and was later appointed as Interim CEO, effective December 4, 2018. The backstory here is that Savneet had tried to convince the PAR Board to sell the company. They refused. The Board then tried to recruit a CEO but no one wanted to take the job. Savneet pulled up his sleeves but initially did not have an intention to stay on as CEO. As he recounted in an interview:

“I was there specifically to sell the company and nothing else. I was not coming in to try and run it. I wasn’t trying to become an expert in restaurant technology. I was just trying to find a way for us to get out of this thing”[9].

The fact that he decided to stay at PAR tells us something about the nature of the opportunity in front of the company. Savneet has an interesting and diverse background:

He is a partner in CoVenture, a multi-asset manager with funds in venture capital, direct lending, and crypto currency.

Previously, he was the co-founder of GBI, an electronic platform that allowed investors to buy, trade, and store physical precious metals.

He was previously an investment analyst at Chilton Investment Company where he covered investments in the technology, alternative energy, and infrastructure space.

Before Chilton, Savneet worked in the investment banking department of Morgan Stanley.

He received a BSc in Applied Economics and Management from Cornell University.

Savneet was on the Forbes 30 under 30 list and Crain’s 40 under 40 list.

His first job was as a scout for the NBA draft.

Savneet certainly had his work cut out for him when taking over the reigns at PAR. In 2019 the PAR CFO came to him and said “we only have 10 weeks of cash flow”[10]. So in short order, Savneet had to lay off 20-25% of the work force within 10 days. They were able to restructure their debt and then get some relief from the SEC and DOJ. He then embarked on a much needed product rebuild (one that cost a lot of money and has been a factor behind the company’s recent FCF losses). As Savneet later recalled:

“We were a software company that had 40 versions, so it’s like we were a cloud but we weren’t really a cloud. Our gross margins on the SaaS were 40% because we had DevOps costs that had gotten out of control because you had 40 versions, that’s hard to deploy…we needed to do a massive rebuild of the product”[11].

Without Savneet Singh, it is doubtful that PAR would have survived. He has transformed the business into a very different company than what existed six years ago. Under Savneet’s leadership, the product was rebuilt and PAR acquired Restaurant Magic (which is now called Data Central), Punchh, MENU, and more recently Stuzo and TASK. The company now has an integrated platform that is resonating with customers and allowing the company to gain market share.

Let’s dig into the financials of the business.