Interactive Brokers (IBKR) - Hoovering up Market Share

A deep dive on the discount brokerage juggernaut

Welcome to Bristlemoon Capital! We have written previously on PAR, AER, PINS, BROS, MTCH, CPRT, RH, EYE, TTD, and META. If you haven’t subscribed, you can join 2,854 others who enjoy our deep dives and investment insights here:

Free subscribers will only receive a partial preview of our reports. The remainder of our reports, which contain the deeper analysis, are reserved for paid subscribers. Consider becoming a paid subscriber for full access to our reports.

Bristlemoon readers can also enjoy a free trial of the Tegus expert call library via this link.

Business overview

Interactive Brokers (IBKR) is a highly automated global electronic brokerage business that offers industry-leading execution at industry-low cost. The company’s flagship trading platform, IBKR Pro, is designed for active, sophisticated traders while the commission-free IBKR Lite is the company’s entry level offering. Traders from over 200 countries use IBKR to trade stocks, options, futures, forex, bonds, mutual funds, ETFs and precious metals across more than 150 exchanges and market centers.

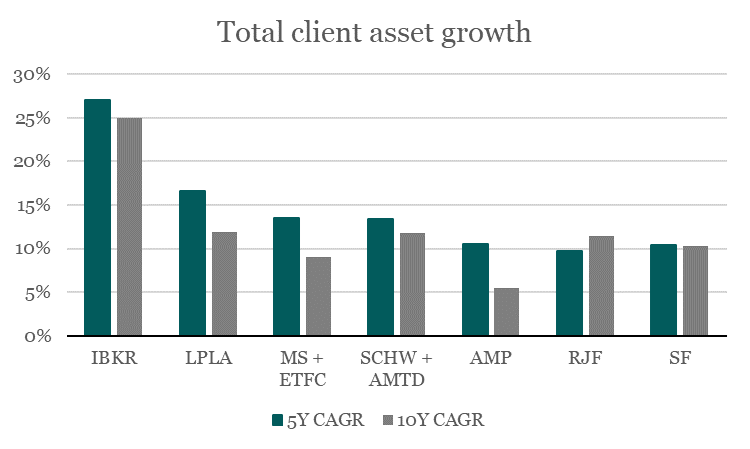

IBKR most recently reported over 2.9 million client accounts in Q2 2024 and nearly $500 billion in client equity. The company has delivered phenomenal client account growth of 35% CAGR over the past five years and has grown client equity at double the pace of traditional discount brokerage and wealth management peers over five- and ten-year horizons. The company generated $4.7 billion in net revenue over the trailing twelve months at a staggering 73% pre-tax margin.

Source: Bristlemoon Capital, company filings

As a discount brokerage business, IBKR generates revenue mainly through commissions on trading activity and net interest income on its income earning assets. Variable costs are limited to execution and clearing expenses and fixed costs are low due to extensive automation, which allows IBKR to earn industry-leading margins.

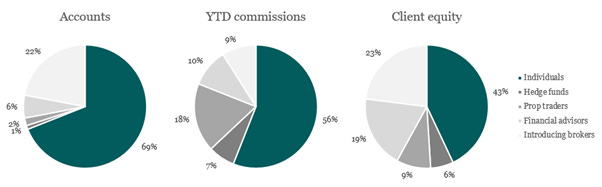

The company offers brokerage services to five client types:

Individuals. These are accounts opened in the name of individuals. They could be traders or investors, professionals or amateurs, ultra-high net worth or funded with bar mitzvah money.

Introducing brokers (IBrokers). These are typically financial institutions such as banks, wealth managers or other brokers who white label IBKR’s trading platform and execution for their own clients. Revenue is shared between IBKR and the IBroker. These relationships can bring tens of thousands of accounts to IBKR.

Registered investment advisors (RIA). IBKR offers a full suite of brokerage services to RIAs and their clients.

Hedge funds. IBKR offers prime brokerage services to hedge fund clients and is a particularly attractive broker for hedge funds with sub-$100 million assets. Hedge funds represent just 1% of client accounts but 6% of client equity and 7% of commissions.

Proprietary trading groups. These professional, high volume trading clients are the bread and butter for IBKR. This is a mature category as IBKR already has high penetration of this client cohort. Prop trading groups are 2% of client accounts but generated 18% of commissions in H1 2024.

Source: Bristlemoon Capital, company filings as at June 2024

Note we use the term “trader” to describe IBKR’s clients because that’s what the company uses; many clients use the platform to buy and hold stocks (i.e., invest rather than just to “trade”).

A brief history lesson

To understand why IBKR operates so differently to discount brokerage peers today, we found the history of the company and its founder to be both fascinating and instructive. The history of IBKR is essentially a history of how the electronic trading of securities came into existence. It is not a stretch to say that without IBKR, the electronic trading landscape today would look vastly different.

IBKR was started by Thomas Peterffy, a figure pivotal to the Interactive Brokers story and the development of the electronic trading of securities. He remains Chairman of the Board and still owns almost 75% of the company, a stake that is worth more than $40 billion.

Peterffy was born in Hungary in the basement of a Budapest hospital during a 1944 Russian bombing raid[1]. He is a descendant of nobles who saw their wealth eviscerated under Hungary’s postwar Communist regime. He had always possessed an entrepreneurial streak: during high school Peterffy would procure smuggled contraband of Juicy Fruit gum, selling these sticks for a 500% markup. At the age of 21, he moved to New York to pursue an engineering career, which fortuitously involved writing software programs on an early computer, the Olivetti No. 1. “I couldn't speak any English, so I figured the computer language might be easier to learn," he later recounted.[2]

Peterffy excelled at computer programming, which saw him eventually transition this skill set to Wall Street, building models for other organizations. By 1977, Peterffy had managed to save $200,000 and bought a seat on the American Stock Exchange (AMEX) to become an individual market maker in equity options[3].

This was a period where trading followed an open-outcry system. Traders would frantically shout or use hand signals to communicate their orders in the trading pit. In fact, during this era, computers were prohibited on the AMEX trading floor[4]! Peterffy observed firsthand the inefficiencies of this archaic system and worked at night to develop his own algorithms (akin to the Black-Scholes model) to calculate the best price to trade each option. He would then print these cheat sheets daily and bring them with him to the trading floor, using them to determine the fair value of these options. Peterffy was the first to use these computer-generated fair value sheets on the trading floor.

In 1982, Peterffy’s trading operation was reorganized into a new firm, Timber Hill Inc., the predecessor of IBKR. Timber Hill came to serve as a vehicle through which equity options trading activities were undertaken as well as a laboratory for implementing Peterffy’s vision for making financial markets more efficient. Not satisfied with using daily cheat sheets, Timber Hill created the first handheld computers for live option pricing in 1983, which gave Peterffy’s traders an advantage over their counterparts[5].

The first Timber Hill handheld computer and predecessor of the iPad, as Peterffy likes to joke. Source: Interactive Brokers

Timber Hill used the profits it earned from its trading operations to invest in new technology that paved the way to revolutionize the securities trading industry. For example, Peterffy built out a communications network with connections to stock and derivatives exchanges around the world. Combining the information from this network with the routing algorithms he devised, Peterffy was able to create a system that could route orders to the exchanges that offered the best prices. This system was upgraded in the 1990s with functionality that could split large orders for the same security into smaller parcels that were then routed to different exchanges depending on prices. This new system facilitated more efficient trade executions and formed the basis of what would become Interactive Brokers[6].

In 1993, Peterffy made the decision to split Timber Hill in two. The electronic market making business would carry on as Timber Hill. A new firm, Interactive Brokers, was formed as discount brokerage operation serving institutions and individual investors. Interactive Brokers was established as a broker-dealer as a way to monetize Timber Hill’s electronic trading intellectual property by democratizing trading for the public[7]. Orders from Interactive Brokers’ clients were sent through the network, executed, and reported to clients in real-time. Clients could also trade a range of securities beyond just stocks and options, including futures, bonds, currencies, and exchange-traded funds. Over time, the number of exchanges that clients could access also burgeoned to the 150+ available today. However, the majority of company profits continued to come from the trading and market making business. But this was about to change.

While Peterffy was well ahead of the curve, a number of high frequency traders emerged in the 2000s that surpassed Timber Hill’s market making business in terms of both speed and efficiency, eroding its profits. In fact, Timber Hill’s market making revenue utterly collapsed from $634 million in 2009 to $40 million in 2017 when the decision was made to cease most of the firm’s market making operations. Nevertheless, the discount brokerage business was scaling rapidly, with net revenues tripling over the same period. Without this pivot to the discount brokerage, Interactive Brokers would not exist today and few of us would ever have heard of Thomas Peterffy.

IBKR’s competitive differentiation

IBKR largely competes along three vectors, which, given the above historical context, can be considered the three foundational pillars of the company.

Price and best execution

Technology and automation

Breadth of product offerings

Price and best execution

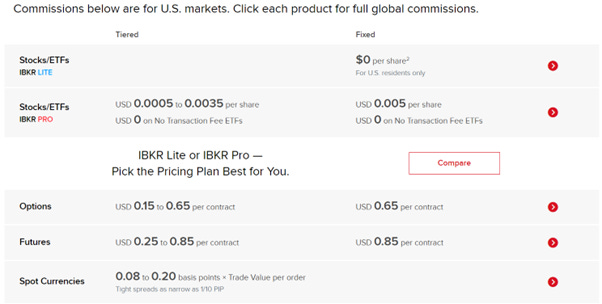

IBKR’s philosophy has always been to offer the lowest cost, which encompasses more than the headline trading commissions. As a platform designed for active, professional traders, execution quality matters more than low commissions and fees. IBKR indicates that on average, total commissions and fees amount to just 1 bps of trade value, with execution costs in the range of 2-5x higher. This means that for a client trading high volume (IBKR average trade size is north of $20,000), a 1 bps slippage in execution – which is just one cent on a $100 stock – will eliminate any commission savings from a zero-commission broker.

Now, obviously, for smaller trades IBKR’s commission will represent a bigger percentage of trade value. The US retail brokerage industry, which has been competing for decades on fees, finally moved to zero commission stock and ETF trading in September 2019. In such an irrational fee environment, one might wonder how IBKR can compete against zero-commission brokers such as Charles Schwab or Robinhood. As these brokers no longer earn commissions on trades, they instead sell the orders to wholesale market makers such as Citadel for opaque execution and earn payment for order flow (PFOF). IBKR launched a US-only IBKR Lite platform for commission-free trading in October 2019, but interestingly four years later Lite comprises less than 5% of total accounts or less than a quarter of US accounts, despite total and US accounts growing over 4x and 2x respectively (our estimate). Evidently, there is a growing subset of retail traders who value transparent best execution over saving several basis points in commissions.

Source: IBKR website

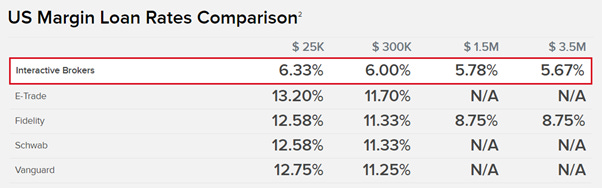

IBKR’s lowest-price philosophy extends beyond net execution costs, as the platform also pays the highest interest on idle cash and charges the lowest interest on margin loans. There is a sliding scale of applicable rates based on account size but suffice to say almost all accounts holding above $10,000 cash (no interest is paid on the first $10,000 cash) would earn significantly higher interest on cash balances at IBKR than at competing brokers. Indeed, the interest on an $11,000 cash balance can be enough to offset IBKR’s commissions on nearly $400,000 of trades. A final benefit is that idle cash is not swept into a subsidiary or partner bank, meaning it is available immediately to trade with.

Source: IBKR website, rates as of September 20, 2024

Source: IBKR website, rates as of September 24, 2024

Technology and automation

IBKR views itself as a technology company that operates a brokerage platform, and at its core the company is focused on developing software that automates its broker-dealer functions. We have read that 60% to 70% of employees are programmers, and most of the senior management team come from programming backgrounds. One Tegus expert explains IBKR’s technology focus as follows:

“The first thing is the infrastructure and our platform. I've never seen a company like that, but 90% of our software is built in-house. So we're not dependent on only any third-party platform. We develop everything ourselves. We can fix everything ourselves. We do not need to wait for processing time or third-party platforms. So that gives Interactive Brokers a high level of flexibility. That translates into the next point. Thanks to that, we could merge various systems together, so they work very smoothly. And while mentioning that, it goes into automation. And this automation, this is kind of deeply embedded in our thinking. […] And then the last two points are because everything is built in-house, it was very easy for us to tweak our system or offer a custom solution for introducing brokers.” Former Head of Brokerage Operations APAC, July 2023

Over the years IBKR has integrated its routing and execution software with over 150 markets and exchanges across 34 countries, allowing clients to trade on these venues without human intermediation. The company built its IB SmartRouting system to support best execution by searching for the best available prices across all available exchanges and dark pools. The company also built its own Alternative Trading System that allows patient traders to cross their orders with other IBKR clients, resulting in even better execution than available on exchange.

Part of what enables IBKR to serve these markets so efficiently is that it has automated back-office functions such as tax and compliance. Connecting to these markets and automating back-office functions sounds straightforward, but this is not the case:

“So we had experienced with some competitors that are really everywhere where we are, but they are not integrated in any sense. So as a result, our technology enabled us to provide that service at much lower rates and much more efficiently, and that nobody seems to want to undertake [the required investment] so far. And I don't know why. Nobody is doing what we're doing.” Thomas Peterffy, 2024 UBS Financial Services Conference

On the client-facing side, IBKR has been developing and improving its desktop Trader Workstation (TWS) for over 20 years and it is regarded as one of the most fully featured platforms available to professional traders. The company has also released streamlined platforms that better suit the needs of less sophisticated traders – including a web platform and two mobile trading platforms and is in the process of building a brand new desktop TWS with a more streamlined functionality set. One common feature across all these platforms is self-service – education and troubleshooting has been automated/codified to be DIY, and a common complaint is that IBKR customer service is terrible and wait times to speak to a human can be impossibly long. Management’s position is that while IBKR is open to onboarding any type of client, it does not actively seek to attract or service basic high-touch retail clients, preferring to leave the handholding to competitors such as Charles Schwab or Robinhood.

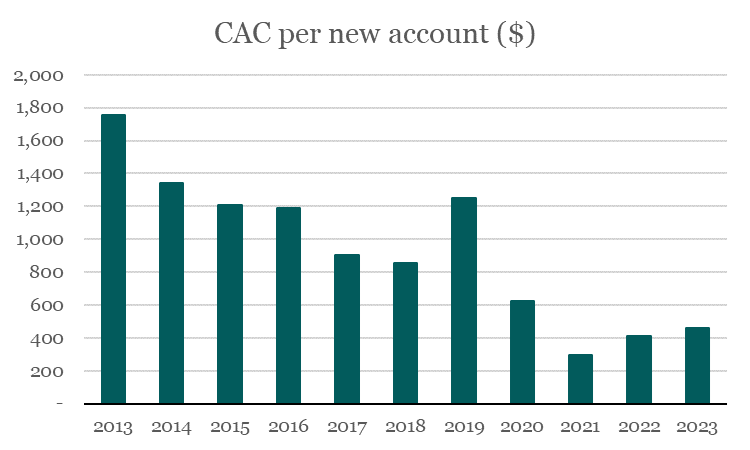

Even the customer acquisition engine – sales and marketing – has been largely automated. The company reported 2,951 employees in Q2 2024, of which only 1% are in sales. These 30-odd salespeople handle institutional prospects such as introducing brokers, hedge funds and investment advisors. Individual clients are mainly acquired through word of mouth and automated advertising channels. This has resulted in customer acquisition cost[8] per new account declining by over 70% over the past 10 years.

Source: Bristlemoon Capital, company filings

“And we finally automated our advertising. So what happens here is that we automatically gauge the yield in each advertising channel every day and we automatically increase or decrease the spending in that specific channel. So it has nothing to do with people anymore. And -- so the only thing that people have left to do is try to identify new additional channels, which we then throw into the mix and we keep measuring it and if it works out fine, then we start to manage it along with all the already-existing channels. And we find that if it's per dollar advertising, we're certainly gradually improving the yield to continue.” Thomas Peterffy, 2023 Barclays Global Financial Services Conference

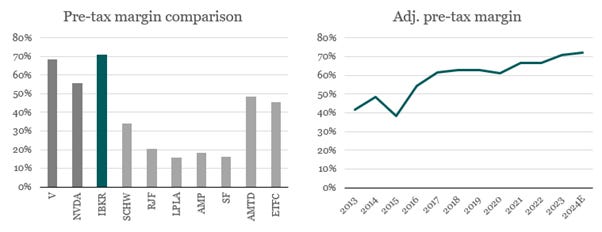

The corollary of this high level of automation across all aspects of the business is that IBKR operates with an extremely low cost structure. The company’s pre-tax margins are phenomenal – right up there with top S&P 500 margin earners such as Visa and Nvidia, and more than twice the margin of peers. While the company has arguably over-earned during the past two years due to the favorable interest rate environment (more on this later), a high 60s pre-tax margin in a more normalized interest rate environment is still indicative of a very high quality business. Quality of earnings is also high as adjustments predominantly relate to FX hedging and mark-to-market on investments.

Source: Bristlemoon Capital, company filings

The low cost structure plus advanced routing capabilities is what allows IBKR to offer among the lowest net execution costs in the industry. This attracts more clients and trading volumes to the platform, which creates further scale efficiencies and operating leverage for IBKR in a virtuous cycle.

Breadth of product offerings globally

Finally, the IBKR platform offers a very broad range of instruments, markets, geographies and currencies to trade. Unlike other discount brokerage peers that tend to be limited by geography or markets, IBKR is available and used by clients in over 200 countries to trade on more than 150 exchanges and market centers in 34 countries and 27 currencies. Clients can trade stocks, options, futures, forex, bonds, mutual funds, ETFs and precious metals all on a single platform.

One particular benefit that IBKR offers its non-US clients (which make up ~80% of total client accounts) is multicurrency accounts which reduce FX risk and minimize forced currency conversion fees, unlike for most peers. This flexibility, combined with low commissions and a wide range of tradable instruments, makes IBKR a compelling choice for international traders looking to access US markets in particular.