AerCap (AER) – An Unconventional Quality Business

Generational supply/demand imbalance creating tailwinds

Welcome to Bristlemoon Capital! If you haven’t subscribed, you can join 2,604 others who enjoy our deep dives and investment insights here:

Before we get onto the stock idea (one that is benefitting from a monumental supply/demand imbalance), we wanted to let readers know that we will be increasing the price for new paid subscribers on 1 August 2024. Importantly, prices for current Bristlemoon paid subscribers will stay the same; it is only new paid subscribers, or those who cancel and resubscribe who will be affected by the price increase. This means that current paid subscribers will continue paying the same price for the life of their subscription, regardless of any future price increases. The new prices are shown below:

We’ve been thrilled by the positive response to the newsletter and want to ensure that the prices we charge reflect the quality of the work we publish. Given the high level of disclosure of Bristlemoon’s intellectual property, we believe that $500 per year is great value. Subscribers who join within the next week will be able to lock in the current lower price of $350 per year ($150 per year, or 30% less, than the new prices that will come into effect) and be unaffected by future price increases.

See below for some of the feedback from our readers:

Below is a list of the stocks we’ve written about:

PAR Technology Corporation (PAR) - The Right Jockey For the Right Horse

Pinterest (PINS) – Not Just Window Shopping

Dutch Bros Inc. (BROS) – A Caffeinated Growth Story

Match Group (MTCH) – To Swipe, or Not to Swipe?

Copart, Inc. (CPRT) – The Auto Undertaker

RH (RH) – A Retail Transformation

National Vision Holdings (EYE) - Bristlemoon Shorts, Edition #1

The Trade Desk (TTD) - A Champion of the Open Web

META and Why Zuck is the King of Counter-Positioning

AerCap Holdings (AER) Thesis

Now let’s give some details about the stock we will be discussing for paid subscribers: AerCap (NYSE: AER). Here are some highlights:

AER trades at an 8.8x forward P/E, and despite an accelerating book value per share growth profile, the company trades at 1x forward P/B.

The aircraft industry is in a deep supply and demand imbalance, with the deficit of airplanes likely to persist for at least the next five years. This could arguably be the best cycle for aircraft lessors that has ever existed.

The AER story features an interesting equity multiple arbitrage opportunity, whereby the company is selling older aircraft at large gains on book value, and using these proceeds to aggressively buy back stock which is trading at a significantly lower book multiple. Last year, the company repurchased ~18% of its market capitalization. We believe this strategy will underpin strong book value per share (BVPS) growth, with BVPS growing at ~27% year-over-year in 1Q24.

Friend of the firm, David Steinthal, the Chief Investment Officer of L1 Capital International, penned an excellent writeup of AER in his June 2024 quarterly letter which alerted us to the opportunity. David is a sharp investor who knows the business inside out and we have but a small fraction of the knowledge on the business that he does. Special thanks go to David for his help in getting us up to speed on AER.

Business Overview

AerCap is the largest aircraft lessor in the world. They own and manage 1,717 aircraft (1,534 of which are owned by AER, the remainder are managed), over 1,000 engines, and more than 300 helicopters[1]. The company has ~300 customers around the world.

Here are some quick details on AER:

AER listed in 2006 on the NYSE. The company is headquartered in Dublin.

The company is the world’s largest owner of commercial aircraft, the world's largest Airbus A320neo Family lessor, and the world's largest 787 owner.

The weighted average utilization rate for AER’s owned aircraft was 98% during FY23. Aside from the pandemic period when the utilization rate dipped to 94% in FY21, AER’s utilization rate has never fallen below 98% in the past 15 years. In 4Q19 it got to as high as 99.8%! This gives us confidence that there is room for AER’s utilization rate to creep higher from current levels.

The average age of AER’s owned fleet is 7.4 years (weighted by book value). This is a relatively young fleet, and the company has recently emerged from a fleet refresh cycle that saw it invest in new technology aircraft. New technology aircraft represent 71% of AER’s aircraft fleet. These are newer, more fuel-efficient aircraft that are the most in-demand aircraft by airline customers, and thus are easier to lease out. This new technology mix will grow, given that new technology aircraft represent more than 90% of AER’s 327 unit order book. The company is anticipating new technology aircraft to comprise ~75% of its fleet by the end of 20241, placing it very well competitively against other lessors who have failed to rejuvenate their asset bases to the same extent.

Source: Company filings

Aircraft lessors have been gaining share of the global aircraft fleet. In 2003, 30% of the global fleet was leased. This has moved up to 50% in 2023, and three-quarters of the incremental aircraft supply over the last five years has been aircraft on operating leases.

Source: Company filings

How does AER make money?

AER owns a fleet of aircraft that it leases out to customers. The company makes money by taking a spread between what they rent their aircraft out for and the cost of funding (i.e., how much interest they’re paying on their debt, as well as the cost of equity).

As the world’s largest aircraft lessor, AER benefits from a scale advantage due to the following reasons:

AER is purchasing aircraft from Airbus and Boeing at a volume that most single airlines are unable to match. This greater purchase volume enables AER to get better pricing from the aircraft OEMs.

These economies of scale extend to managing the specification of the aircraft (these specification costs can run into the tens of millions of dollars for a widebody aircraft). AER’s scale gives the company commercial relevance with suppliers that provide components such as seating, galleys, avionics, and so on.

AER being the largest aircraft lessor with an investment grade credit rating also gives the company a funding advantage.

AER has data scale that can be used to improve its leasing operations. What are the costs of repairing a certain engine? How long are those engines staying on wing before repairs are needed? AER has a lot of datapoints about MRO shop visits that can help it get insights into the true cost of maintaining certain assets (which can be different from the figures claimed by an OEM).

Lastly, we would note that the CEO Aengus Kelly owns around 2.7% of the shares outstanding, making his stake in AerCap worth a little over $500 million. We applaud the fact that Kelly does not pursue growth for the sake of growth. The following quote from the 2024 AerCap Investor Day highlights a disciplined approach to growth that is centered around value creation:

“But you can rest assured as long as I'm in the bus, we are not overpaying for something. We're just not doing it. I mean I don't care if we grow the business or don't. I couldn't care less. I care about are we creating value? Are you making money? I've shrank this company twice. We've grown it very aggressively. I would say I'm the most reluctant buyer of aircraft in the world” - Aengus Kelly (CEO), AER Analyst Day 2024.

Supply/demand imbalance

A generational shortage of aircraft

We love situations where an industry is experiencing a supply and demand imbalance. If you can correctly identify the bottleneck (i.e., who the economics will accrue to) and gain confidence that new supply won’t quickly come online, then these can make for immensely profitable investment setups. In the case of AerCap, there is a generational shortage of aircraft due to the COVID supply chain dislocations and a number of other issues we will discuss. We will briefly comment on the supply and demand situation below:

“Everybody knows that the OEMs are not going to make the number of airplanes they're saying. That's just not going to happen. And every airline worth their salt in the world knows…they've known it for years.” – Aengus Kelly (CEO), 3Q23.

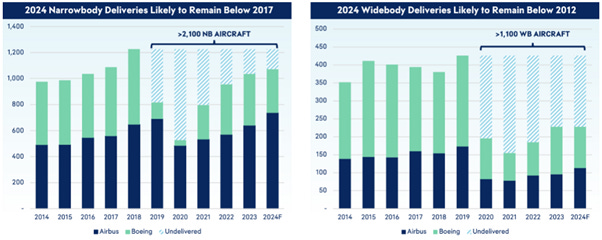

The CEO of AER expects this supply and demand imbalance to last until the end of the decade (i.e., another six years). Here’s the problem: there has been a more than 3,000 aircraft delivery shortfall over the pandemic period relative to pre-COVID delivery levels, yet there is only production capacity at Airbus and Boeing of around 1,250 aircraft. Aircraft production capacity is very much not something that can be quickly ramped up. This means that the aircraft OEMs simply cannot build new aircraft fast enough to plug the COVID delivery shortfall as well as to keep pace with continued demand growth.

As we can see in the chart below, narrowbody deliveries are currently below 2017 levels. For widebody deliveries the supply picture is even worse, with deliveries below 2012 levels.

Source: Company filings

In addition, certain engine OEMs have experienced quality issues that have necessitated recalls. In July 2023, RTX, the owner of the engine-maker Pratt & Whitney, announced a recall of its Geared Turbofan (GTF) series of engine. This was due to a rare powder metal defect that could cause cracking of some engine components. This has led to accelerated inspections of the GTF engine, with 600-700 engines needing to be pulled off Airbus A320neo jets for inspections between 2023 and 2026. The repair work was initially estimated to take 60 days, but this has blown out to an astonishing 300 days per aircraft2. In April 2024, it was reported that one-third of jets with Pratt & Whitney GTF engines were sitting idle as a result of the recall, adding to the current supply shortage problems3.

The supply problems aren’t just confined to OEM production rates; there is also insufficient capacity to repair aircraft. When planes are delivered and flying, they periodically need to be serviced and repaired by maintenance, repair and overhaul (MRO) facilities. MRO capacity was significantly reduced during COVID, and this issue is being exacerbated by issues with certain models of newer aircraft which require service time, as well as the abovementioned engine defects. All of this reduces MRO throughput, leaves planes grounded for longer, and adds to the supply issues.

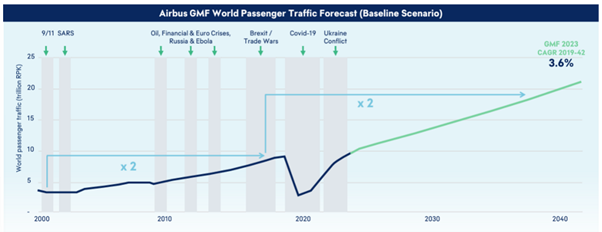

While supply is constrained, demand for aircraft has been solid. Global passenger traffic is now above pre-COVID levels and continues to grow. As a crude rule of thumb, global passenger traffic doubles every 15 to 20 years. IATA is currently forecasting that there will be 56% more people flying in 2024 compared to the number of flyers in 20124. This is great, but there simply is not enough supply to meet this growing demand for travel. We expect global passenger traffic to grow for decades to come: consider that in India today, 15% of all people that get on an aircraft are expected to be first-time flyers, as well as the fact that there are presently no direct flights between China and India, the world’s two most populous countries5.

Source: Company filings

Increasing prevalence of lease extensions

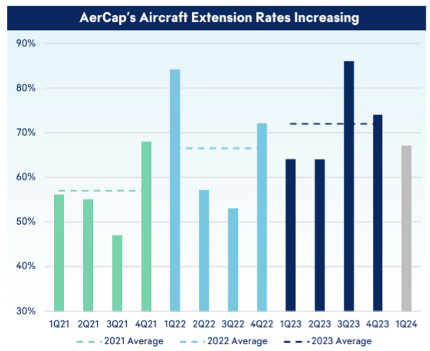

There are ways that we can gauge the tightness of the market. Firstly, the percentage of AER’s aircraft that are seeing lease extensions is increasing. When a lease expires, the airline that was leasing the aircraft from AER can either extend the lease for that same aircraft, or they can look to buy or lease a newer aircraft. Historically lease extensions occurred circa 15% of the time; airline customers much preferred to get a newer plane rather than retain the older plane that’s coming off lease. This has dramatically changed in the last three years as a result of the severe shortage of aircraft. Airlines are struggling to secure supply of these new planes and are forced to extend their existing leases just to maintain their current seat capacity.

As we can see in the chart below, lease extension rates were almost 60% in 2021, and have risen to around 72% in 2023. Those numbers are continuing to march higher as we progress into 2024. Furthermore, for deals signed since 4Q23, AER has placed those aircraft at an average term of seven years, compared to five years in 2019.

Source: Company filings

There were some striking quotes from an aviation leasing panel discussion via Tegus that highlight just how severe the supply shortfall is:

“So we need whatever we need. And today, you can get lease extensions on assets where before COVID, you would have not even considered them for cargo conversion. So quite often, you see assets which are now built in 2000, 2002, 2003, and you can still sign anything between three to six years lease extension on it.”

“So when you look at the current rating, you can hardly see any naked asset being traded. Most of the assets which are traded are assets with lease[s] attached. So the market is really in a high tension, in a high demand and whatever can be done to mitigate this, but when you talk to people in the industry, everybody is saying, hey, can it be fixed in two or three years? No. It will probably take six or seven years or maybe even eight years to get this one back to normal.”

“So for anybody who has assets right now, this is a great time to be in the game because lease rents are at historically high levels. Airlines are talking to leasing companies about slots that are much further out than they normally would.”

Bristlemoon readers can enjoy a free trial of the Tegus expert call library via this link.

Strong gains on aircraft sales

Secondly, we can look at the gain-on-sale that AER is realizing on the aircraft that it sells from its fleet (typically to other aircraft lessors, but increasingly to airlines as a result of the tight market for these assets). An aircraft lease is akin to a bond: there are fixed monthly lease payments and at the end of the lease term you get your asset back (although in the case of an aircraft lease, the asset is the residual value of the aircraft which accounts for depreciation).

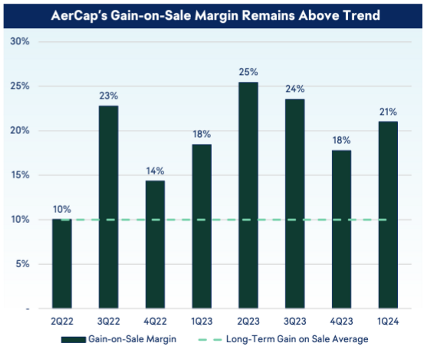

Given this, one would expect a higher interest rate environment to have a deleterious effect on asset values, and manifest in lower gains-on-sale. This, however, has not been happening. We can see below that AER continues to print healthy gain-on-sale margins that are materially above the long-term gain-on-sale average.

Source: Company filings

Going back 60 quarters, AER has disclosed that they consistently sell aircraft at a gain of around 10-11% above book value. This equates to roughly 137% of book equity because those assets are levered. More recently, AER has been selling assets at up to 125% of book value, which is almost 180% of book equity. The reason these gains are sustaining is because lease rates are elevated. Buyers of these aircraft know that they can lease these aircraft at high rates, which overwhelms any headwind from a higher interest rate environment.

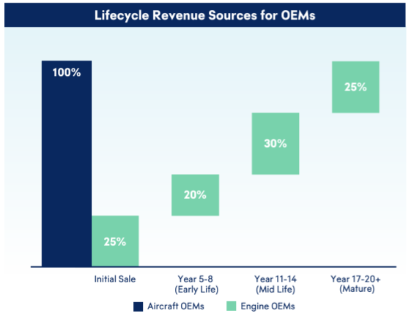

Engine OEMs are an anchor on aircraft production rates

Like any industry subject to cycles, the risk is that a lot of new supply comes online (this would be a headwind to leasing rates and a negative for AER). There is a nuanced reason why the Airbus/Boeing duopoly is unlikely to overproduce aircraft over the medium to long-term. This has to do with the business model of the aircraft engine manufacturers, a critical supplier to the aircraft OEMs.

If we think about Airbus and Boeing, they have every incentive to maximize production and sell as many aircraft as the market will pay for. As we can see in the chart below, the aircraft OEMs receive 100% of their revenue from the initial sale of the aircraft. However, the engine OEMs follow a razor-razorblade model where the bulk of their revenue (and particularly profits) is backloaded, occurring over the multi-decade life of the engine as it is periodically maintained and overhauled. Only 25% of the engine OEMs’ revenue is recognized upfront and the initial sale of the engine typically incurs a loss for the engine OEM. The profits for the engine OEMs are realized over three shop visits where the engine is repaired and rebuilt.

Source: Company filings

Why does this matter? Because engine OEMs have a very strong incentive to make sure older aircraft remain in service so that they can receive MRO revenues and actually derive a profit from that engine sale. If there is an oversupply of new aircraft, then older aircraft are the first to get scrapped. These are the very aircraft that engine OEMs were expecting to earn a profit from. This is extremely bad for engine OEMs and if there’s an oversupply of new aircraft, the most cash flow damaging action they can take is to continue delivering new engines for aircraft.

The backloaded profitability of the engine OEMs’ business model thus acts as an anchor on production rates, and it’s why we haven’t seen a sustained period of aircraft oversupply. This is all to say that we don’t see the supply and demand imbalance being rectified anytime soon.

Lastly, we would note that the desperation of airlines to increase their available seat kilometers is reflected in the increasing use of aircraft, crew, maintenance, and insurance (ACMI) providers. ACMI contracts, also referred to as wet leases are basically short term (1-12 month contracts) whereby the lessor is supplying both the aircraft as well as a crew to operate the plane (this is distinct from dry leases, which is what AerCap provides). The fact that some airlines are turning to wet leases to meet their demand requirements is a signal of market tightness and the difficulty in securing aircraft.

A former Vice President of Leasing at AerCap made the following comments via Tegus: “there is just no availability of aircraft period, whether they're new, brand new or new-ish or even older aircraft. The supply is really the lowest that has ever been.”

Bristlemoon readers can enjoy a free trial of the Tegus expert call library via this link.

Valuation

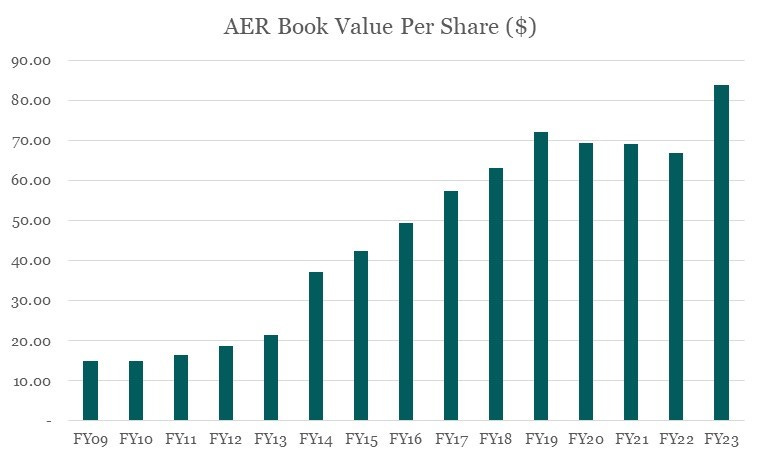

For everything we’ve described thus far, the price for AER appears incredibly undemanding. The stock trades on an FY24 P/E of 8.8x, and roughly 1x P/B. Notably, the stock has seldom traded higher than these levels despite growing its book value per share (BVPS) at a 13% CAGR over the past 14 years. It is worth exploring why that has been the case and whether this could change in the future.

Source: Bloomberg

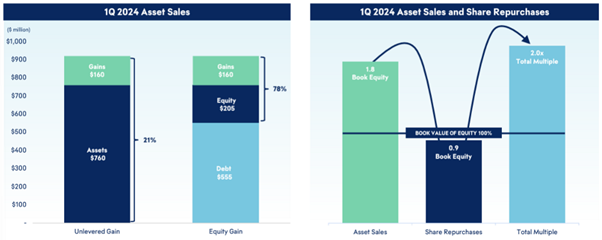

Firstly, we want to highlight an equity multiple arbitrage that is taking place on AER’s balance sheet. If we home in on 1Q24, we can observe AER’s capital recycling strategy in action. In short, the company is selling assets for a premium to book value (with the gains being magnified by leverage) and then using these proceeds to buy back AER stock at a significantly lower multiple.

This is an equity multiple arbitrage that will generate value for AER for as long as the stock’s multiple remains subdued (there is reflexivity to this growth strategy). AER can benefit in two ways: 1) a continuation of this equity multiple arbitrage; or 2) the AER stock multiple significantly increases which would eliminate the arbitrage but also directly benefit AER equityholders.

Source: Company filings

If we dig into the details (which have come from AER’s Analyst Day, which did a fantastic job at framing the opportunity), we can see that AER sold $760 million of book assets for $920 million, earning a $160 million gain on sale which represents a 78% gain on sale over the book equity value of those assets (the rest being funded by debt). So, AER sold aircraft assets in 1Q24 for roughly 1.8x of their book value, but then bought back its stock at 0.9x book value (the multiple has since increased slightly), thus amplifying the positive impact on book value per share. Similarly, the 25% growth in BVPS in 2023 was largely driven by a hefty buyback, in part funded by asset sales through 2023, that reduced the share count by 18%.

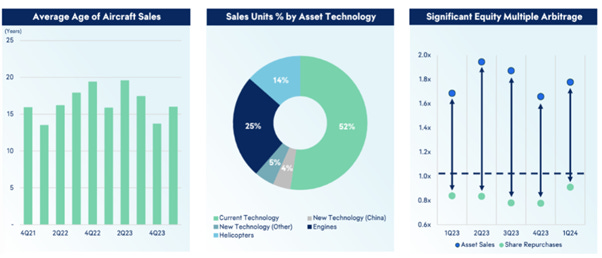

A reasonable question might be which assets did AER sell and why is it selling them? If they are selling their best aircraft to book outsized gains, then the risk is they will be left with a lower quality fleet that disadvantages the business in the future. But as we can see below, the average age of aircraft being sold is north of 15 years most of the last few quarters, with these sales disproportionately being older, current technology aircraft.

Source: Company filings

CEO Aengus Kelly during the 2Q23 earnings call commented on this capital recycling strategy.

“And clearly, today, we firmly believe the cheapest aircraft in the world are the AerCap shares. We are selling assets to professional aircraft traders at significant gains and then buying back the shares in our own business from what the public equity market values our aircraft at a significant discount. As long as that trade continues, we'll keep hitting it”, Aengus Kelly (CEO), 2Q23 Earnings Call.

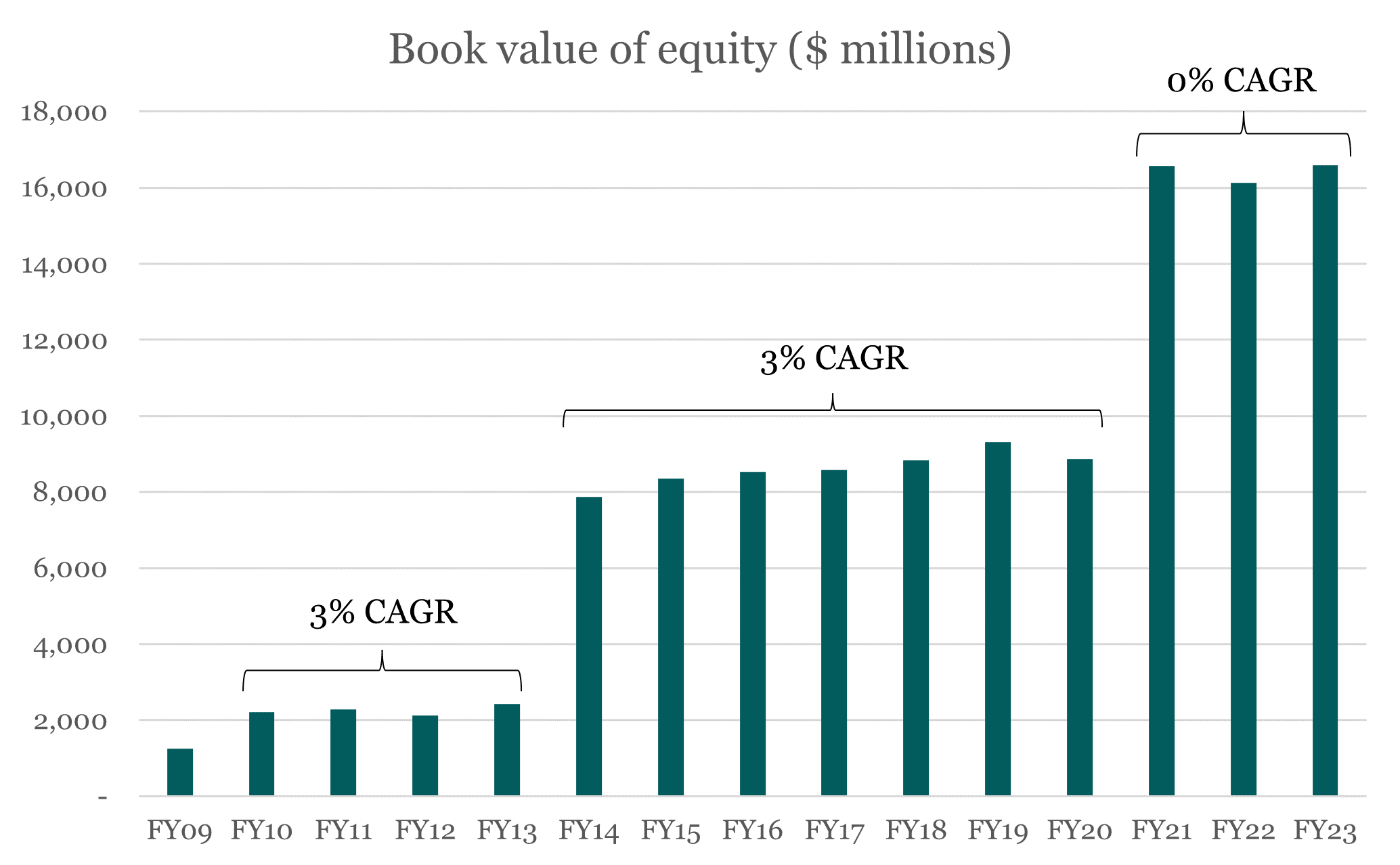

The second component of the BVPS growth is the numerator, book value, where unfortunately our enthusiasm wanes. Unlike BVPS, the book value of equity only grew at a CAGR of 3%/3%/0% over the periods 2010-13, 2014-19, and 2021-23 (there were major acquisitions and COVID that impact comparability across the entire period). This means the BVPS growth has largely come from shrinking the share count – i.e., financial engineering, rather than the compounding of the shareholders’ equity of the business.

Source: Bristlemoon Capital; Company filings

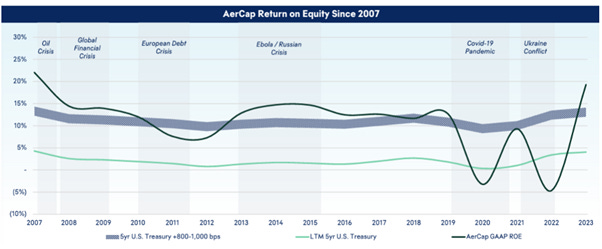

Furthermore, book value is only half the equation – we must also consider the return on equity that AER earns on its book value. The company targets a return on equity that’s 8% to 10% over the risk-free rate. We can observe that even though the broader airline industry has succumbed to nasty cycles, AER’s return on equity has historically been above its target of 800-1,000 basis points above 5 year U.S. Treasuries (the pandemic was an exception, as well as the Ukraine conflict where Russia confiscated a number of AER’s aircraft which caused a $3 billion write-down). In fact, AER has achieved an 11.2% return on equity since 2007, which was on average 910 basis points over Treasuries.

Source: Company filings

A relatively stable 11% average return on equity over 17 years – barring COVID, Ukraine write-downs and subsequent insurance recoveries – is decent but by no means spectacular. This is especially when we consider the leverage employed. Private equity firms produce mean returns in the low-double digits6 while typically employing ~50:50 debt/equity7. AER on the other hand operates at ~2.5x debt/equity and delivers an 11% return on equity (though this has risen to mid-teens on an adjusted basis in the past two years).

Management’s stated cost of equity is 8% to 10% over the 5 year Treasury, but it is up to the investor to determine what is the appropriate cost of equity to apply to AER’s business. Given the high leverage, a cost of equity north of 15% wouldn’t be inappropriate. Factoring in the historical ~3% growth in book value ex-acquisitions, we estimate that AER has not sustainably earned above its growth-adjusted cost of equity. If an asset-intensive business earns a return on equity that is equal to its cost of equity, it should trade at 1x book value. Therefore, it does not surprise us that AER has traded below 1x P/B for much of its history, and we would not expect the stock to trade sustainably above 1x until it consistently generates a higher return on equity.

Source: Bloomberg

Book value is understated

Fortunately, we don’t think you need to rely on multiple expansion to get paid with AER; it is simply a nice kicker if the market becomes willing to pay a higher price for the growth AER is producing. Rather, we think equityholders can do well via the compounding of BVPS. As mentioned, the company has grown its BVPS by a low-teens percentage rate over the last 14 years. More recently, BVPS growth has accelerated to 26.8% year-over-year in 1Q24.

Source: Bristlemoon Capital; Company filings

While the strong BVPS growth that AER has been achieving is good, we would note that the company’s BVPS of $87.5 is also likely to be vastly understated. There are a few key reasons to believe that AER’s true book value is materially higher than the reported book value that the company communicated during its 2024 Analyst Day:

When AER purchased GE’s aircraft leasing business (GECAS) during the depths of the pandemic in 2021 for $30 billion, they acquired these assets for a $3.3 billion discount to their carrying value8 (GE ended up recording a c.$3.3 billion non-cash pre-tax loss in connection with the closing of the transaction). These purchase accounting nuances result in a roughly $16 per share understatement of the book value of the GE assets. Furthermore, we would note that GE followed a more conservative accounting approach, with relatively shorter useful lives (i.e., 15-20 years for GECAS aircraft, compared to AER’s useful lives of 25 years for passenger aircraft and 35 years for freighter aircraft) resulting in quicker depreciation schedules and potentially further understatement of the true asset values.

The fact that AER has historically sold assets at a 10% premium to stated book value supports the idea that the market value of aircraft is well in excess of book value. Furthermore, AER is an owner of hard assets in a world that’s recently come through an inflationary period. It is worth noting that for every 1% of inflation on AER’s $60 billion of assets, this adds around $3 per share of value9 (these aren’t reflected in book value, given the assets are recorded at historical cost).

AER’s book value does not include potential insurance recoveries to AER’s assets that Russia confiscated. The company has recovered $1.3 billion to date, but there is still $2.2 billion remaining of outstanding claims. This amounts to around $11 per share of value.

All of this ties together to suggest that AER’s book value is understated. We estimate that the true book value is likely north of $120 per share.

Why is the stock so cheap?

Beyond what we have discussed about AER’s return on equity relative to its cost of equity, we have several other thoughts as to why AER trades so cheaply:

A number of investors we have spoken to about AER harbor reservations about the airline industry. Airlines through the cycle are marginal businesses and are vulnerable to exogenous shocks that can flow through and impact lease default rates for AER (i.e., wars, pandemics, credit crunches etc.) However, we would note that AER has more recently seen an improvement in the credit strength of its customers, the GECAS transaction further reduced customer concentration, and the company has best-in-class repossession capabilities that have seen it act swiftly and aggressively to repatriate aircraft from lessees experiencing a credit event. Lastly, AER forces high-risk lessees to pay maintenance reserves in excess of the lease payments as another way to manage customer credit risk.

There are risks around future travel demand that could impact airline demand for passenger aircraft, and thus could prove a headwind to lease rates. While we have confidence that aircraft supply will remain tight for quite some time, a diminution of demand for leased aircraft by airlines could help push the market more towards a state of balance and soften lease rates.

The nature of AER’s capital recycling growth algorithm involves earnings that house asset gains. Skeptics would question the earnings quality of AER. We do not think there is anything nefarious about this, but it does create lumpiness to AER’s earnings profile whereby investors are likely reluctant to capitalize these gains on sale. These dynamics also make it difficult for AER management to provide multi-year EPS guidance, creating less visibility into the company’s future earnings profile for investors and the sell-side.

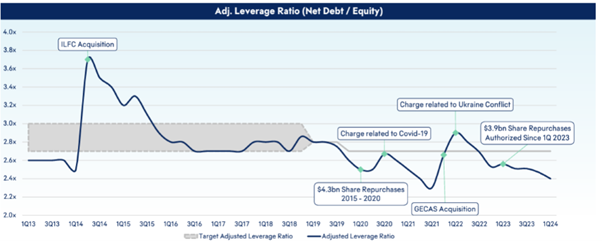

Another common refrain that might stop investors from investigating AER is the amount of leverage used in the business. However, we would note that around 80% of AER’s debt is fixed, and the remaining floating rate debt has been converted to fixed in order to hedge out interest rate risk. While the amount of debt in the business looks high, it is important to note that this debt is held against assets. AER is also operating at a historically low leverage ratio.

Source: Company filings

Our view is that to the extent that this strong cycle allows AER to continue growing its BVPS at 20%+ rates, the stock should deliver an attractive IRR if it maintains its current 1x P/B multiple. Given the unprecedented nature of this cycle, driven by the impact of the pandemic and the OEMs’ ongoing struggles with raising aircraft production rates, it is also possible that AER’s return on equity improves such that its P/B ratio breaks out of its historical trading range. Put simply, if a company can grow its BVPS for above 20% rates for long enough, it is highly unlikely to remain trading at 1x book.

Disclaimer / Disclosures

The information contained in this article is not investment advice and is intended only for wholesale investors. All posts by Bristlemoon Capital are for informational purposes only. This article has been prepared without taking into account your particular circumstances, nor your investment objectives and needs. This article does not constitute personal investment advice and you should not rely on it as such. This document does not contain all of the information that may be required to evaluate an investment in any of the securities featured in the document. We recommend that you obtain independent financial advice before you make investment decisions.

Forward-looking statements are based on current information available to the author, expectations, estimates, projections and assumptions as to future matters. Forward-looking statements are subject to risks, uncertainties and other known and unknown factors and variables, which may affect the accuracy of any forward-looking statement. No guarantee is made in relation to future performance, results or other events.

We make no representation and give no warranties regarding the accuracy, reliability, completeness or suitability of the information contained in this document. To the maximum extent permitted by law, we do not have any liability for any loss or damage suffered or incurred by any person in connection with this document.

Bristlemoon Capital Pty Ltd (ABN: 22 668 652 926) is an Australian Financial Services Licensee (AFSL Number: 552045).

George Hadjia is associated with Bristlemoon Capital Pty Ltd. Bristlemoon Capital may invest in securities featured in this newsletter from time to time.

As of March 31, 2024

https://www.reuters.com/business/aerospace-defense/rtx-expects-3-bln-hit-q3-pratt-whitney-gtf-engine-issues-2023-09-11/

https://www.flightglobal.com/engines/one-third-of-jets-with-pandw-gtf-engines-sitting-idle-as-recall-impact-spreads/157654.article

AER Investor Day 2024.

AER Investor Day 2024.

https://caia.org/blog/2024/04/23/long-term-private-equity-performance-2000-2023

https://www.federalreserve.gov/econres/feds/files/2023009pap.pdf

AER Investor Day 2024.

AER Investor Day 2024.

AerCap presents a particularly compelling story to me now with the recent Airbus recall and seemingly no end in sight for the supply-demand imbalance of commercial aircrafts. Curious to know what metrics you’re now looking mostly closely at and what you believe would give AER the re-rate it deserves?