Adobe Inc (ADBE): slowly, then all at once

Is AI eating Adobe?

Welcome to Bristlemoon Capital! We have written previously on TDG, the AI bubble, FICO, GOOGL, ASML, SNPS, UNH, META, GRND, HEM SS, MELI, U, APP, PDD, IBKR, PAR, AER, PINS, BROS, MTCH, CPRT, RH, EYE, and TTD.

If you haven’t subscribed, you can join 5,600 others who enjoy our deep dives and investment insights here:

Free subscribers will only receive a partial preview of our reports. The remainder of our reports, which contain the deeper analysis, are reserved for paid subscribers. Consider becoming a paid subscriber for full access to our reports.

A reminder that you can register for our upcoming fireside chat with Timee CEO Ryo Ogawa via the following link.

Australian wholesale investors looking to invest in the Bristlemoon Global Fund can do so via this link.

Introduction

Towards the end of last year, we started sifting through what we thought was the rubble of the software sector looking for attractive opportunities. Software sector multiples as measured by the IGV had fallen to the lows of the 2022 bear market on fears that AI would “kill SaaS” for a multitude of reasons: some sensationalist (vibe coding replacements for systems of record) and some real (seat loss, margin compression and/or more competition). Evidently, we were still too early as the rubble has subsequently been nuked into glass.

Source: Bloomberg. Note non-GAAP EPS

One stock that looked derisked enough for us to initiate a starter position is Adobe Inc (ADBE), which had derated to sub-20x forward GAAP P/E compared to a post-SaaS transition history spent almost entirely north of 40x. We laid out some initial high-level thoughts in our December quarterly letter as to why the AI disruption narrative for Adobe might be overstated. However, as we spent the past month or so drafting this article (while watching the market speedrun the diSaaSter —> catSaaStrophe —> SaaSmageddon trade), we’ve refined our framework for software stocks we want to own and formed a much more nuanced view on Adobe, which could reasonably be summarized by Superman:

This is not an article where we pontificate our views on why the SaaSpocalypse narrative is overblown, at least for some SaaS companies. There is already so much public discourse arguing both sides that we don’t have much incremental to add; but more importantly, the market doesn’t give a damn about what you or I think and anyone who resolutely believes they know what the world will look like in two years (let alone the 20+ years of software terminal value) is the real irrational actor.

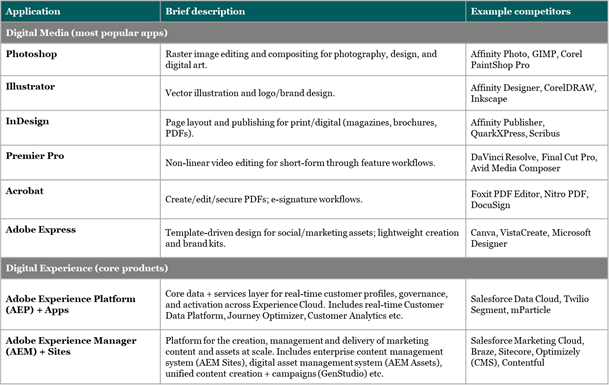

This is also not a deep dive into the history and nitty-gritty details of Adobe’s business segments and products, because that’s not where we think the alpha lies in the present environment. As such, for those who are unfamiliar with the company, we’ve enlisted ChatGPT to provide an overview of Adobe’s product suite and use cases.

Source: Bristlemoon Capital, ChatGPT, Adobe

With this preamble out of the way, we can move onto the real question.

Is Adobe an AI loser?

To us, this question is ultimately about whether the value proposition of Adobe’s creative applications lies in “creation” or “orchestration/workflow”. In a generative AI world, do high-powered professional grade content creation/manipulation tools need to exist? No serious customer is going to vibe code an Adobe product replacement regardless of how frustrated they are with Adobe’s pricing. But might existing and prospective customers decide they need less Adobe in their lives?

To determine whether Adobe stock is a generational buying opportunity or a melting ice cube (or value trap at best), we believe it is critical to answer the following questions:

What does being an AI loser look like for Adobe?

Are Adobe’s products susceptible to being disrupted by AI?

Is Adobe’s business model or economics susceptible to being disrupted by AI?

Can Adobe self-disrupt using AI before an AI competitor or startup disrupts it?

If AI disruption does occur, where will it materialize?

In seeking to answer these questions, we focus mainly on Adobe’s Digital Media segment, which consists of Adobe’s Creative Cloud suite of applications plus Acrobat and is central to the stock’s terminal value. We believe that any decision to own Adobe stock must be underpinned by the view that the Digital Media business is insulated from AI disruption, as the Digital Experience (DX) segment is very unlikely to offset a deterioration of the core creative business.

We flag upfront that the remainder of this article expends no words contemplating the positioning of the DX business. At a high level, we think the DX products are more insulated from AI disruption because of consumption pricing and potentially higher usage if AI agents proliferate the internet. It is, in a sense, a narrow System of Record for the marketing organization of an enterprise. However, this segment is only 25% of total revenue (unchanged since FY19, so it hasn’t increased in importance), and likely a lower share of earnings given its low-70% gross margin compared to 95% for Digital Media. So, if Digital Media is disrupted by AI, DX is not going to save the day.

What does Adobe being an AI loser look like?

As one of the pioneers of the perpetual license to SaaS transition, Adobe’s core business model is underpinned by monthly Price * Quantity. If AI was disrupting Adobe’s digital media business, we would expect to see any of the following:

Seat count reduction

Pricing power erosion

Margin compression

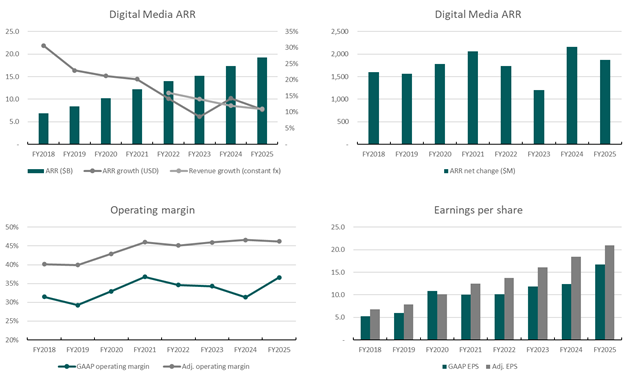

It has been more than three years since the ChatGPT moment, and Adobe’s financial performance is not representative of a company that is an AI loser.

Source: Bristlemoon Capital, company filings

Adobe does not report seats, churn or net retention, but we can infer from the ARR growth above and price increases in recent years that seat count has not declined post-ChatGPT, nor has pricing power been eroded. The net increase in Digital Media ARR looks healthy, and margins have remained stable at a high level. By all indications, this does not look like the financial profile of a business that is being disrupted by AI, and the first-order conclusion is that the current narrative-driven derating has completely dislocated from fundamentals. But, seeing as the market price is the consensus NPV of all future expectations (rational or otherwise), we need to turn our minds from past performance to the future and think about how things are evolving.

Are Adobe’s products susceptible to being disrupted by AI?

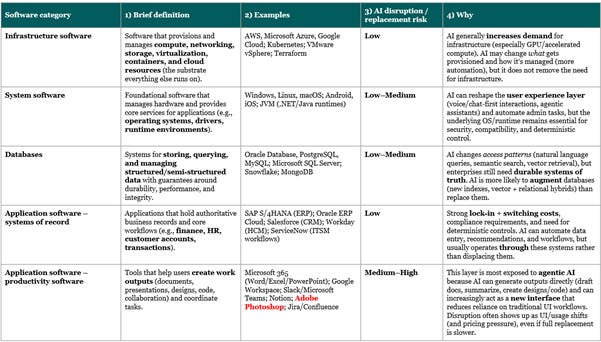

Before answering this question, let’s take a step back and briefly look at the broad categories of software that exist and what characterizes them as more or less susceptible to AI disruption. There is plenty of existing material on the Internet written about this topic and we are not trying to reinvent the wheel here, so we enlist ChatGPT again to provide a high-level overview.

Source: Bristlemoon Capital, ChatGPT

As we can see, Adobe’s core creative software falls within the most vulnerable category of software – productivity-based application software. This explains why Adobe stock has experienced one of the more extreme de-ratings within the software sector and currently trades below 15x forward GAAP P/E and ~1x PEG ratio. It is this objectively, rather than subjectively, cheap multiple that attracted our attention initially.

To answer whether Adobe’s products are susceptible to AI disruption, it is helpful to separate Adobe’s “job to be done” into creation and workflow. Within the creative fields, some software tools are used mainly for the creation of digital assets (e.g. Autodesk Maya, Blender, Adobe Photoshop in some cases) and other tools are used mainly for workflow orchestration or getting a project from ideation through to finished product.

If workflow is the most important job to be done by Adobe software, the company should ultimately prove to be a beneficiary of generative content creation. Generative image and video models that enable much faster and cheaper content creation should drive an explosion of content, some of which will require software like Adobe Photoshop or Premiere Pro to polish into a professional finished product (i.e. TAM expansion).

If creating content is the most important job, the value of Adobe’s software is at risk of erosion because an alternative tool (an image or video model) can do it more efficiently and at lower cost. A high-powered, hard-to-master application like Photoshop gets relegated to the utility workflow layer where minor edits are made to already-generated content. Even if the Adobe workflow remains essential, pricing power may be impaired if users and/or expense approvers perceive greater value in the creation stage.

In simple terms:

Creation is highly susceptible to AI disruption and is already happening

Workflow orchestration is less susceptible to AI disruption and is not happening (yet)

Much of the bear case for Adobe’s creative software rests on people (whether amateur or professional) being able to create images, illustrations, videos etc. using just natural language prompts instead of spending years mastering Adobe’s feature-rich but complex user interface (UI). Thus, even as demand for content creation explodes, Adobe’s seat-based business model may shrink.

We think this perspective largely misunderstands Adobe’s role in the content production process. Even before the proliferation of generative AI, “creation” – as in something from nothing – rarely started within Adobe’s product suite. For example, take Photoshop and image editing. The image most likely originated as pixels on a digital image sensor, which was then uploaded into Photoshop for the editing process. If the intended output is a composite image, Photoshop’s role as the orchestration layer is even more important, allowing the user to combine and manipulate disparate visual elements within one image.

The same can be said about software like Premiere Pro (and competitors such as Avid Media Composer or DaVinci Resolve) for video post-production, i.e. they are used for the editing stage once the raw footage has already been produced. Sure, Nano Banana Pro or Kling 3 might be able to one-shot a simple creative prompt, but natural language edits using these models can be clunky and imprecise (essentially re-prompting the model to generate the output slightly differently). In these cases, having precise human-controlled editing tools may even be more time and cost efficient.

Of course, this will depend on the creative field as well, e.g. illustrators or digital artists who start with a blank canvas and a flexible creative brief will be most disrupted by “good enough” AI image generators. So, we don’t dispute the assertion that some Adobe products will face some disruption, but AI’s raw generation capability is likely overstated as a risk.

Having said all this, the one reason we find it so hard to disprove a steelman AI disruption thesis is that the AI we have today is the worst it is ever going to be. Therefore, dismissing the disruption risk because AI image gen can’t one-shot a complicated scene with perfect fidelity or AI video still occupies the uncanny valley is likely to be shortsighted. Likewise, a strongly held belief that Adobe will retain its central role as workflow orchestrator is a bet that AI development won’t advance to a stage where precise compositions and edits are possible via text prompt or that Adobe tools won’t be relegated to the backend of an agentic natural language UI.

Source: X

Ultimately, all tools are a means to an end. For the commercial creative field, the end is a piece of content that adheres to some specification. Adobe is one of multiple tools used to achieve that end, and AI that can directly (now, or in future) create the output poses a threat to the incumbent tools and workflows used to create that same output. For this reason alone, it would be difficult to size up ADBE as a high conviction investment.

The remainder of this article is reserved for paid subscribers, where we discuss whether Adobe’s business model and economics are susceptible to AI-disruption, what Adobe can do to mitigate any pressure on seats and pricing, and turn our minds to how AI disruption might materialize in Adobe’s business in the future. A big thank you to our paid subscribers!