Is the Airline Industry Really That Bad? – AerCap and A Case of Sandbagged Guidance

An update on the Fund's AerCap investment

Welcome to Bristlemoon Capital! We have written previously on ADBE, TDG, the AI bubble, FICO, GOOGL, ASML, SNPS, UNH, META, GRND, HEM SS, MELI, U, APP, PDD, IBKR, PAR, AER, PINS, BROS, MTCH, CPRT, RH, EYE, and TTD.

If you haven’t subscribed, you can join 5,698 others who enjoy our deep dives and investment insights here:

Australian wholesale investors looking to invest in the Bristlemoon Global Fund can do so via this link.

Introduction

“The airline industry’s demand for capital ever since that first flight has been insatiable. Investors have poured money into a bottomless pit.” – Warren Buffett, 2008 Annual Letter to Berkshire Hathaway Shareholders

Yes, we are indeed starting this missive with a Buffett quote. But while Buffett in his usual folksy manner has consistently deplored the subpar economics of the airline industry, we would posit that the quote above (and the many other Buffett airline quotes) are reductive and fail to account for the distribution of economic fortunes of the various airline industry participants.

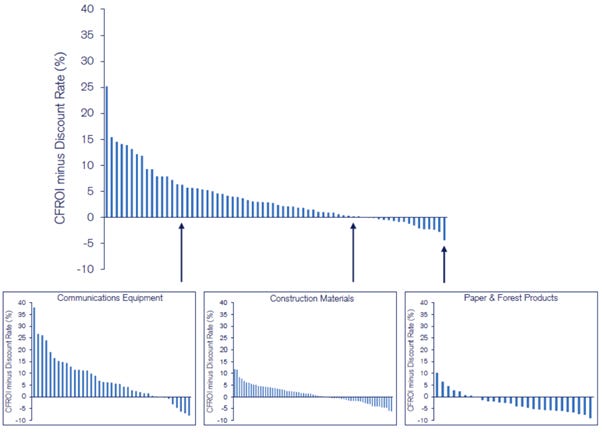

Let’s dig into this idea. As we can see in the chart below, there is a distribution of value creation amongst various industries. But in the smaller sub-charts, we can also observe that within any given industry there is a distribution of value creation. In other words, the average level of value creation (or destruction) for an industry masks the fact that beneath the surface there will be some companies creating value, and others destroying value.

Source: Credit Suisse

(N.B. the blue bars measure the spread between the cash flow return on investment (CFROI) and the cost of capital across 68 global industries, classified under MSCI’s GICS framework, using 5,500 publicly listed companies)

Admittedly, when we first started looking at AerCap (AER) in mid-2024, our thinking was prejudiced by the bad reputation of the airline industry as a cash incinerator. You see, AER is the world’s largest aircraft lessor, and we initially struggled to fathom how this would be a business worth investing in for Bristlemoon. As we did more work on AER, this uneducated view very much changed.

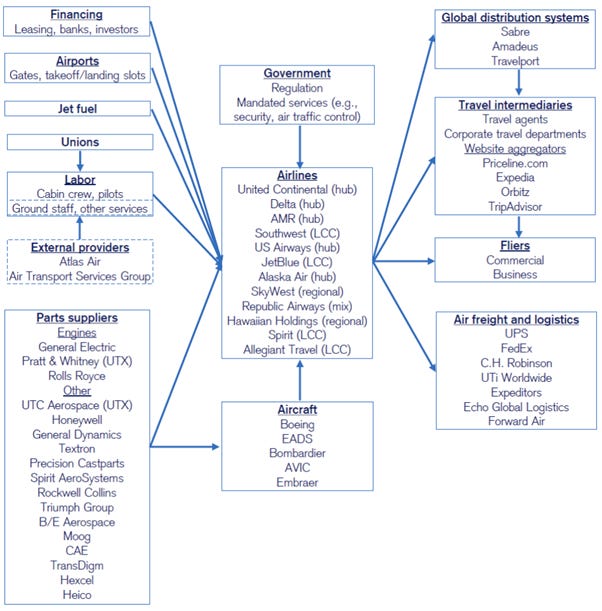

As we can see from the industry map below, the airline industry is obviously a lot broader than just airlines.

Source: Credit Suisse

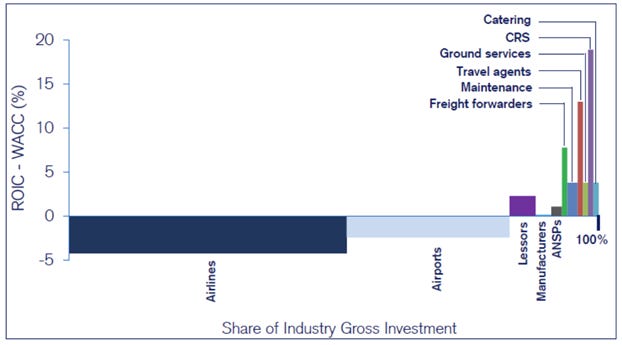

So how does an aircraft lessor stack up? Based on Michael Mauboussin’s profit pool chart below, we can observe that lessors have generated a healthy amount of economic value (measured as a function of the economic profitability of the industry – that is, the CFROI less the discount rate – and the aggregate invested capital).

Source: International Air Transport Association, “Vision 2050”, February 12, 2011; via Credit Suisse.

(N.B. Returns data is from 2002-2009, and investment data is as of 2009. CRS = computer reservations systems; ANSP = air navigation service provider)

A recap on AerCap

While this is a high level, rather academic approach to industry analysis, it’s worth reiterating what attracted us to invest in AerCap back in 2024. We would point readers to our original write up on AER back in July 2024 which can be found here. We have removed the paywall to that article so all readers can view the writeup in full (notably the majority of points in the article continue to provide tailwinds for AER today).

The stock is up more than 60% since July 2024, having compounded at 33% per annum. However, despite this stock price increase, there are still reasons why we continue to own the stock in the Bristlemoon Global Fund.

Source: Bristlemoon Capital; Bloomberg

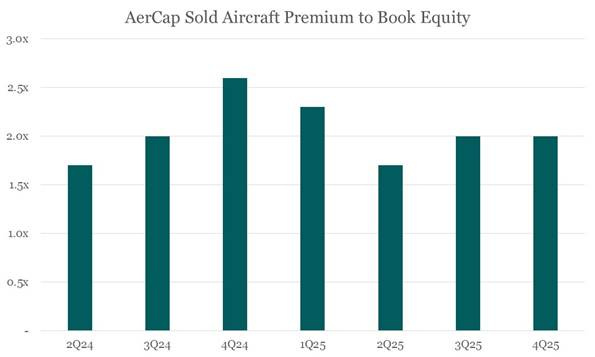

As a recap, AER is a multiple arbitrage story. The company is selling planes from their fleet at 2x book value, and buying back stock at around 1x book. This is, of course, financial engineering. But it is also wonderful value generation mechanism given the very high degree of confidence we were able to build around the aircraft undersupply situation persisting.

Source: Bristlemoon Capital; Company filings

AER CEO Aengus Kelly has done a spectacular job of creating value for AER shareholders (it’s no wonder – his interests are quite aligned given that he owns more than $770 million of AER stock). For example, AER repurchased 22.1 million shares in 2025, shrinking its diluted shares outstanding by around 11% year-over-year. In fact, the number of shares outstanding for AER is now 31% lower than it was just three years ago.

In this sense, owners of AER over that period now have a 45% greater claim on the business due to these buybacks. This is remarkable, and there are very few examples in public markets where companies retire almost one-third of their share count in such a condensed period.

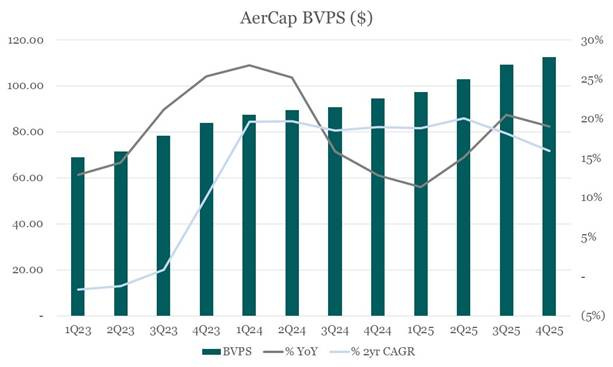

These buybacks have led to the company’s book value per share (BVPS) compounding at a healthy clip (and note that this BVPS is understated for a variety of reasons we state in our original writeup).

Source: Bristlemoon Capital; Company filings

Sandbagged Guidance

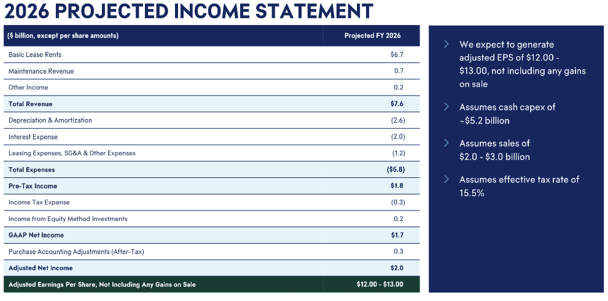

Earlier this month the company reported its Q4 2025 earnings result and gave guidance for FY26 EPS of $12 to $13. With the stock trading around the $150 mark, that guidance sounds wholly underwhelming when we consider that AER has historically traded at an 8x P/E (implying a share price range of $144 to $152 per share). This misses a few things, and we will mount a case why we believe that the guidance given is highly conservative.

Firstly, we would note that the $12 to $13 EPS range does not include any further gains on sale from selling aircraft. Thought of another way, the guidance assumes that AER simply stops selling planes for high prices and realizing material gains on sale that benefit its EPS. We would round the probability of this occurring down to zero, particularly given the company is already assuming $2.0 to $3.0 billion in aircraft sales in FY26 (the company disclosed this when it disaggregated the various P&L projections that support the company’s FY26 EPS guidance).

It is worth noting that in FY25 AerCap sold $3.9 billion worth of aircraft and generated $3.95 per share from gains on sale of these owned aircraft (i.e., almost 26% of FY25 adjusted EPS of $15.37 came from gains on sale). While these gains from asset sales are difficult to underwrite and will be lumpy by quarter, perhaps we can bake in an additional $3-4 of EPS from gains on sale in FY26. This bumps up the FY26 EPS range to $15-$17.

It is also worth noting that even outside of any gains on sale, AER has a tendency to be conservative when guiding the base business EPS. For example, in Q4 2024, the company guided FY25 EPS to a range of $8.50 to $9.50. As we progressed through 2025, the company continued to upgrade this EPS guidance. Excluding gains on sale, AER achieved $11.42 of base business EPS in FY25, a whole 20% to 34% higher than the initial FY25 guidance range given in Q4 2024.

Our expectation is for this FY26 EPS guidance to be upgraded as we move through the year, and this is based not so much on precedent but on some of the conservative assumptions underpinning the guide relative to what we think the future holds for AER.

Below we can see the various assumptions the company is using to arrive at its $12 to $13 of FY26 EPS.

Source: Company presentation

What immediately jumped out at us was the projection for $6.7 billion of basic lease rents in FY26. This is mostly because AER generated $6.7 billion of basic lease rents in FY25. So, in other words, in one of the tightest aircraft markets we’ve seen in decades, the company is assuming that basic lease rents will be flat in FY26.

For example, AER’s owned aircraft average utilization rate has been 99% for the last two consecutive years. In FY25, AER extended 87% of leased aircraft, up from 79% in FY24, highlighting very strong customer demand for leased assets. This is all putting upward pressure on lease rates which should be supportive of basic lease rent growth.

However, it should also be noted that the company is selling planes from its fleet, which naturally has a deleterious effect on lease revenues. Nevertheless, basic lease rents increased by 5% and 2% year-over-year in FY25 and FY24, respectively. These were years when there were a heavy number of asset sales. We would also point out that AER continues to replenish its fleet via aircraft purchases, which helps offset the impact on basic lease rents from aircraft sales.

As a final point, 12% of AER’s current fleet is comprised of COVID-era leases, which will roll off linearly out to 2031-2032 (i.e., around 2% of AER’s fleet will reprice each year out to the early 2030s). This is an important point due to the magnitude of repricing. During AER’s May 2024 Investor Day, management disclosed that AerCap extended an aircraft for an existing operator in 2020. It was a three year extension struck at a sub-$120,000 rate. The aircraft came up for re-lease and was extended again at a lease rate above $165,000. In other words, AER was able to achieve a 40% increase in lease rates even though the aircraft was three years older.

We suspect that given lease rates have continued to increase since then that AER could achieve a very healthy pricing uplift on the 12% of its lease book that will roll off in the coming years. For example, if 2% of the lease book were to reprice with a 50% lease rate uplift, then this should boost basic lease rents growth by 1 percentage point.

It’s possible that another $2 of EPS could emanate from management upgrading its base business guidance. Tying all of this together, we believe a more reasonable EPS range for FY26 is $18-19 per share. The next part in framing the return shareholders are playing for is to determine what multiple AER might trade at in the future.

What multiple is fair?

Historically, AER has roughly traded at between 0.6x to 1.2x of its book value.

Source: Bloomberg

The stock has also traded at a c.7.5x P/E on average over the last decade, struggling to sustain above 10x.

Source: Bloomberg

The fact that AER’s multiple is at the top of its historical trading band, sitting at around 9.5x is not a great starting point. And there’s clearly downside to the extent to which the multiple de-rates back to its historical levels (this is a key reason why the Fund’s position in AER is sized much smaller today).

It is, however, also worth turning our minds to future opportunities that could cause the multiple to rerate. AER management was asked the following question on the Q4 2025 earnings call:

“In the industry, another owner of engine assets announced they’d be looking to convert engines to power turbines to service data centers. Is that something you guys are exploring?”

CEO Aengus Kelly’s answer highlighted AER’s willingness to participate in converting aeroderivative opportunity – that is, converting aerospace engines such as the CFM56 to turbines that power data centers:

“And of course, we’re looking at this. And if it turns out that the demand for what are currently commercial aerospace engines, if that demand to convert them into ground-based power generation for data centers is very durable and is long lived, then of course, we will participate in that, either directly or indirectly, directly by converting the engine into ground-based power generation or indirectly by taking advantage of this surge in demand. But at the moment, we want to make sure that this demand is a durable demand and it’s not fleeting, and that’s our focus at the moment is sizing the market. And from there, then we will participate, as I said, one way or the other.

In terms of the quantum of engines that we have ourselves, if you look at what’s installed on our aircraft, take the CFM56 model, we are the largest owner of CFM56s in the world. And I would remind you that all of our engines are serviceable and have to be returned for the most part in full life conditions, which is very different to a portfolio of engines that is half life or run out engines, and you’re swapping modules to make a serviceable engine. So, when we look at the engine portfolio that we have…on any of those metrics, we would have more engines than anyone in the world.”

The recent pop in the share price of FTAI Aviation (+55% YTD) highlights the immense uplift in value the market is currently willing to ascribe to companies hitching their cart to the AI data center buildout. FTAI recently announced FTAI Power, an initiative to convert CFM56 engines into 25-megawatt turbine units that can generate electricity to power data centers. The stock went vertical.

Source: Bristlemoon Capital; Bloomberg

Our belief is that energy is one of the key bottlenecks in the AI infrastructure buildout. Existing grid capacity is insufficient to power these energy-hungry data centers, which is why we’re already seeing an increasing prevalence of behind-the-meter (BTM) power solutions (i.e., energy systems installed on the customer’s side of the electricity meter rather than on the utility/grid side). The demand for energy is likely to be so great that these BTM energy systems such as aeroderivative turbines could become permanent fixtures to providing power, as opposed to a stop-gap solution that will temporarily bridge these energy needs while the grid plays catch up.

Given the multi-year tailwinds around data center energy demand that we think there is decent visibility over, combined with Aengus Kelly’s openness to participating in the aeroderivative opportunity, there is a scenario where AER significantly re-rates above its past historical multiple range if the company did start selling CFM56 engines to FTAI or if it embarked on converting the engines itself. We believe the former is much more likely, given that FTAI Power required a year of investment to operationalize and it was built on FTAI’s Maintenance, Repair & Exchange (MRE) platform (which is not something AER has).

If the market were to catch wind that AER is now selling engines to FTAI which are then being converted for data center power generation use cases, then this could lead to a re-rating. However, this is a rather speculative prospect to be banking on for further multiple expansion (again, which is why the Fund’s AER position is currently small) and we suspect that Aengus Kelly would prefer that there was not a significant re-rating in AER’s multiple. Rather, we’re almost certain he’d prefer to surreptitiously profit from the aeroderivative opportunity and then use those profits to repurchase large amounts of AER stock at a depressed multiple – the same playbook he’s been using for years.

This isn’t a terrible setup. Management has indicated that the aircraft shortage should persist into the 2030s, meaning that they should be able to continue selling aircraft assets at a healthy premium to book and buying back stock at a lower multiple. But if investors were to suddenly become giddy about AER being an indirect beneficiary of the data center buildout and subsequently bid up the stock, then AER stockholders obviously do well in that scenario too.

AER is one of those rare opportunities where you have very good visibility over the value drivers, but with the stock having re-rated somewhat and many other stocks in this market having significantly de-rated, we are currently holding AER as a smaller sized position in the Bristlemoon Global Fund.

Disclaimer / Disclosures

The information contained in this article is not investment advice and is intended only for wholesale investors. All posts by Bristlemoon Capital are for informational purposes only. This article has been prepared without taking into account your particular circumstances, nor your investment objectives and needs. This article does not constitute personal investment advice and you should not rely on it as such. This document does not contain all of the information that may be required to evaluate an investment in any of the securities featured in the document. We recommend that you obtain independent financial advice before you make investment decisions.

Forward-looking statements are based on current information available to the author, expectations, estimates, projections and assumptions as to future matters. Forward-looking statements are subject to risks, uncertainties and other known and unknown factors and variables, which may affect the accuracy of any forward-looking statement. No guarantee is made in relation to future performance, results or other events.

We make no representation and give no warranties regarding the accuracy, reliability, completeness or suitability of the information contained in this document. To the maximum extent permitted by law, we do not have any liability for any loss or damage suffered or incurred by any person in connection with this document.

Bristlemoon Capital Pty Ltd (ABN: 22 668 652 926) is an Australian Financial Services Licensee (AFSL Number: 552045).

George Hadjia and Daniel Wu are associated with Bristlemoon Capital Pty Ltd. Bristlemoon Capital may invest in securities featured in this newsletter from time to time.

Measuring moat is such a great piece