Grindr (GRND) - The Gay Dating App Monopolist

Is this the most dominant dating app in existence?

Welcome to Bristlemoon Capital! We have written previously on HEM SS, MELI, U, APP, PDD, IBKR, PAR, AER, PINS, BROS, MTCH, CPRT, RH, EYE, TTD, and META. If you haven’t subscribed, you can join 4,344 others who enjoy our deep dives and investment insights here:

Free subscribers will only receive a partial preview of our reports. The remainder of our reports, which contain the deeper analysis, are reserved for paid subscribers. Consider becoming a paid subscriber for full access to our reports.

Bristlemoon readers can also enjoy a free trial of the Tegus expert call library via this link.

George Hadjia from the Bristlemoon team will be attending the Berkshire Hathaway AGM in Omaha this year and would love to catch up with other investors and allocators. Please reply to this email or reach out to info@bristlemoon.com if you are in Omaha and want to catch up!

Introduction

Did you know that up until the 1950s, all U.S. states had laws that criminalized homosexual acts? These laws typically targeted sodomy, construed as “crimes against nature, committed with mankind or with beast”[1] In fact, the American Psychiatric Association (APA) classified homosexuality as a mental disorder until 1973[2]. However, the last few decades have seen an increasing acceptance of homosexuality in the U.S. and abroad.

While these trends can become politically charged, one thing is clear: a dating app such as Grindr (NYSE: GRND) that caters to gay and bisexual men is benefiting from these demographic shifts, with revenues and earnings having grown at 26% and 24% CAGRs, respectively, over the last five years. Layer on the fact that Grindr has a virtual monopoly over the gay dating app market, has higher engagement levels than any dating app in existence, and is still early in its monetization journey, and there was enough to get us interested to do more work on the company. Consider the fact that just 7.6% of Grinder’s MAUs are paying users, compared to low-20s% for Tinder.

We have previously opined on the dating app space via our deep dive on Match Group, a Business Breakdowns podcast, as well as a recent podcast with Eric Seufert on the dating app space. Our enthusiasm towards hetero dating apps such as Tinder has significantly cooled, and we believe that they have been over-monetized in a way that disrupts and degrades the network dynamics between male and female users. Grindr, being an app primarily for gay men, does not suffer the same network imbalance between male and female users, which we will explore in this report.

While no one on the Bristlemoon team is in the gay community, we took the liberty of downloading the Grindr app to get a feel for the product, and to help readers understand the nuances of Grindr.

We will step readers through the product design, and how it differs from the hetero dating apps such as Tinder and Bumble, and then explore the implications of Grindr’s product quirks as they relate to the monetization potential of the user base.

Key Takeaways

GRND has a monopoly on the gay dating app market; it has the #1 position in virtually all markets in which it operates. 90% of the users on the app are looking for casual sex interactions, and the company’s product design emphasizes speed and proximity to enable this. GRND’s user engagement is off the charts, with users on average spending 70 minutes per day on the app.

Grindr’s business model is a freemium subscription model augmented by advertising. The app is free to use, but users can pay for premium subscriptions to unlock access to additional features, and remove annoyances such as ads, which are excessive in the app.

Grindr is a network business that is now at a scale that would be incredibly difficult to replicate or disrupt. The company has 90% unaided brand awareness in the U.S. and spends de minimis on advertising while still enjoying high-single digit year-over-year MAU growth. User growth, at this stage, has become self-reinforcing for GRND. The relatively stronger desire for proximity on Grindr means that its “atomic network” – that is, the minimum size of the network required for the platform to deliver value and become self-reinforcing – is arguably higher for Grindr compared to the hetero apps. This makes it even harder for competitors to chip away at Grindr’s moat.

We have reservations about the quality of GRND’s management team, particularly CEO George Arison, and the ability of management to execute on their strategic vision for the business. The feedback we heard about Arison from former employees and on Glassdoor was overwhelmingly negative.

From GRND’s 2024 Investor Day disclosures, we are able to estimate the company’s ARPPU for the U.S. and International segments. We calculate that GRND’s International users are only monetizing at 58% of the rate of its U.S. users. To the extent that the company is adding more of these relatively lower-monetizing International users, it is dilutive to overall ARPPU growth. This is important when we consider that 63% of GRND’s overall payer additions came from International between 1Q21 and 1Q24, and we anticipate an even higher amount of future net payer additions to come from International.

We are less bullish than other investors about GRND’s ability to substantially lift its payer penetration rate. For dating apps, monetization is most effective when one side of the network will pay to reach the scarcer, more selective side (i.e., women in the case of an app like Tinder). On Grindr, however, attention isn’t scarce – many users report that they can find a date or hookup fairly easily without paying, provided they are in a populated area. This creates an interesting paradox on Grindr: because the app has a high supply of willing partners, which makes the app very effective for free users, this effectiveness reduces the incentive for users to pay for premium features.

We look at what assumptions are required to produce a mid-teens percentage IRR at year 5, modelling out the various line items to get a more granular understanding around what needs to happen for investors to get paid. Our conclusion is that the market is baking in a significant ramp up in the payer penetration rate, a development that we at Bristlemoon would not be comfortable underwriting for reasons we discuss in the report.

Table of Contents

Business Overview

Incredible engagement metrics

Demographics

User experience walk-through

No matching needed

Right Not

Roam

How Does Grindr Make Money?

Direct Revenue

Indirect Revenue

Business Quality

Reservations about GRND management team

Competition

Business History

Grindr’s Growth Algorithm

MAUs

Payer penetration and revenue per payer

Tinder pulled the monetization lever too hard

Proceeding cautiously with monetization

GRND’s U.S. and RoW payer penetration rates

Grindr avoids gender imbalance dynamics of hetero apps

Immediacy supports monetization

User spending dependent on user attractiveness

Ads Opportunity for Grindr

Financials

Valuation

Conclusion

Business Overview

Grindr Inc. (GRND) owns the Grindr app, which is the leading dating app for primarily gay and bisexual men. The app has around 14.7 million monthly active users (MAUs), with a user base that spans over 190 countries. Grindr, which launched in 2009, was one of the first geolocation-based dating apps, pioneering a new model of online connection for gay men. The app has an unshakable reputation as a hookup app – a place to find quick, often same-day meetups; much of the activity on Grindr is facilitating casual sex interactions, with the company itself acknowledging that 90% of users on the app are looking for something casual.

Grindr emphasizes speed and proximity – who is near me right now and wants to meet? Think of Grindr as the Uber for gay dating – you open up the app when you’re looking to find a date or hookup on-demand. Hetero apps, even the more hookup-oriented Tinder, still have an element of browsing for later; Grindr is often for here-and-now. Grindr in this sense is monetizing different user intent than the hetero apps. To put it crassly, Grindr is primarily monetizing the sex drive of males who are trying to satisfy an urge.

“The reality is to say it outright, I mean, Grindr just delivers on getting you laid very, very fast in the major cities in the U.S. You touch a button and it’s pretty much as easy as ordering a pizza. You can have an encounter in person of sexualized nature.” – Founder and CEO of Hornet [competitor to Grindr], via Tegus

For readers who might have interfaced with heterosexual apps such as Tinder or Bumble, we would note that the interface and user experience on Grindr is entirely different. For example, Tinder and Bumble use a swipe-based, double opt in matching mechanism. On these apps, you will swipe through profiles until you match with a profile that has also swiped right on your profile. Grindr’s interface, on the other hand, is a location-based grid of profiles, showing who’s nearby and available. We dive into this user experience and what it means for GRND’s monetization potential later in the report.

Grindr’s product design encourages immediacy. Profiles are short (a few pictures and a brief description), the distance to each user is shown, and you can initiate a chat with anyone without needing to “match” first. In essence, it’s a bit like walking into a bar where you can say “hi” to anyone. By contrast, hetero dating apps usually require a mutual match (both swipe right) before conversation, akin to a friend introducing you only if there’s mutual interest. Grindr removes that gate, which can lead to more conversations and yes, more explicit propositions, very quickly. Users can exchange nude photos on the app and in our testing of the app we had multiple Grindr users who reached out with an initial message of a revealing photo.

Incredible engagement metrics

This freedom and immediacy drive extremely high user engagement metrics. In 2024, Grindr users on average spent over 70 minutes per day on the app– an eye-popping figure that outstrips most dating apps. They also sent over 130 billion chat messages in 2024, indicating the rapid-fire conversational nature of the platform.

“People spend over an hour on the app a day, and those numbers are not going down. They're going up, right? So we're doing very well in both of those metrics now. So we are not seeing any sort of drop off in engagement, whether it's overall or within the Gen Z segment, which is where people kind of focus on a lot.” – George Arison (CEO), Goldman Sachs Communicopia Conference 2024

While the time spent numbers from Sensor Tower are somewhat lower than what management claims, there is still very strong user engagement with the app, and much more time is spent on Grindr than competitor gay dating apps such as SCRUFF and GROWLR.

Source: Sensor Tower

We can also observe that Grindr engagement is far above that of the hetero apps such as Tinder, Hinge and Bumble.

Source: Sensor Tower

In fact, the amount of time users spend on Grindr is nudging up against some of the best-in-class social apps such as Instagram and TikTok.

Source: Sensor Tower

Grindr users often keep the app open and running as they chat, share photos (over 2 billion photos in 2024, many likely NSFW), and coordinate meetups. This incredible engagement is a double-edged sword for Grindr: on one hand it means abundant opportunities to show ads or upsell features, but on the other hand it reflects that the app has essentially become a utility in users’ lives, and any disruption or frustration due to over-monetization could cause strong backlash given how ingrained it is.

Demographics

It might be surprising to some that 9.3% of U.S. adults identify as lesbian, gay, bisexual, transgender (LGBT), or something other than heterosexual in 2024 (based on a Gallup poll). This is also up significantly from 3.5% in 2012 when Gallup first measured it. Regardless of your political views, the data shows that more and more Americans are identifying as gay.

Source: Gallup

Much of this is driven by much higher rates of LGBTQ+ identification amongst younger generations of Americans. More than one in five Gen Z adults – that is, those born between 1997 and 2006, who were aged between 18 and 27 in 2024 – identify as LGBTQ+[3]. This is significantly higher than just 1.8% of those from the silent generation (i.e., born in 1945 or earlier) identifying as LGBTQ+. But even within the Gen Z demographic, LGBTQ+ identification rates have increased from an average of 18.8% in 2020 through 2022, to 22.7% over the past two years[4].

Source: Gallup

GRND management has noted that gay men on average have significantly higher disposable income than their straight counterparts. During their Investor Day they noted that gay households have 2x the income of a straight household ($128k for same sex male couples compared to $75k for the total population in the U.S.[5]), and that 52% of gay men in the U.S. have a Bachelor’s degree (compared to 36% of all U.S. adults)[6]. The majority of gay couples not having children helps increase their disposable income relative to straight couples. However, we also came across studies calling out the myth of gay affluence with conflicting data. For example, a somewhat dated study by UCLA’s Williams Institute from 2014 found that 29% of LGBT individuals experienced food insecurity, and one in five gays and lesbians aged 18-44 received food stamps in the last year.

The problem with the user demographics statistics quoted by management is that many Grindr users are closeted – that is, they do not openly identify as being gay – and would not be captured in those studies. For example, the former CFO of Grindr via a Tegus call mentioned that 80% of the user base is anonymous. We’ve seen figures that around a quarter of Grindr’s user base is closeted. These users are on the app but are not being captured in the sanguine demographic numbers, which may overstate the attractiveness of the userbase from a monetization standpoint (particularly for advertisers, which we’ll touch on later).

There is also a common perception, particularly from those who have studied the hetero dating apps, that Grindr’s user base is concentrated in the coastal metropolises such as SF, LA, and NYC. The company has refuted this, stating that the user base is more evenly distributed across the country:

“So we're actually everywhere. And even in the U.S. people might have perception that, hey, like, probably more heavy on the coast. It's actually not. Incredibly, there's a very heavy set of people who are in the middle of the country, big cities in the country, and also rural areas in the country. And frankly, people in rural areas might be using Grindr more actively because that's like their only outlet. Like there's not even a gay bar that you can go to, right?” – George Arison (CEO), The Citizens JMP Securities Technology Conference 2025

User experience walk-through

We think that it’s always helpful to interact with consumer-facing apps to better understand the product. Below are the initial login and profile creation screens for Grindr.

Source: Grindr App

Notably, one can create a user profile with no photos and no information about themselves. This is very different to the big three hetero apps (i.e., Tinder, Hinge and Bumble), which all require photos. Tinder recently in many regions now requires users to upload at least one face photo. The onboarding process is slower and more involved for these hetero apps: on the 1Q23 earnings call, Match Group mentioned that Tinder new user onboarding takes three to four minutes, and for Hinge the process can take 5x longer, implying a 15-20 minute sign up time as users spend more time inputting information to complete their profiles. Grindr is the antithesis of this, taking just a few minutes to get up and running. There are reasons for this.

Grindr intentionally allows very minimal profiles due to some of the nuances of the gay community it is serving. In certain areas, especially where being gay is stigmatized or even illegal, users prefer not to show their faces publicly. This is widely understood and accepted on gay dating apps, unlike hetero apps, whereby not having a bio or clear photos would be a dealbreaker. From our observations on the app, many Grindr users have just a photo (some don’t even show their face – they might use a torso picture or omit a picture of themselves altogether) and a short text bio, in addition to basic stats such as age, weight, height, and HIV status. Below is an example of a Grindr profile layout:

Source: Grindr App

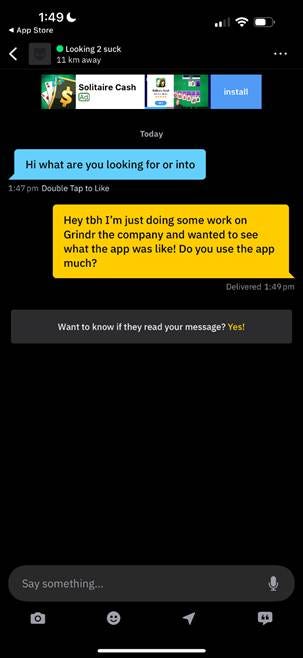

In our interaction with the app, we uploaded a totally blank profile – it had no photos or text. Within minutes the profile had users sending direct messages to it. Some said simply “hi”, while others sent scantily-clad photos of themselves with no text. From this, it is clear that anonymity is no constraint in receiving interest from other Grindr users. If you are in close proximity to other Grindr users, they will message you to find out more, which might lead to a more involved exchange where photos are shared, and other preferences are divulged. Below is an example of an anonymous user called “Looking 2 suck” who messaged our completely blank profile within minutes. Note the low quality banner ads that litter the page.

Source: Grindr App

A key drawback from this approach is that bad actors (think bots, catfishes, or scammers) can operate under the cloak of anonymity, with no verification required to filter out nefarious actors. While Grindr’s management team incessantly states that the app is only for users that are over the age of 18, there are cases of underage boys using the app which puts them at risk of sexual exploitation and trafficking. There have been over 100 men across the U.S. that have faced charges since 2015 related to sexually assaulting or attempting to meet up with minors for sex on Grindr[7]. This puts GRND in a bind: should it enable widespread anonymous use of the app to continue its strong MAU growth, or should it require stricter verification to foster a safer community, but then risk losing users who would not be on the app but for the ability to interact anonymously? It has chosen the former approach, and the company’s age verification protocols are laughable.

No matching needed

Tinder, Hinge and Bumble use the double-opt in matching system: you swipe on profiles (or like/comment on Hinge prompts) and only if both express interest is a conversation initiated. This introduces friction, with users, especially men, needing to wait for matches. On Grindr, however, there is no matching required. Every user in your vicinity is listed in a grid; you can tap anyone’s profile and send them a message instantly. The result: Grindr users tend to initiate chats quickly and with many people.

As we mentioned, it is not uncommon for a Grindr user to be bombarded with messages within minutes of logging in. In contrast, a male user on Tinder might swipe for days without a single match. Grindr’s open chat model leads to a flood of interactions that drives up engagement (i.e., more chats, more time in the app), and is a free-for-all environment that’s more akin to a crowded house party than a curated speed-dating event.

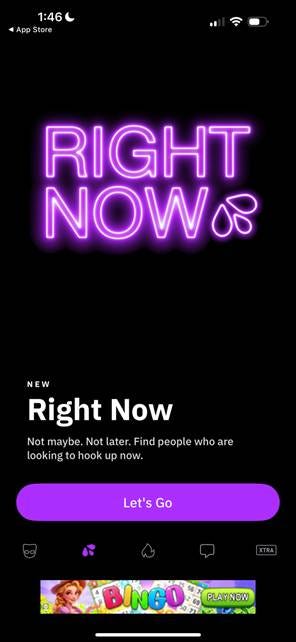

Right Now

Grindr has a feature called Right Now. As the name suggests, it is for users who are after a hookup right now. This feature is located in a separate tab within the app.

Source: Grindr App

Grindr has also introduced the Right Now feed, which shows users in close proximity who are also looking for a hookup:

Source: Grindr App

Roam

Below we can see a pop up prompt to introduce users to Grindr’s “Roam” feature, the first new feature on the company’s Investor Day product roadmap which was rolled out in Q3 of 2024. Roam lets users port over to different locations to interact with a new set of users. This feature is particularly useful if a Grindr user is traveling somewhere and wants to arrange some meetups ahead of time. Also note that during their Investor Day in 2024, the company disclosed that 27% of their weekly active users (WAUs) were traveling, meaning that this feature should be one that users derive sufficient value from to consider paying for it.

Source: Grindr App

As an aside, we think that it’s remarkable that GRND is only now rolling out a travel feature in the app. Tinder rolled out its Passport feature back in 2015[8]! Grindr’s management team blames the tardy rollout of elementary features on technical debt that the company is still in the process of addressing:

“There was a lot of technical debt and a lot of effort was put in and it continues to be put-in in solving the technical debt. So for the first couple of years, it was really impossible to build new product because you had so much technical debt to deal with.” – George Arison (CEO), Goldman Sachs Communicopia Conference 2024

While this means that the cadence of product rollouts should accelerate once this technical debt is remedied, it also creates execution risk in the event that these product bugs take longer to be fixed.

How Does Grindr Make Money?

Grindr’s business model is a freemium subscription model augmented by advertising. In other words, the app is free to download and use at a basic level, but generates revenue through paid premium subscriptions and in-app purchases (that’s the “direct” revenue), as well as selling ad space in the app (the “indirect” revenue). This is broadly similar to other dating apps – Tinder, Hinge, and Bumble also rely on freemium models – but the particulars of Grindr’s monetization differ slightly due to product differences. Direct revenue comprised 84.4% of GRND’s FY24 revenue mix, with the remaining 15.6% of GRND’s revenue coming from Indirect revenue (i.e., advertising). GRND has an unusually high advertising revenue mix. Consider that Indirect revenue for Match Group represented less than 2% of total revenues.