Starting a Fund (the Good and the Bad)

Musings on the fund launch journey

Welcome to Bristlemoon Capital! We have written previously on PINS, BROS, MTCH, CPRT, RH, EYE, TTD, and META. Our next deep dive will be on PAR. If you haven’t subscribed, you can join 2,230 others who enjoy our deep dives and investment insights here:

This post was inspired by a tweet I wrote to document and reflect on the Bristlemoon Capital fund launch journey, capturing both the good and the bad. The tweet attracted a decent amount of interest, receiving over one million views on X (Twitter). This post expands on that tweet, adding further color and thoughts.

As an aside, the Bristlemoon Global Fund will launch on 1 July 2024 and applications for wholesale investors have now opened. Further information can be found at www.bristlemoon.com and enquiries can be made at info@bristlemoon.com. Please feel free to forward this on to any wholesale investors who might be interested.

Starting a fund means starting a business

Roughly a year ago I left my job at a hedge fund in New York to start my own fund, Bristlemoon Capital. Unsurprisingly, launching a fund is very hard. It requires execution on multiple fronts: constructing and managing a portfolio, navigating the operations/ legal/compliance buildout, capital raising and building a brand, and then eventually managing a team as the assets under management scale. Often it feels like you are doing the jobs of multiple people. In fact, in the early stages, you are doing the jobs of multiple people. These roles also require very different skillsets.

A good analyst does not automatically convert to being a good portfolio manager, and being a good portfolio manager does not mean you will be a good leader of a business. Managing people is very different from managing a portfolio of stocks. And merely analyzing a business is different from having the autonomy and accountability for all investment decisions. Navigating the various business startup hurdles requires introspection to recognize and acknowledge your strengths and weaknesses.

Do you remain calm under pressure and effectively manage stress? Do you enjoy working with people? Are you someone who can create buy-in to your vision for the business amongst both employees and external stakeholders? Your weak spots will be exposed by the pressures of starting a business; it’s best to know beforehand where you have shortcomings so that you can look to address them (for example, by hiring people into the business with complementary skillsets).

Starting a fund means starting a business, and this means being an entrepreneur. You are creating something from nothing. Running a fund isn’t simply picking stocks. Rather, it involves being responsible for a multitude of decisions, both big and small, as well as portfolio and business-related. When you are an analyst within a fund, there is someone above you making those decisions. In effect, you are shielded from the cognitive load of dealing with the many managerial decisions.

Actioning these decisions requires both decisiveness and being strategic in driving forward outcomes. You need to be highly self-motivated because the onus falls entirely on you to will the fund into existence. This creates a mental burden that is very different to if you were working as an employee in a business, with a more clearly (and narrowly) defined set of responsibilities.

The realities of launching a fund

Most likely, you will be constantly thinking about the fund and all the things you need to do, probably in an obsessive way. This drive to get the business going has seen me working seven days a week, often late into the evening. There have been no holidays. The upside is that there is a deep sense of purpose and fulfilment derived from this; it doesn’t feel like work.

Pushing yourself hard requires understanding your limits and carefully managing yourself within those limits to avoid burnout. I am vigilant about exercising regularly, eating well, and getting enough sleep, but this can be disturbed more easily than before when I was working as an analyst at a fund.

To those thinking about starting a fund, the mental burden of running a business should not be underestimated. There is no shutting off. Mentally checking out and going on a two week European vacation just isn’t really possible when so many aspects of the business, and portfolio, require your daily attention.

Embarking on the fund launch journey requires not just buy-in from yourself, but buy-in from your partner and family. You will have less time for them and the stresses of launching a fund can affect the quality of that time you spend together. Unfortunately, it can be hard to be present when your mental bandwidth is limited.

If you are contemplating starting a fund, you need to determine whether you want to take on the stresses and uncertainty that come with a fund launch. It’s best to be realistic about what’s involved and acknowledge that the fund launch journey is an inherently challenging one.

The upside

The good thing is that there is a much stronger nexus between your effort and the financial value that accrues to you. This is a strong motivator, but so is the sense of purpose and pride from building something of your own. It is hard to describe the mindset shift that occurs when you are building your own house, versus someone else’s.

A fund is a platform that attracts opportunities. Since setting up Bristlemoon we've had private deals come our way. There have been companies enquiring to rent our Australian Financial Services Licence. There have been opportunities to appear on podcasts. You do not get the same inbounds working as an analyst at a fund. Someone above you is fielding those opportunities and is more likely to reap the value from them.

A potentially underappreciated aspect of starting your own fund is how incredibly motivating it is. The learning curve is steep and it’s difficult to communicate how fulfilling each day of the journey is.

Raising capital

The biggest gating factor to launching a fund is capital. Capital is the lifeblood of a funds management business – without it you will lack a sustainable enterprise. Raising capital requires building trust, often with people you’ve only recently met. This is a very different skillset from stock-picking and building that trust with investors falls squarely on you.

Can you communicate articulately? Can you convey your point of differentiation and strategy in a clear manner that resonates with investors (who will range from sophisticated to unsophisticated)? Do you present as trustworthy? Do investors like you?

This is perhaps the most perverse part of this business. Those that can spin a story can often raise real money, even in the absence of any investing acumen. Conversely, there are some phenomenal investors who struggle to raise capital because they are weak at selling themselves.

As much as you might like to outsource the capital raising so that you can focus on stock picking, you can’t reasonably expect to fully extricate yourself from the marketing process; high net worth individuals and family offices want to meet you, the person responsible for making the stock calls. It is you and your judgment who they are backing. Outsourcing your marketing responsibilities to a salesperson frankly won’t cut it.

If you hate talking to people and can’t stand the thought of selling your story and expertise to new people on a regular basis, then you should either not start a fund, or you should partner with a co-founder who is more amenable to the required capital raising duties. The upside from the time spent marketing is you will forge genuine connections and rapport with the people entrusting you with their capital.

Give yourself enough time

The capital raising journey is characterized by randomness and non-linearity. The process does not lend itself to planning; it is not as simple as writing down a list of prospective investors and then contacting said prospective investors. I tried this. It got very little traction. Family offices get a lot of inbounds and won’t talk to you without a warm referral. Raising capital is more akin to a thread you unravel: you’ll meet someone who makes an introduction to a person in their network, and then that new person might refer you to someone else. These interactions tend to expand concentrically. They also take time.

While you might have a capital raising timeline for your fund, the serendipitous way in which these interactions unfold means that you typically must acquiesce to other people’s timelines. A prospective investor might be traveling overseas for all of January. Or perhaps they’re not great at checking emails and require a polite follow up before they respond. Capital raising adheres to the self-referential adage of Hofstadter’s law: the process will always take longer than expected, even when Hofstadter’s law is taken into account!

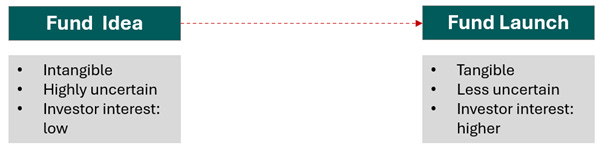

From the outset, it is incredibly difficult to accurately underwrite how much money you'll be able to raise. This can be daunting. It’s important, however, to step into the shoes of prospective investors and empathize with their allocation decision. Let’s say you have just an idea to start a fund but have not taken any steps to bring that fund into existence. From the perspective of an investor, the idea of agreeing to wire money to a bank account for some nebulous pipe dream is likely to be unappealing. You have to make it real. You have to create something tangible that others want to be a part of.

Source: Bristlemoon Capital

Investors will want to know the fund’s strategy and see evidence of the fund coming to life. This is reflected in common questions that investors will ask. What is the fund structure and who are the service providers you are using? Do you have an AFSL? When is the launch date? What level of capital commitments do you currently have? What level of launch AUM are you targeting?

Prospective investors are like penguins on an ice block: no one wants to be the first to jump in, but once one jumps into the water, others are more likely to follow.

Source: Fodors Travel Guide

You need to create reasons for investors to want to take the plunge. This requires taking the plunge yourself and plowing ahead with what might only be limited investor interest initially. If you don’t back yourself, why should anyone else be willing to back you? You likely won’t want to initiate the fund setup process, and bear the associated costs of this, without a clear line of sight on raising money from investors. However, you probably won’t be able to build investor interest unless you show that you are all in on this committed to moving ahead with the launch.

With time, and more concrete evidence of the fund coming into existence, it should become easier to get traction with investors, and you should get a clearer idea of how much money you are likely to raise. The initial uncertainty slowly gives way to a sharper image of how the business could take form.

Playing on hard mode

It should be noted that if you launch a fund in a bootstrapped way, which is what Bristlemoon is doing, then you will be playing on hard mode. You will be funding the venture from your own savings. This also means that you should plan for the worst and keep your fund’s cost structure to a minimum. Depending on your circumstances, you might also need to contain your personal expenditure. I have been putting together the pieces to launch Bristlemoon for almost a year without a salary, necessitating a ratcheting down of personal expenses.

My monthly credit card bill is now a quarter of what it was when living in New York. There are no big ticket discretionary purchases. Almost all meals are cooked at home. While many of these cost savings might be marginal, it all adds up. More importantly, it instills a mindset of frugality that will permeate the spending decisions you make when running the fund. Keeping a tight lid on costs is essential to lengthening your runway, giving you the time needed to build a track record and continue raising capital.

The upside of launching a fund can be great, but it doesn’t come for free. Playing on hard mode with a bootstrapped launch does involve sacrifices, but it is the difficulty of the journey that makes you care deeply about what you’re building. Besides, these “sacrifices” aren’t too severe in the grand scheme of things; no one is going to shed a tear for the fund manager cooking meals at home rather than eating out! Chances are if you are even contemplating starting a fund, you’re in an incredibly privileged position – be grateful for every day you get a shot at building your business.

The trust and credibility problem

Launching a fund is characterized by the chicken and egg conundrum: you need capital to build a track record; and to raise capital, you need a track record. Investors will use an investing track record as a heuristic for assessing your investing competence. This is perfectly reasonable, but it's also an imperfect approach.

An investing track record is only a proxy for an investment manager’s skill. This is because luck plays a varying role in every investment outcome; the vagaries of chance can positively or negatively intervene and reduce the quality of signal derived from an investor’s historical portfolio performance.

Luck can cause investors with a poor investment process to chalk up phenomenal investment returns, sometimes for years on end. Despite its flaws, investors still like to see a track record, and it is usually better to have one than not have one. While you don’t need an investing track record to start a fund, its absence will likely create a trust and credibility problem when you go to raise capital from investors.

The lack of a marketable track record simply makes it harder for someone to assess and get comfortable with your investing aptitude. More specifically, it makes it harder for investors to determine a priori whether you're going to make them money. Again, this doesn’t make it impossible to raise money, but you will need to prove to investors that you are thoughtful about investment decisions and will not take foolhardy risks.

Turning stock research into marketing

Bristlemoon has sought to communicate its approach to investing via this newsletter, one that publishes 40-70 page deep dives on companies as well as ancillary investing thought pieces. We took the view that the benefits from being transparent greatly outweighed keeping our intellectual property out of the public domain.

By publicizing our work, we've been able to fast-track that process of investor education about our investing approach and have done that at scale. It’s changed the nature of conversations we have with prospective investors as it has allowed them to read our analysis and build comfort that there is a deep amount of thought that sits behind each investment decision.

Absent the newsletter, we would have needed to educate investors about our investing ability on a one-to-one basis. This would have been laborious and difficult to manage, particularly given the many competing time commitments when starting a business. By tapping into the scale of the internet, the newsletter shifts this investor education from a one-to-one basis to a one-to-many basis.

The beauty of this is the content we publish is synergistic with the analysis we’d be doing anyway in managing the portfolio. In effect we are turning stock research into marketing. The newsletter also serves as a regular touchpoint with investors that helps keep them in the loop with our thinking. Without it, it would be easy to be forgotten about, and attempting to communicate one-on-one with investors at a comparable frequency would have likely created an internal resourcing problem.

We would go so far as to say that without the newsletter, our chances of launching Bristlemoon would have been vastly diminished. We’ve been fortunate to secure a healthy number of investor commitments and have had inbounds from investors looking to invest with us via the newsletter which is encouraging. While it is no panacea, and writing stock research is still very different from running a fund, we believe that putting our research in the public domain has to an extent helped assuage the trust and credibility problem.

We are immensely grateful for all the support and wish others who are thinking of embarking on the fund launch journey nothing but success. For some great threads on X (Twitter) that talk about launching a fund or joining a startup fund, the following resources are excellent:

Disclaimers / Disclosures

The information contained in this article is not investment advice and is intended only for wholesale investors. All posts by Bristlemoon Capital are for informational purposes only. This article has been prepared without taking into account your particular circumstances, nor your investment objectives and needs. This article does not constitute personal investment advice and you should not rely on it as such. This document does not contain all of the information that may be required to evaluate an investment in any of the securities featured in the document. We recommend that you obtain independent financial advice before you make investment decisions.

Forward-looking statements are based on current information available to the author, expectations, estimates, projections and assumptions as to future matters. Forward-looking statements are subject to risks, uncertainties and other known and unknown factors and variables, which may affect the accuracy of any forward-looking statement. No guarantee is made in relation to future performance, results or other events.

We make no representation and give no warranties regarding the accuracy, reliability, completeness or suitability of the information contained in this document. To the maximum extent permitted by law, we do not have any liability for any loss or damage suffered or incurred by any person in connection with this document.

Bristlemoon Capital Pty Ltd (ABN: 22 668 652 926) is an Australian Financial Services Licensee (AFSL Number: 552045).

George Hadjia is associated with Bristlemoon Capital Pty Ltd. Bristlemoon Capital may invest in securities featured in this newsletter from time to time.

It is lots of hard work. As you say raising capital isn't linear but once you keep knocking on doors eventually things lead to other things. Sometimes life surprises you in good ways. Good luck!

Great read thanks. Did you consider just running your own capital to build a track record - letting the 'product' speak for itself and thus worrying less about marketing and capital raising?