The Perils of Short Selling

Why shorting is a hard way to make money and how Bristlemoon approaches shorting

Welcome to Bristlemoon Capital! If you haven’t subscribed, you can join 1,580 others who enjoy our deep dives and investment insights here:

Enron. It is a word that immediately brings to mind one thing: fraud. In August of 2000 Enron’s stock fetched $90 per share. In December of 2001 the company declared bankruptcy, and its stock traded for less than $1 per share before being delisted from the New York Stock Exchange. For those making a foray into the world of shorting stocks, Enron might seem like the poster child for the perfect short: a highly-levered, fraudulent business that saw 99% of its value wiped out in a little more than a year. However, as we will explore, what might seem like the best shorts are often the most dangerous.

Imagine that you just landed your first buyside gig at a hedge fund. Your portfolio manager tasks you with building a quant screen to generate ideas that the fund can short. Fun! What criteria would you choose for this quant screen? Perhaps you’d look for stocks trading at 52-week highs, with elevated price-to-earnings ratios, and with highly levered balance sheets. If any of these stocks turn out to be frauds, then even better! Or so you might think.

Frauds

Let’s start with why frauds are actually some of the worst types of shorts. They are fool’s gold: they hold immense promise for outsized investment gains once the fraud is exposed, but the journey towards that payoff is often a painful one. Every fraud is based on a lie. And the worst frauds feature a gaping disconnect between the reported financials and the underlying financial reality of the business.

The problem with shorting frauds is two-fold:

If a management team is lying about the true financial state of a business, there’s nothing stopping them from concocting even more egregious lies in the future; and

The time horizon over which the short will pay off is often unclear.

Think of it this way: you might be right, but an unscrupulous CEO’s lies could propel the stock to heights that force you out of the trade. As the price of the stock rises, your exposure to that short position also grows. The prudent short seller will be forced to risk-manage the position and reduce that exposure by covering some of the short position. This results in the crystallization of losses along the way before the broader market agrees with you that the company is indeed a fraud (and thus dumps the stock). So, you might eventually be right. But being right on a short is a pyrrhic victory if it ends up blowing a hole in your portfolio.

To profit from a fraud, you need to have an adequately sized short just at the right moment. This is because frauds often break rather suddenly. People tend to not want to own fraudulent businesses, and head for the exits en masse. This could be catalyzed by an SEC investigation, or even a well-researched short report from a credible outfit (there is of course a spectrum here – your Tweet might fail to hold the same gravitas as if John Hempton or Hindenburg Research publicized similar conclusions). The key point is that timing matters, and it’s very hard to get the timing right on these sorts of shorts due to the very narrow window in which a fraud short will be monetized.

There are numerous examples of hedge fund luminaries being lionized for correctly shorting stocks that turn out to be frauds. The accolades often miss the fact that while those investors’ conclusions proved to be correct, there is minimal look-through as to how much, if any, money those funds made on that trade. Often these “successful” short trades hold more marketing value than financial value for funds.

Given that shorts are often, and very much should be, sized smaller than longs for risk management reasons, the financial payoff is likely far less than what the media attention would suggest. For example, a 150 basis point short position that falls 50% will produce just 75 basis points of investment gain. This is an amazing outcome for a short but fails to account for the losses incurred along the way as the position was trimmed. Even the full 75 basis points provides only a modest contribution to the overall performance of a portfolio.

We don’t try to short frauds – it goes in the too hard basket for us. It takes an immense amount of work to correctly uncover a fraudulent business, and the financial payoff is unclear for the reasons we have noted above. We respect and admire those that can identify and profit from frauds consistently. To those that do insist on shorting frauds, it is best to not be a visionary but rather a fast follower. If possible (assuming you can borrow the shares and the cost of borrow doesn’t become usurious), one should consider only shorting fraudulent stocks in the event that the market has already begun to recognize the fraud in earnest.

Shorts with bad balance sheets

The budding hedge fund analyst tasked with building the quant screen frantically scratches out “look for fraudulent companies” from their notepad. They proceed down their list to “companies with a lot of debt”. It might seem logical to look for shorts with highly levered balance sheets. Debt, after all, can accelerate the compression of a company’s equity value when the fundamentals erode. However, more debt is not always a good thing from the perspective of finding attractive shorts.

This is because debt is an amplifier. While it can hasten the decline of a failing business, a highly leveraged company can also rally spectacularly if the market were to suddenly turn cheery about the future of that business. Thus, higher levels of debt typically cause greater levels of volatility in a company’s equity value. This is something that must be considered when constructing a short portfolio. Being too exposed to highly leveraged shorts can make your short book trade like a yo-yo.

The higher the leverage for the companies you’re shorting, the more sensitive your short book will be to changes in interest rates. This is fantastic when interest rates are rising, and the rising interest expense eats away at profit margins. It can also be catastrophic when interest rates are decreasing, or even believed by the market to be on a path to decreasing.

While this might all seem like a moot point if you have patient capital that can look through volatility, we would argue that there is no such thing as patient capital when shorting. After all, you are borrowing those shares and must adhere to the rules of whoever is lending those shares out to you. If the stock rallies high enough, your broker will require you to post additional collateral to replenish the maintenance margin (that is, the minimum equity an investor must hold in their margin account after shorting the stock). Extreme volatility isn’t something you simply ride out when shorting stocks. That can kill you. Rather, higher volatility increases the likelihood that you will need to risk manage – that is, trim – your short position and incur losses.

Another dynamic to be wary of for highly levered companies is when the market value as a percentage of enterprise value significantly compresses, the volatility of the equity is likely to significantly increase. Often when the market value as a percentage of enterprise value falls below 20%, the specter of bankruptcy draws closer, and the company’s bonds will likely trade at a discount. The implication is that there’s a real risk that the equity gets wiped. This causes the stock to start trading like an out-of-the-money option. Think of the stock as a loaded spring that can exhibit violent upward price movements on even modestly positive news flow. These stocks are extremely dangerous and we do not try to short them.

Shorting a stock all the way down to bankruptcy might sound appealing as a way to squeeze all the juice from the short idea. However, the last mile of the journey is dangerous due to the abovementioned dynamics, as well as the risk that the short trade becomes crowded and the cost of borrow (i.e., how much a prime broker who is lending you the stock is charging you in that arrangement) can spike. For example, Sears’ cost of borrow soared to astronomical levels as the company careened towards bankruptcy, reaching north of 50%.

Sometimes the cost of borrow can reach ridiculous levels even outside of bankruptcy situations. Consider Trump Media & Technology Group (Nasdaq: DJT) in March 2024; the company had a 157.6% cost of borrow fee, a result of it being the most shorted SPAC in the U.S. according to S3 Partners. If that’s the annual cost to short DJT, you’d better hope that the share price drops very quickly!

Stocks that are expensive

The young buyside analyst, somewhat befuddled as to what constitutes a good short, reasons that if buying undervalued companies makes sense, surely you can just do the opposite and short overvalued companies. Those new to short selling often approach shorting as simply inverting what they do on the long side. When buying a stock (i.e., going long), the dictum of buy low and sell high is sensible. Merely inverting this logic when shorting, and simply shorting expensive stocks, is downright dangerous. If an articulation of your short thesis on a stock starts with “it trades on a high P/E”, then you should perhaps reconsider the trade in the absence of any other strong points that substantiate a credible, and imminent, downside case.

For stocks that are “overvalued”, you are simply playing for mean reversion to a normalized earnings multiple at which the stock has historically traded (if the stock has always traded at its current high multiple, then even this mean reversion logic cannot be used as a rational basis for shorting the stock). The problem with shorting purely on the basis of overvaluation is that expensive stocks can not only remain expensive, they can get even more expensive.

You might think that a low-growth industrial parts distributor trading on 50x earnings is silly. It probably is, but there’s nothing stopping it from getting even sillier. In fact, if investors have shown a willingness to buy the stock at a nonsensical multiple, then they have already displayed a disregard for the fundamentals. There is little that can stop this suspension of disbelief from pushing the stock to a 100x P/E, or even 200x. Shorting these sorts of stocks might be tempting but can be like picking up pennies in front of a steam roller.

Why short stocks at all?

Shorting is a very difficult way to make money. The odds are structurally stacked against you. When you buy a stock your upside is uncapped and the most you can lose on that investment is 100% of your capital. For shorting, it is the precise opposite. The most you can ever make on a short trade is a 100% investment gain (often it is a lot less, as shorts typically are not maintained down to bankruptcy), but your potential losses are unbound. This is worth repeating: your potential losses for any short trade are infinite. Also consider the fact that equity markets on average have increased by 10% per annum. This makes for quite the challenge in making money from shorting. So why short at all?

We view shorting as simply another way to make money. We can utilize our insights about an industry and companies to profit not just from buying great businesses, but shorting poor businesses that are deteriorating. However, in acknowledging the difficulty and structural pitfalls of shorting we noted above, we seek to be opportunistic in our approach to shorting. We don’t have a standing short book and are perfectly comfortable having zero shorts if there’s a paucity of compelling ideas. Rather, we look to short opportunities that we believe will generate positive P&L dollars (as distinct from short alpha, which is valuable if a long and short book are structured correctly).

Our intent is for our short trades to be 1) profitable in aggregate over time; and 2) give us the flexibility to protect on the downside in select situations. This is a high bar, and we would note that shorting is not a large focus at Bristlemoon. The majority of our time is spent finding great businesses that can compound our investors’ wealth over many years. But if a great short comes on our radar that we can readily diligence, we want the flexibility to act on that to profit on behalf of our investors.

Lastly, as we build out the Bristlemoon investment team over time, we think that the ability to short is a positive from a talent attraction and retention standpoint. Many of the brightest investors enjoy the intellectual pursuit of shorting and have a desire to build this skillset (albeit it will be a limited portion of their research time at Bristlemoon). We believe it is good for analysts to get exposure to bad businesses and uneconomic business models. This breadth of experience can help them form a greater appreciation for good businesses, and the process of shorting is one that we believe encourages intellectual honesty.

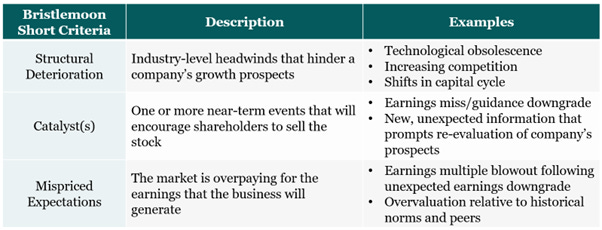

Bristlemoon short framework

Bristlemoon employs a three-part framework to shorting, as presented below. Basically, we want to short deteriorating businesses with an imminent catalyst that will cause investors to realize they have grossly overpaid for the stock.

Source: Bristlemoon Capital

Ideally our short book will consist of bad businesses in bad industries that are already showing signs of struggling. A weak, structurally declining industry means flagging industry growth rates and lower odds of that company producing earnings that can appease the market.

While not a hard rule, we prefer not to short quality businesses. These businesses are usually far more resilient, and a good management team can manage a difficult period in ways that might reduce the likelihood of material earnings downgrades (this is both in terms of deftly managing the actual business, as well as properly managing investor expectations). Furthermore, the shareholders in high quality businesses are also more likely to look through any near-term weakness, given they are holding that business for its long term compounding potential. This is distinct to shareholders of a poor quality business that are likely playing for a valuation multiple arbitrage; they don’t have loyalty to that business and are far more likely to abandon ship when the waters get choppy.

Shorting is so difficult because it requires not just an analysis of the fundamentals of a business, but it requires empathy. It is not enough to just short deteriorating businesses. You need to short a business that’s deteriorating more so than what other investors were expecting. You need to empathize with how others are viewing that stock. The perfect short is where new information comes to light that is so ghastly that it causes the longs to lose faith in their investment thesis, and subsequently dump the stock. We require each of our shorts to have one or multiple near-term catalysts so that we can get paid quickly on our short. A multi-year holding period for a short does not interest us.

Risk management protocols

Part of the Bristlemoon name derives from the importance of surviving. This means being around long enough for compounding to work its magic. For this reason, we have a stringent risk overlay for our short book to limit our losses. We have preordained risk budgets for each short. This is essentially the maximum amount of money we would tolerate losing on any given short. The risk budget is calculated as 15% of the maximum position size we would take for that short. The maximum position size (and thus the risk budget) depends on the risk/reward skew and other factors. It is subjective.

For example, for a short position in a company where the maximum position size is 120 basis points, then the maximum allowable loss would be 18 basis points. This means that once an 18 basis point loss has been incurred, we must exit that position. We enact this framework by systematically trimming and exiting the short at different loss levels. This involves halving the size of the short position if the price of the stock increases by 10%. If the price increases by 15% from our cost base, we will exit the short position.

Source: Bristlemoon Capital. While we have been specific in quantifying our shorting risk framework, we reserve the right to make adjustments over time.

These are admittedly very tight risk parameters. However, the idea of this risk framework is not to maximize the money we can make while shorting. It is to contain losses that could otherwise destroy our performance and put us out of the race. This risk management overlay also forces us to carefully contemplate the timing of the short. Why now? What are the chances that the short will run against us? How much conviction do we have that our short catalyst will play out as envisioned and be recognized by the market in a way that causes the trade to work?

The risk with this framework is that once a short is covered due to a price rally, there will be a temptation to re-enter the position at a higher price. But this temptation to reinitiate the short will be overruled if the risk budget has been exhausted – in other words, we already used up our dry powder on that short position. These risk budgets do reset after six months. The reason for this is that six months is a long enough period to take us out of the heat of the moment and reset our emotional compass, and there’s a higher chance that the momentum fueling the rally will have faded.

Successful short selling requires discipline. It takes discipline to stick to this risk framework. There will be periods where you get stopped out of a short when you know you are right. But being right doesn’t matter if no one else in the market agrees with you. We are okay forgoing gains on a short to sleep at night knowing that our short book won’t kill us. Julian Robertson, the late founder of Tiger Management and father to many Tiger “cubs” and “grand cubs”, had a stringent interview process for investment team members. One question that was routinely asked was “Would you prefer to be intellectually right but lose money or to be intellectually wrong but save the trade?” When shorting, we would rather “save the trade” and avoid outsized losses. Having a strict risk framework helps us avoid the temptation for our egos to override our better judgement.

Disclaimers / Disclosures

The information contained in this article is not investment advice and is intended only for wholesale investors. All posts by Bristlemoon Capital are for informational purposes only. This article has been prepared without taking into account your particular circumstances, nor your investment objectives and needs. This article does not constitute personal investment advice and you should not rely on it as such. This document does not contain all of the information that may be required to evaluate an investment in any of the securities featured in the document. We recommend that you obtain independent financial advice before you make investment decisions.

Forward-looking statements are based on current information available to the author, expectations, estimates, projections and assumptions as to future matters. Forward-looking statements are subject to risks, uncertainties and other known and unknown factors and variables, which may affect the accuracy of any forward-looking statement. No guarantee is made in relation to future performance, results or other events.

We make no representation and give no warranties regarding the accuracy, reliability, completeness or suitability of the information contained in this document. To the maximum extent permitted by law, we do not have any liability for any loss or damage suffered or incurred by any person in connection with this document.

Bristlemoon Capital Pty Ltd (ABN: 22 668 652 926) is an Australian Financial Services Licensee (AFSL Number: 552045).

George Hadjia is associated with Bristlemoon Capital Pty Ltd. Bristlemoon Capital may invest in securities featured in this newsletter from time to time.

Thanks for the article about shorting. Shorts appealed to me because it can help reduce portfolio volatile.

My experience is like what you described. I tried shorting based on accounting issues, but it turned out much more difficult than I expected. A lot of other factors like sentiment and short-term flows become important. Paul Marshall said that when a short position goes against you, it grows in size, making it a growing problem. Exactly like what you said