Meta Platforms (META) 2Q25: SuperMetalligence

Move over Metaverse, there’s a new money pit in town

Meta’s strategic investments in AI are yielding impressive results, fueling astonishing growth in all aspects of its business despite the law of large numbers. Emboldened by his company’s resurgence from the Metaverse nadir, Mark Zuckerberg now turns Meta’s high pressure cashflow hydrant to an even more ambitious mission. Shareholders are clearly giving Zuck enough rope, but we do wonder if the outcome will be different this time.

A blowout quarter for Meta

Meta delivered incredibly strong Q2 results and Q3 guidance that handily beat expectations:

Revenue growth of 22% YoY beating consensus by 6%, and a stable 2-year stack of ~44% growth for the past four quarters.

Operating income growth of 38% YoY and 500 bps of operating margin expansion on the back of ongoing cost controls and operating leverage.

EPS growth of 38% YoY to $7.14, smashing consensus by 21% and similar to last quarter’s beat.

Q3 revenue guidance of $47.5 to $50.5 billion or +17% to +24% YoY, beating consensus of $46.2 billion.

While P&L performance remains very strong, we see ongoing deterioration of cash results as capex continues to step up. Operating cash flow of $25.6 billion was largely absorbed by $17 billion of capex, resulting in just $8.5 billion of free cash flow. FCF margin is down to 18% and could potentially fall to 10% in 2026 given the capex step-up compared to 40%+ operating margin.

Source: Bristlemoon Capital, company filings

The 2025 capex guide was tightened slightly to a range of $66 to $72 billion representing an over $30 billion YoY increase at the midpoint. But the real kicker is the initial outlook for 2026, which is expected to step up to ~$100 billion! Yet even with this nearly 3x capex increase over two years, the company is still compute constrained per the CFO:

“But even with the capacity that we’re bringing online, we are still not quite perfectly meeting the demand that teams have for compute resources across the company.”

The biggest driver of the 2026 capex increase will be Gen AI instead of Core AI investments. When we spoke to the company last year, Core AI was still the majority of capex (2024 capex: $37 billion), and we suspect that this year the balance may flip. By next year, we expect the majority of capex to be for Gen AI initiatives, which don’t yet have a monetization timeline. While management still maintains that the capex is fungible between Gen AI and Core AI, our back of the envelope math suggests that at a quantum of $100+ billion capex every year (and growing), it may prove difficult to earn an adequate return on investment from Core AI advancements alone.

But before we consider the AI capex vs ROIC debate, it is worth highlighting how Core AI investments have been driving improvements across the business.

Core AI investments powering growth

For those who don’t follow Meta, Core AI is essentially the investments into the company’s recommendation and advertising systems that drive engagement and revenue across the core platforms. The improvements that stem from these investments are bucketed into two categories: engagement initiatives and monetization efficiency.

On engagement initiatives, the clearest indicator of success is the reacceleration of DAU growth over the past three quarters. Despite nearly 3.5 billion people already using Meta’s apps daily, DAU is somehow still growing at 6% YoY. This suggests to us that AI – whether it be through better recommendations or Meta AI itself – is driving higher daily engagement.

Source: Bristlemoon Capital, company filings

Other engagement improvements that were highlighted in Q2 include over 20% YoY growth in video time spent on both Facebook and Instagram, driven by enhancements to the recommendation systems. This comes on top of a 7% increase in time spent on Facebook and 6% increase on Instagram reported in the six months through Q1, which came on top of a 8%/6% increase in time spent on Facebook/Instagram in the nine months through Q3 2024. So there do appear to be strong incremental gains in time spent across the apps from better AI recommendations. The company is also making good progress on longer-term content ranking innovations such as cross-surface foundation models and extending LLM architectures into existing recommendation systems.

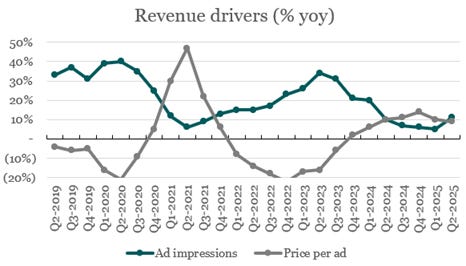

We generally subscribe to Ben Thompson’s (of Stratechery) view that ad networks are at their healthiest when revenue growth is being driven by ad impressions rather than price per ad. Strong growth of ad impressions supports robust ad revenue growth in future quarters, while an over-reliance on eCPM growth tends to degrade advertiser returns over time. For the past few quarters, ad impression growth had slowed materially while price per ad grew double digits, but in Q2 there was a meaningful inflection in ad impression growth driven by rising engagement on the core platforms and some further ad load optimization on Facebook. Meta has also started inserting ads into Threads and the WhatsApp Updates page, though these won’t be material contributors to ad impression growth this year (or next, for WhatsApp).

Source: Bristlemoon Capital, company filings

On monetization efficiency, CFO Susan Li noted that the 9% growth in price per ad benefited from improved ad performance, suggesting that underlying ROAS continues to increase. Susan spoke extensively about improvements to ad retrieval and ranking systems, each of which drove 3% to 5% increases in conversion on Facebook and/or Instagram. During the quarter, Advantage+ was also rolled out as the default option for sales and app campaigns, and adoption has been higher than expected.

"The Andromeda model architecture we began introducing in the second half of 2024, powers the ads retrieval stage of our ad system, where we select the few thousand most relevant ads from tens of millions of potential candidates. In Q2, we made enhancements to Andromeda that enabled it to select more relevant and more personalized ads candidates, while also expanding coverage to Facebook Reels. These improvements have driven nearly 4% higher conversions on Facebook Mobile Feed and Reels."

"In Q2, we improved the performance of GEM by further scaling our training capacity and adding organic and ads engagement data on Instagram. We also incorporated new advanced sequence modeling techniques that helped us double the length of event sequences we use, enabling our systems to consider a longer history of the content or ads that a person has engaged with in order to provide better ad selections. The combination of these improvements increased ad conversions by approximately 5% on Instagram and 3% on Facebook Feed and Reels in Q2."

We think it is easy for investors to dismiss or underappreciate small improvements to engagement and ad efficiency, especially when viewed against massive capex investments. But an 8% increase in time spent could, ceteris paribus, translate into a $15 billion increase in revenue, and a stack of 3% improvements to ad efficiency could support a 10% increase in eCPM with no degradation to ROAS.

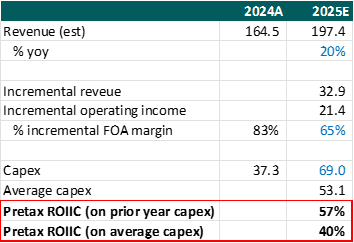

The example below shows how the cumulative benefits from Core AI investments can generate an attractive incremental pre-tax return on capital at current capex levels.

Source: Bristlemoon Capital

Finding religion in superintelligence

Moving on from Core AI, it is clear that Mark Zuckerberg has found his new messianic calling: to usher in the Metaverse superintelligence. From our perspective, it is interesting watching his descent into an AI maximalist. Throughout 2023, Zuckerberg appeared content to do his own thing with AI (open source, product-focused, school project-ish etc.) and let the frontier labs compete for the state-of-the-art models. In early 2024, Zuckerberg changed his position and believed Meta needed to pursue AGI. Fast forward to 2025, he has been on a multi-billion-dollar binge to acqui-hire the best AI talent in a bid to build superintelligence. This seems to be spurred by his observation of the exponential rate of AI progress (so far).

"I think it's basically just what we're continually observing how this works, what the trajectory or the pace of AI progress has been. I think it continues to be on the faster end. And that I think informs a lot of the decisions, from everything from the importance and value of having the absolute best and most elite talent-dense team at the company, to making sure that we have a leading compute fleet so that the people here can do, so the researchers here have more compute per person to be able to lead their research and then roll it out to billions of people across our products, making sure that we build and drive these products through all of the different things that we do, which I think is one of the things that our company is the best in the world at, is basically when we take a technology, we're good at driving that through all of our apps and our ad systems and all that stuff.

So, yeah, I mean, we're just going to push very aggressively on all of that, but, at some level, yeah, this is—there's sort of a bet in the trajectory that we're seeing, and those are the signals that we're seeing, but we're just trying to read it."

As Meta shareholders, it is not clear to us why Meta needs to achieve “superintelligence” (whatever that means) at all costs. We understand that Meta has enormous consumer distribution and cash flow, but we don’t understand i) why a personal AI assistant for the median human needs to be a “superintelligence”; ii) how a superintelligent personal assistant can realize its full potential without access to email, calendar, encrypted messages etc; and iii) how a highly engaging personal assistant does not cannibalize time spent on Meta’s monetized surfaces.

Even as we give Zuck the benefit of the doubt when it comes to (eventual) monetization, we have to wonder what it might look like. With OpenAI hiring Fidji Simo to build out an advertising business, it is evident that subscriptions alone are insufficient to cover the cost of a freemium service where the substantial majority of users are non-paying. Yet Meta’s engagement-driven ad model is not well suited to conversational use cases – WhatsApp ads sit in the separate Updates tab, and Susan revealed on the follow-up call that the company abandoned plans to introduce Messenger inbox ads after initial testing.

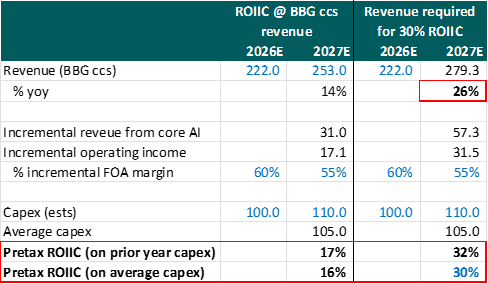

We believe Meta will ultimately figure out a sustainable monetization strategy for “superintelligence”, but the $100 billion a year and growing capex burden adds a certain level of urgency. Investors are currently cheering Meta’s strong P&L performance and letting the enormous capex outlay slide. But should revenue growth disappoint, we imagine the market reaction could be reminiscent of 2022, especially if Zuck is unrelenting in his pursuit of superintelligence. As we mentioned earlier, even if the Gen AI investments are fungible with Core AI, we struggle to see how forcing $100 billion a year of capex into the core platform can deliver adequate returns.

Source: Bristlemoon Capital, Bloomberg consensus

Two observations here: 1) a low-teens post-tax ROIIC is not yet value destructive in the sense that it is likely still above Meta’s cost of capital, but presumably shareholders would prefer buybacks; and 2) obviously if the superintelligence investment was not meeting internal expectations, Meta should cut capex. Our biggest concern is that instead of rationally reducing capex, an irrational decision is made to throw even more money at the problem (in line with current LLM scaling laws).

Disclaimer / Disclosures

The information contained in this article is not investment advice and is intended only for wholesale investors. All posts by Bristlemoon Capital are for informational purposes only. This article has been prepared without taking into account your particular circumstances, nor your investment objectives and needs. This article does not constitute personal investment advice and you should not rely on it as such. This document does not contain all of the information that may be required to evaluate an investment in any of the securities featured in the document. We recommend that you obtain independent financial advice before you make investment decisions.

Forward-looking statements are based on current information available to the author, expectations, estimates, projections and assumptions as to future matters. Forward-looking statements are subject to risks, uncertainties and other known and unknown factors and variables, which may affect the accuracy of any forward-looking statement. No guarantee is made in relation to future performance, results or other events.

We make no representation and give no warranties regarding the accuracy, reliability, completeness or suitability of the information contained in this document. To the maximum extent permitted by law, we do not have any liability for any loss or damage suffered or incurred by any person in connection with this document.

Bristlemoon Capital Pty Ltd (ABN: 22 668 652 926) is an Australian Financial Services Licensee (AFSL Number: 552045).

George Hadjia and Daniel Wu are associated with Bristlemoon Capital Pty Ltd. Bristlemoon Capital may invest in securities featured in this newsletter from time to time.

What's your view on the current Meta Oakley glasses and future Augmented Reality versions (e.g. future versions of Orion)?