Do You Dance While the Music Is Playing?

Reflections on changes in how stocks are being priced

Bristlemoon Chief Investment Officer, George Hadjia, was recently in Los Angeles, Omaha and New York, where he met with investors and allocators. Below is an update sharing some of the key insights from those conversations and how they inform our thinking on a market environment that continues to reshape the way stocks are priced.

Feel free to subscribe, and join 6,074 others who get our investment memos directly to their inboxes.

In my recent travels to the U.S., I had a lot of conversations with other investors who are grappling how to adapt to this market environment. Market environment is a bit of a nebulous descriptor, so it’s worth elaborating.

With multi-strategy funds (a.k.a. multi-managers or pods) capturing a disproportionate share of hedge fund AUM growth over the past decade, they have become a more important part of how liquid securities trade. Given how much these pods lever up their equity capital and the high level of portfolio turnover, increasingly the pods are the marginal buyer (or seller) of liquid securities. Layer on top of that the rise of passive and retail participating more actively in pockets of the equity market, and it’s not hard to see how these developments have changed the manner in which stocks trade. This is the change in market environment I am referring to.

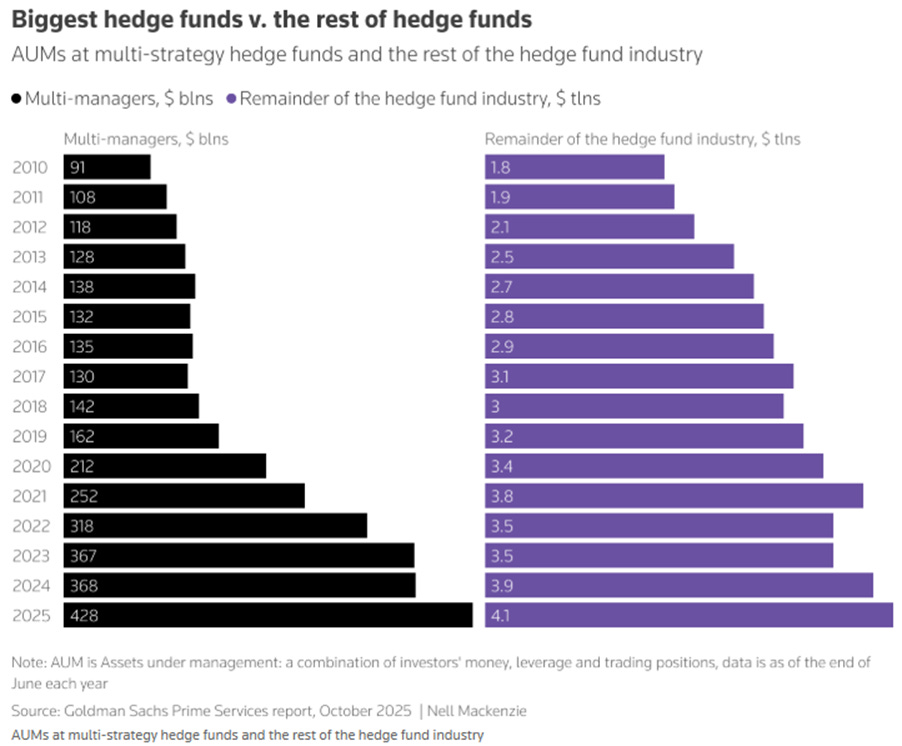

As we can see below, multi-managers account for around 10% of the total hedge fund industry AUM. Incredibly, the multi-strategy funds went from managing $91 billion of assets in 2010 to roughly $428 billion in 2025, a 4.7x increase in assets over the last 15 years.

However, data from the Goldman Sachs prime desk showed that multi-strategy firms accounted for around one-third of the gross market value managed by hedge funds in equities[1] (i.e., due to the leverage employed).

J.P. Morgan’s data for the month of November 2025 revealed that multi-strategy funds had leverage at 444.3%. In other words, for every $100 of capital from investors, the multi-strategy fund had almost $450 in long and short positions[2]. That’s a lot of leverage!

It’s thus no surprise that the pods operate within very tight risk parameters. They run market neutral (although some pods have flexibility to tilt their net exposure beyond strictly neutral), which basically means they need to net out their long exposure with an equivalent short exposure. With that much leverage and highly restrictive risk parameters, there is minimal scope for drawdowns.

There is no shortage of stories of pods being wound down if a manager blows through their risk limits. So, what this means is that the pods have minimal duration and have a strong tendency to be long the stocks that are “working” at any given time. The corollary of this is that the pods have an inherent bias towards being long momentum (bottlenecks, accelerating growth profiles, and the like).

If we think about the current market, the area of the tech sphere that is working (and in a gargantuan way) is semiconductors. The SOX (The Philadelphia Semiconductor Index) is up around 67% year-to-date, and some of the earnings beats during Q1 were simply eye-watering. If you’re a tech pod, you’re getting up and dancing while the music plays. In other words, you’re probably buying semis due to strongly positively inflecting growth profiles, good visibility into demand persisting (and there being little to derail near-term earnings beats), as well as just strong momentum in these stocks.

But, if you’re running market neutral like the pods do, you can’t simply buy semiconductor stocks and call it a day. You have to fund that exposure, and have an offsetting short book. Software and consumer internet names have been prime funding source candidates. We’ve previously noted that there’s been a lack of narrative nuance, with the tech landscape bifurcating into perceived AI winners and perceived AI losers. The way in which the multi-managers execute their strategies has likely exacerbated this dynamic.

Just take a look at the spread between the IGV and SOX. While the SOX is up c.67% year-to-date, the IGV (a software sector ETF) is down around 12%. That’s a 79 percentage point outperformance of semiconductors versus this software basket in less than six months.

This has split the fortunes of fund managers. If you’d owned a lot (or even just a little) of semi and AI-beneficiary companies, your Fund is probably shooting the lights out. If you had been caught on the wrong side of this trade, it’s likely a completely different story, with a different set of conversations with clients. I have never witnessed a period in markets where capital has rotated from one sector into another at such a scale and in such a short period of time. It feels truly unprecedented.

We admittedly have had too much of what was in the IGV, and too little of what was in the SOX. And that’s hurt our year-to-date performance. I’m not writing this to lament this soft run of performance, and I’m also not blaming the market (as they say, “no crying in the casino”). Rather, I thought this was a good opportunity to relay the thoughts and discussions that flowed from conversations I had with investment managers who I met during my travels to the U.S., many of which were grappling with similar challenges in navigating this market.

How are managers adapting?

One of the biggest challenges is that in order to keep up in this hot market, it has required most fundamental managers to pivot dramatically from their process which has worked historically (e.g., deep fundamental work, valuation sensitivity, buying and holding quality businesses that compound over the long-term, etc). The current market is faster moving, more narrative driven, and if you’re constrained by fundamentals, you probably won’t get there on many of the higher torque AI-related names that are further out on the risk curve.

This is certainly not to say that all AI-related stocks are expensive. But many of the stocks that are going vertical require a continuation of heady demand years into the future, such that these stocks can grow into their lofty valuations. Investors dabbling in the more speculative part of the semis complex are increasingly underwriting demand that extends into 2030 and beyond. That demand might transpire, but these stocks become increasingly risky to the extent that investors are treating that growth as a sure thing.

There was broad acknowledgement from managers I spoke to that these stocks are expensive. But in terms of how those stocks are being traded and the market structure changes highlighted above, the absolute valuations of these stocks have been relegated to a secondary concern. Rather, the focus is squarely on whether these companies are accelerating their topline and producing earnings beats. So long as that is happening, seemingly expensive stocks can march higher. It’s the rate of change of the fundamentals in the short term that has mattered most for these stocks, and more and more non-pod investors are recognizing this and changing the manner in which they invest.

This approach of playing near-term accelerations/decelerations is anathema to fundamental investors who typically underwrite businesses based on the earnings and cash flows they will produce over long stretches of time. This approach acts as an anchor that makes it hard for fundamental managers to simply pivot into the stocks that are working.

That discipline helps avoid overpaying for speculative stocks, but it also makes it difficult to perform well in markets where investors are willing to pay up for outer year cash flows that rely on a chain of assumptions around ever increasing demand, restrained capacity additions, tech roadmaps that do not upend favorable supply/demand dynamics, and accommodating capital markets. In some of these AI stocks, the path to getting paid appears exceptionally narrow and deceptively multiplicative.

It does feel like there’s a huge spread in the willingness of the market to give credit to outer year cash flows for AI winners versus AI losers, which speaks to the prevailing confidence in the AI trade persisting.

The difficulty in adapting to this market is exacerbated by many managers feeling the need to adhere to what they’ve marketed to their LPs (i.e., sticking to what’s on the tin of the fund strategy). This dynamic is more acute for managers with more institutional mandates that will give far greater scrutiny to any process changes.

I heard numerous stories of fund managers who can invest on their personal account chalking up massive year-to-date returns, but being down in their fund. This likely reflects the tendency of a manager’s approach to investing to become sclerotic if their LPs are likely to penalize them for process changes (even if those process changes are necessary and a sensible course of action). I think the impetus to change is always greatest during periods of drawdown/underperformance but it was a topic in virtually all the conversations I was having.

Semis is the FOMO trade

Semis is now firmly the FOMO trade. Regardless of fundamentals, every manager is feeling the pull of the seemingly infinite money glitch of owning semis. Lots of generalists I’ve spoken to during my trip have sharpened their pencils on the space, with some shifting meaningful portions of their book into select hardware names.

So, while no doubt pods are in semis and using internet/software as funding sources, the rotations of capital out of software and into semis are to an extent also being directed by long-only funds that are obviously very conscious of lagging their benchmarks.

Interestingly, the generalists venturing into semis are unconstrained by the knowledge/experience of how low quality some of these names were considered previously, or how cyclical the fundamentals of these stocks have been historically. Rather, it’s easier to come to the space with a blank slate and, for example, form a view around the sustainability of the supply/demand imbalance in memory persisting.

We have not done a great job at playing the AI boom. We own NVIDIA and ASML as they are quality businesses and we can get comfortable with the valuations of these stocks. But they have much lower torque to the AI trade compared to say memory prices going parabolic, and they won’t have the same insane earnings beats. We have been waiting for a pullback which very much has not occurred in some of the semi stocks we’d be comfortable owning.

Semis tourists make the trade more fragile

The problem with so many generalists chasing semis is that it makes the AI trade more fragile. Having spoken to a number of investors in recent weeks who have recently initiated positions in semis, they have openly admitted that they’re not across the tech details and acknowledged that they could be blindsided by tech changes that are negative to fundamentals.

This is perfectly fine when there’s upside momentum in the stocks. But the risk is that an increasing portion of the shareholder bases of these hot semis stocks lack true conviction in the fundamentals, which increases the risk of an unwind to the extent that there are any unforeseen developments that cast doubt on the fundamentals (or perhaps even just if these stocks stop working, and momentum reverses).

Lots of managers are entering these stocks simply because they’re the stocks that are working and the fear of underperforming/career risk is forcing them to dance while the music plays. But because of this, they’re also much more likely to pull the plug once these stocks stop working. So while the fundamentals for many semi stocks are currently amazing (monstrous earnings beats and accelerating growth profiles), some of the valuations require conviction around very strong fundamentals extending into 2030+. We have been looking at names in the space and have struggled to build that conviction.

We manage money on behalf of high net worth individuals, family offices, a charity, and we have our own money, and our families’ money in the Fund. For this reason we do not feel compelled to chase the popular stocks in a hot market, and unnecessarily risking the capital we’ve been entrusted with managing. If we do not assess the risk/reward to be attractive, and we lack the conviction in that stock, we will pass, even if others are making a lot of money. These are just not risks we think are sensible to take.

It will be interesting to see how it all plays out, and as always, we welcome constructive pushback on any of the above!

[1] https://www.reuters.com/business/finance/hedge-funds-double-down-using-near-record-leverage-quest-boost-returns-2025-12-03/

[2] https://www.reuters.com/business/finance/hedge-funds-double-down-using-near-record-leverage-quest-boost-returns-2025-12-03/

Disclaimer / Disclosures

The information contained in this article is not investment advice and is intended only for wholesale investors. All posts by Bristlemoon Capital are for informational purposes only. This article has been prepared without taking into account your particular circumstances, nor your investment objectives and needs. This article does not constitute personal investment advice and you should not rely on it as such. This document does not contain all of the information that may be required to evaluate an investment in any of the securities featured in the document. We recommend that you obtain independent financial advice before you make investment decisions.

Forward-looking statements are based on current information available to the author, expectations, estimates, projections and assumptions as to future matters. Forward-looking statements are subject to risks, uncertainties and other known and unknown factors and variables, which may affect the accuracy of any forward-looking statement. No guarantee is made in relation to future performance, results or other events.

We make no representation and give no warranties regarding the accuracy, reliability, completeness or suitability of the information contained in this document. To the maximum extent permitted by law, we do not have any liability for any loss or damage suffered or incurred by any person in connection with this document.

Bristlemoon Capital Pty Ltd (ABN: 22 668 652 926) is an Australian Financial Services Licensee (AFSL Number: 552045).

George Hadjia and Daniel Wu are associated with Bristlemoon Capital Pty Ltd. Bristlemoon Capital may invest in securities featured in this newsletter from time to time.

A quality, clear-sighted take IMO